")

")

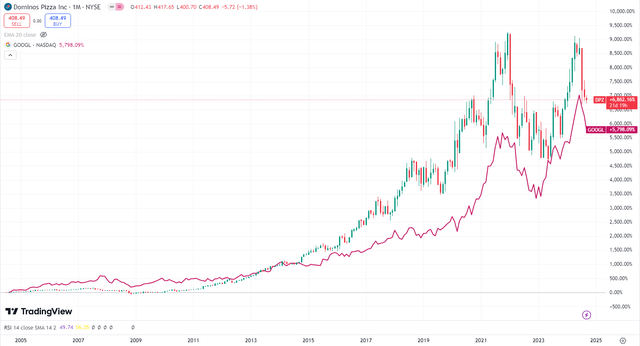

As I finished my last slice of Domino’s Pizza (NYSE:DPZ) today, I was inspired to write about the stock. It’s amazing to think that DPZ stock has seen mouth-watering returns over the years, up over 6,800% since its IPO in 2004, even outperforming Alphabet (GOOGL) (GOOG), which I just wrote about, during that time frame.

DPZ Stock Performance Compared To GOOGL Stock (TradingView)

However, the stock of the largest pizza chain in the world has been flat since Q3 2020. Overall, I think the days of stellar returns are over for Domino’s stock, as growth rates have slowed down and the current valuation is fair at best.

While there’s long-term upside potential in DPZ stock due to its expected growth, high-quality business model, and fair valuation, the upside potential isn’t enough to get me excited. Therefore, I rate the stock as a Hold.

What Makes Domino’s Business Model So Great?

Domino’s is primarily a franchisor, which, from what I’ve come across in the past, has generally been a highly profitable business model for several companies. 99% of its locations are owned and operated by franchisees, meaning that Domino’s essentially makes most of its money from royalties. This allows Domino’s to run the business with minimal capital expenditures, making it a free cash flow (defined as cash from operations minus CapEx) machine.

Capital expenditures only made up 2.4% of its sales (in the trailing 12 months), and its levered free cash flow margin in the same period comes out to 11.1%, for a total FCF figure of $511.6 million.

Domino’s Pizza’s Cash Flow History (Seeking Alpha)

Let’s compare that to Shake Shack (SHAK), another player in the QSR (quick-service restaurant) space. Shake Shack had 547 locations as of June 26, and only 236 of them are licensed (franchised). That’s 43% of SHAK’s locations. As a result, capital expenditures made up 11.7% of its revenues in the past 12 months, which negatively impacts its free cash flow for now.

Is There Growth Ahead For Domino’s Pizza?

Global pizza market growth: While there are already plenty of Domino’s Pizza locations (it has “a global enterprise of more than 20,900 stores in over 90 markets,” according to its most recent earnings report), there’s still growth ahead. According to Technavio, the global pizza market is forecast to hit $217.15 billion in value by 2027, exhibiting a CAGR of 6.26% from 2022 to 2027, although this includes all types of pizza sales, not just from restaurants.

Store count increase: Besides the global pizza market growth, Domino’s will continue to expand its store count. In the U.S. it expects to open over 175 net new stores per year from 2024 to 2028. Internationally, it will miss its original 2024 goal of over 925 net new stores by 175 to 275 stores because of “challenges in both openings and closures being faced by Domino’s Pizza Enterprises,” (OTCPK:DPZUF) according to the earnings report. The lowered international expectations likely are what caused the stock to fall after earnings, but still, that’s some decent growth for such a mature company.

New menu offerings can drive growth: On top of additional store openings, Domino’s can continue growing by introducing new menu offerings, such as its recently introduced New York Style Pizza, which features a thinner and more easily foldable crust.

Improved loyalty program: Additionally, last year, it improved its loyalty program by lowering the points threshold for rewards and offering a more diverse selection of rewards. This can incentivize people to order more often, and it has driven loyalty program order growth. In the Q2-2024 earnings call, Domino’s CEO Russell Weiner said, “For example, in our carryout business, orders with a loyalty redemption in the first half of 2024 are twice as high, 2 times, as they were in the first half of 2023 under our old loyalty program.”

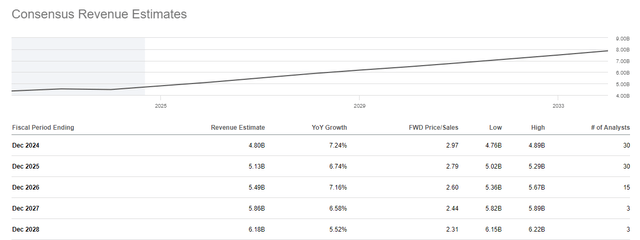

Uber Eats partnership to drive growth: Last year, Domino’s partnered with Uber Eats, and the firm mentioned that it saw a $1 billion opportunity in the aggregator marketplace. Uber Eats made up 1.9% of Domino’s sales in Q2, and it expects this figure to reach 3% or higher by the end of the year. The consensus revenue estimate for Fiscal 2024 comes in at $4.8 billion. So even if Uber Eats was to make up 3% of total 2024 revenues, that would still be only $144 million in sales, meaning that there’s lots of growth ahead.

Currently, Domino’s has an exclusivity agreement with Uber. But that agreement ends in Q1 2025. Then, Domino’s will decide if it wants to expand to other companies like DoorDash or stick with Uber only.

Overall, the company is expected to grow its revenue by roughly 6-7% annually over the next few years — similar to the growth expected from the global pizza market.

Domino’s Pizza Revenue Estimates (Seeking Alpha)

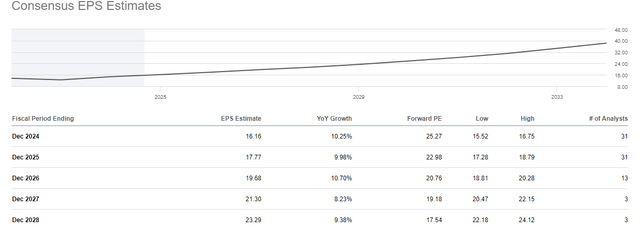

On the EPS front, the expected growth rate is a bit higher. See below. We’ll use these EPS estimates to help us with our valuation in the next section.

Domino’s EPS Estimates (Seeking Alpha)

DPZ Stock’s Valuation Is Fair But Not A Bargain

The image above states that analysts expect $16.16 in EPS for Fiscal 2024, giving the stock a forward P/E ratio of 25.3x. Yes, this figure is about 16.2% lower than its five-year average of 30.15x. However, the lower valuation is also somewhat justified because the company’s growth rate has slowed down over the years.

Per Finbox, Domino’s five-year diluted EPS CAGR comes in at 11.9%. Meanwhile, analysts’ EPS estimates imply growth rates that are slightly lower. While it’s not impossible for the company to see a valuation multiple expansion back to a 30x forward P/E, especially because it’s such a high-quality company, we like to be more conservative.

Assuming that the stock maintains the same P/E multiple, the stock price should rise in tandem with EPS growth over the longer term. This would give DPZ stock roughly 10% annual returns through December 2026 based on EPS estimates. It’s not bad, but it’s not exciting, either.

The Bottom Line on Domino’s Pizza Stock

Domino’s Pizza has a high-quality franchise business model that allows it to generate robust amounts of free cash flow and EPS via royalties. Further, the company has a good amount of growth ahead via new store openings, global pizza market growth, the Uber partnership, menu innovation, and its improved loyalty program.

Nonetheless, with EPS growth expected at 10.25% this year (plus 10% and 10.7% for the next two years), along with a forward P/E of 25x, the days of mouth-watering returns are over for DPZ stock. I don’t expect the stock to return much more than 10% annually over the next few years, which is fine, but it’s not exciting enough for me to give a Buy rating. Thus, I rate it as a Hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

")