")

")

Summary

Digital Realty Trust (NYSE:DLR / DLR.PR.L / NYSE:DLR.PR.K / DLR.PR.J) is a REIT that specializes in data center (“DC”), colocation, and interconnection solutions. Founded in 2004 and headquartered in Austin, Texas, the company has grown to become one of the largest global providers in the DC space. Its portfolio includes DCs and colocation facilities across North America, Europe, and Asia, catering to a diverse clientele that includes domestic and international companies across various industries, such as IT, financial services, and telecommunications. The company’s strategic focus on connectivity, reliability, and scalability has enabled it to establish a significant presence in key markets worldwide, supporting the DC and colocation needs of businesses as they expand their digital infrastructure. Over the years, DLR has executed a growth strategy that includes both organic development and strategic acquisitions.

The increasing prevalence of AI products has been a boon for DC providers over the past year or so. The market is supply constrained, driving robust rent growth and leasing activity. The market has given DLR a lot of credit for these developments, with investors expecting AI to drive the next gold rush for DCs.

Unfortunately, DLR’s relatively old portfolio of legacy DCs and intense focus on growth have financially put it in a tight spot. It relies on capital recycling, dilutive equity issuances, and JVs to fund growth. This has led FFO and AFFO per share to remain virtually flat over the past 2 years. With upcoming debt maturities set to further increase interest costs, we see this trend as likely to continue for the foreseeable future.

Against that backdrop, we see the ~37% premium to our NAV estimate as a risky entry point and believe we missed our chance to buy the shares at a high but potentially reasonable price in 2023. We also considered the 3 Series of listed preferred stocks but concluded that they are also unattractive to us given the relatively low yield, modest discount to liquidation preference, and low likelihood of redemption in the near term, given the company’s capital constraints.

We give the 4 securities a Hold rating, with a bearish tilt, on valuation. They are too expensive to consider a Buy, but we see the near-term fundamentals of the DC market as too good to allow material underperformance.

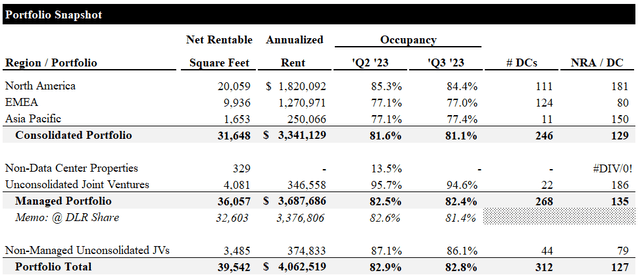

Portfolio Snapshot

DLR’s consolidated portfolio comprises ~32k sqft of net rentable area (“NRA/NRSF”), concentrated mainly in North America. It owns a further ~4.4k sqft of NRA in non-data center properties and unconsolidated JVs, and ~3.5k sqft in non-managed and unconsolidated JVs.

Occupancy remains relatively weak in the low-80s within the owned portfolio, compared with market vacancy rates of <8% in key markets (e.g., DFW, Virginia, and Chicago). Based on expert calls with an ex-DLR account director, we understand this to be a function of the age of the REIT’s assets and organizational issues, particularly in its sales force.

Portfolio Snapshot (Empyrean; DLR)

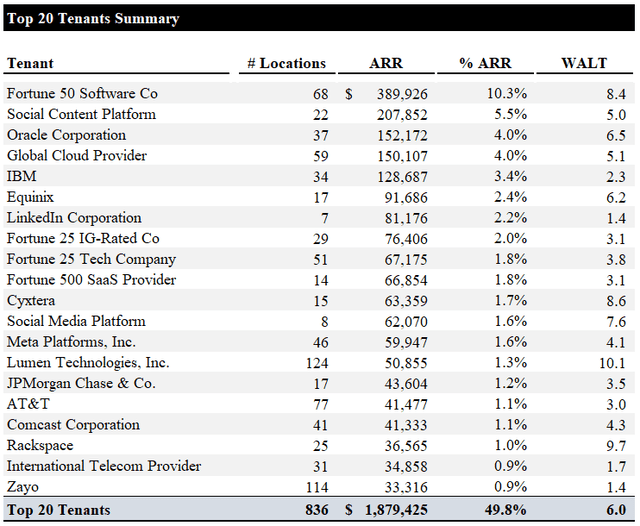

Given the sensitive nature of DC operations, DLR does not disclose the specific identity of many of its top tenants, making it difficult to assess credit quality. Many are highly creditworthy (e.g., IBM, Meta, etc.), while there are 2 that stand out as concerns: Cyxtera and Zayo. Cyxtera recently filed for bankruptcy and was approved for sale to Brookfield. Zayo, while not in bankruptcy, has its first lien TLs trading in the 80s and senior debentures trading in the high 70s.

Top Tenants (Empyrean; DLR)

Given the high demand for DC space and power, and significant lack of supply, we are not overly concerned about the tenant profile. We do see the age of the portfolio, and the upgrade capex requirement this entails, and the issues in the sales force as greater concerns.

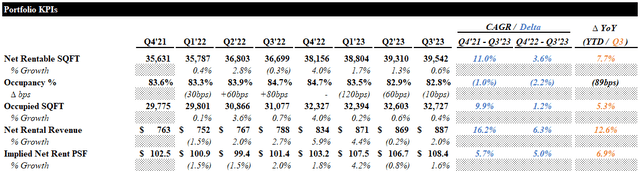

Recent Performance

Total portfolio NRA has increased ~11% from Q4’21 to Q3’23. Despite a slight decline in occupancy, net rental revenue has grown ~16% (n.b., ~6% cumulative increase in implied net rents).

Portfolio KPIs (Empyrean; DLR)

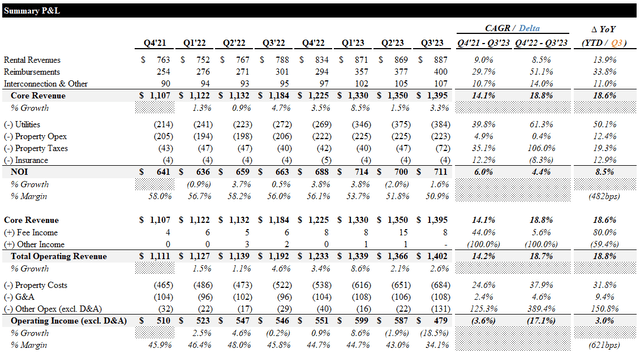

Rental revenues have grown at a ~9% CAGR and are up ~14% YoY in the YTD Q3’23 period. A ~30% CAGR on tenant reimbursements was insufficient to fully offset cost inflation, diluting the NOI CAGR to ~6% (n.b., ~480bps of NOI margin dilution YTD).

Summary P&L (Empyrean; DLR)

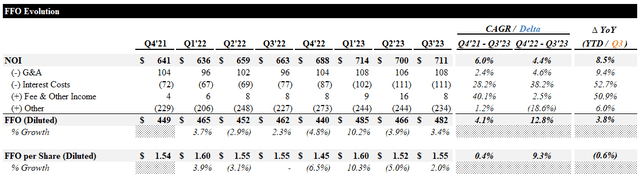

The ~6% NOI CAGR was further diluted by a ~28% CAGR in interest costs, leading to a ~4% CAGR on diluted FFO. Share issuances further eroded this growth, leading to a flat FFO per share trajectory.

FFO Evolution (Empyrean; DLR)

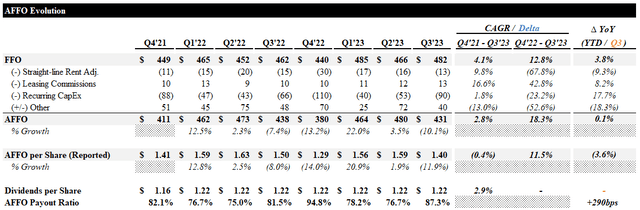

Elevated leasing commissions contributed to AFFO growth (n.b., ~3% CAGR, flat YoY YTD) being slightly weaker than FFO growth.

AFFO Evolution (Empyrean; DLR)

The dividend was raised ~5% in Q1’22 to ~$1.22 per quarter and has remained at that level since. The AFFO payout ratio has hovered around ~80% through ’23 YTD. In our view, rising interest costs, occupancy pressure and the capex requirement for the growth strategy make a dividend increase unlikely in the near term.

Valuation

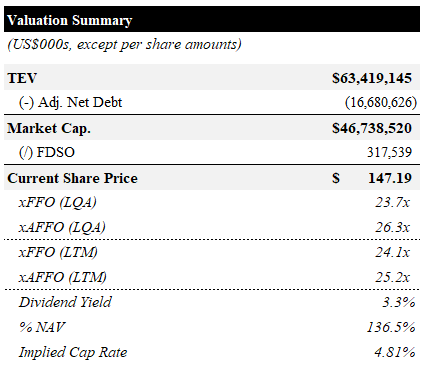

DLR is trading for ~23.7x / 26.3x LQA FFO / AFFO per share (n.b., ~24.1x / ~25.2x LTM). It yields ~3.3% and is trading at a ~37% premium to our NAV estimate (n.b., ~4.8% implied cap rate). We discuss the assumptions used in our NAV estimate below.

Valuation Summary (Empyrean; DLR)

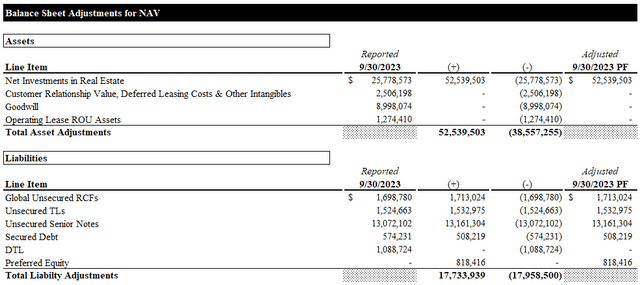

The principal balance sheet adjustments used to derive our NAV estimate are shown below. We applied a 6.5% cap rate to an NTM NOI assumption of LQA NOI + 10%. The cap rate assumption is based on management’s disclosures for the July ’23 JV with GI Partners, and is a ~50bps premium to the DLR’s sale of 3 hyperscale JVs to TPG for a 6% cap. The 10% NTM NOI growth assumption is based on Q3 same-capital cash NOI growth of 9.4%.

Balance Sheet NAV Adjustments (Empyrean; DLR)

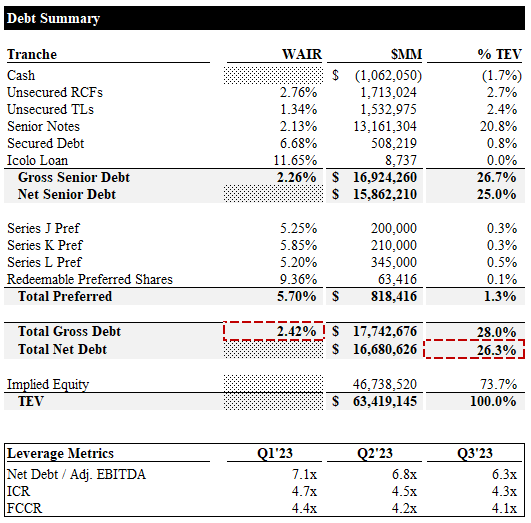

Leverage is extremely reasonable, ~27% / ~25% of TEV gross / net (n.b., ~18% / ~26% including pref). Net debt / EBITDA has declined ~0.8x in the last two quarters. Interest and fixed charge coverage have tightened but remain extremely healthy at >4x. Given the seemingly modest leverage profile, we also wanted to take a look at the listed prefs: Series J, K, and L.

Debt Summary & Cap Table (Empyrean; DLR)

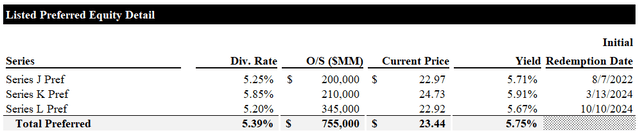

All 3 Series trade for modest discounts to liquidation preference and offer high 5% yields. The Series J has been eligible for redemption since August ’22 but remains outstanding. The Series K and L are eligible for redemption in March and October ’24, respectively. As DLR has elected to not redeem Series J, it is difficult to make a strong case for them to redeem the Ks or Ls. The case is stronger for the Ks, as they are 60-65bps more expensive than the Js and Ls.

Preferred Stock Detail (Empyrean; DLR)

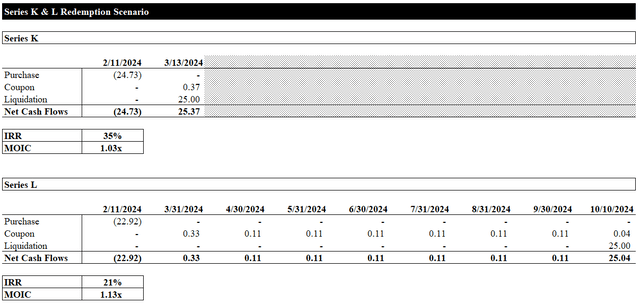

Below are our returns calculations for the Ks and Ls under a redemption scenario.

Series K & L Redemption Return Analysis (Empyrean; DLR)

Given the short time frames, the returns look attractive on an IRR basis. On a MOIC basis, they look less exciting given the modest discount (i.e., less capital appreciation) and low yield. When we layer in the fact that DLR has chosen to not redeem the Js despite having more than a year to do so, we don’t love the risk/return profile. For a REIT pref redemption play, we much prefer Gladstone’s Series E.

Risks / Catalysts

Leasing Momentum

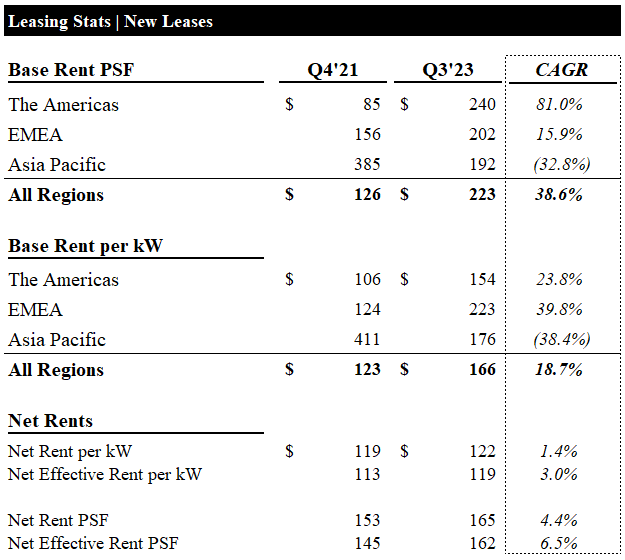

DC lease rates have trended up consistently since ’21, as major markets across the world are supply constrained. Rising costs of capital, land, materials, and a lack of power availability have slowed construction and completion. This is all happening against a backdrop of consistent demand growth, now accelerating due to AI deployments.

New Lease Rates (Empyrean; DLR)

As seen above, the base rents DLR has been commanding on new leases have exploded over the past 2 years (n.b., ~39% CAGR on base rent PSF, ~19% per kW). However, much of this growth is attributable to the rising capital and operating costs outlined above. Net and net effective rents PSF have grown significantly slower, at ~4% and ~7% CAGRs, respectively. On a per kW basis, the pricing growth has been even less stellar, at ~1% and ~3% CAGRs on the net and net effective rents per kW, respectively.

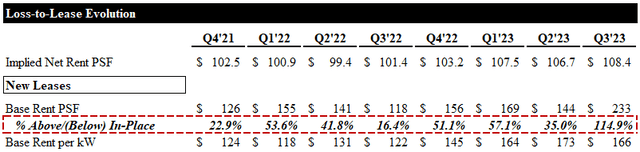

Although market net rents are growing modestly, they are still significantly higher than DLR’s in-place lease rates. Below, we see the loss-to-lease evolution over the past 8 quarters.

Loss-to-Lease Evolution (Empyrean; DLR)

The loss-to-lease implied by these 8 quarters’ leasing activity averages ~49% (i.e., average ~49% rent uplift upon re-leasing). This provides plenty of room to drive rent growth above the low single-digit market rent growth implied by the previous set of figures. However, while this is a fundamental catalyst, the market is already giving DLR quite a bit of credit for this with the ~37% premium to NAV.

Capital Allocation

DLR’s capex guidance for full-year ’23 is +$3bn, more than 1.5x its LTM and LQA FFO. While most of this is related to developments, and it is therefore considered growth capex, it is still money out the door. This shortfall, though entirely intentional, leaves DLR capital constrained. This is likely a major factor in management choosing not to redeem the Series J preferred, utilize JVs, and recycle capital – something most other DC REITs do not do to the extent DLR does. It is also very likely behind management’s recent dilutive share issuances.

Management issued ~11.3MM (n.b., ~4% of Q1’23 fully diluted shares) shares at a weighted average price of ~$96.35 in Q2 and Q3’23. This means that management issued equity at a price which implied a ~5.1% yield, while it had capacity on its RCF, which bears interest at a rate of ~2.8%.

This is certainly not the type of capital allocation we love to see as shareholders, especially in a sector that is supposed to benefit from highly favorable supply/demand dynamics.

Conclusion

We set a very high bar for Buy ratings on REITs trading at premium valuations, let alone a ~37% premium to NAV. There is a strong argument to be made for DC REITs to trade at a premium, given the extremely strong market fundamentals, but we have 2 main concerns. First, how long will the AI-driven DC boom last? Based on expert calls, we’ve heard that the market is expected to begin stabilizing in ’25, but we can’t say for sure. Second, DLR’s portfolio is relatively old and will require substantial capex to be upgraded to handle the technical requirements of AI workloads (e.g., density and water cooling). These two concerns make us uncomfortable paying a premium multiple for the business. We also have a hard time making the bearish argument, as the AI tailwind will likely persist for the short term, and the sector is highly favoured.

The prefs also remain unappealing. The capital requirements to upgrade the portfolio and realize management’s lofty growth ambitions make redemptions unlikely in the near term, and we see greater return potential and certainty of redemption in other REIT pref redemption plays (i.e., GOODN).

For now, we rate the common and pref as Hold with a bearish bias.

Read the full article here

")