")

Business Update Conference Call Transcript")

")

Introduction

Customers Bancorp (NYSE:CUBI) is a regional bank in Pennsylvania that just reported a strong second quarter, beating on both the top and bottom line. With the market not rewarding shares higher post-results, I think the market is underappreciating a notable increase in its net interest margin, up 19bps to 3.29%. This uptick highlights the bank’s successful shift towards higher-yielding loans and improved deposit cost management. Despite a slight decrease in total assets and deposits, the bank’s earnings exceeded expectations, with an adjusted EPS of $1.48, surpassing both consensus estimates and previous results. In this article, I’ll provide a comprehensive overview and analysis of the company’s latest Q2’24 performance and why I’d be a buyer of shares at the current price.

Company Overview

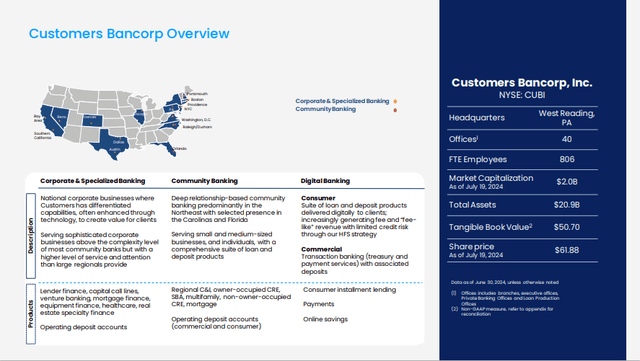

Customers Bancorp is a bank holding company that offers a wide range of financial products and services for both individuals and businesses. The bank provides various types of deposit accounts, including checking and savings accounts. It also offers a variety of loans for business needs, real estate purchases, and personal mortgages. In addition to traditional banking services, Customers Bank specializes in industry-specific financing and services, such as tech and healthcare loans, equipment financing, and real estate. The bank is also involved in digital and technology-driven banking, including services for fintech companies and blockchain-based payments and supports additional banking functions like mobile and online banking, wire transfers, and merchant services. Founded in 2009, Customers Bancorp is headquartered in West Reading, Pennsylvania and has over $20 billion in assets.

Investor Presentation

CUBI Q2 Results

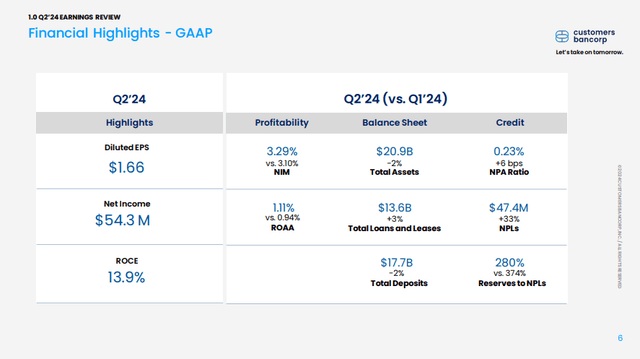

When looking at the latest results for Customers Bancorp, which I’ll just refer to as CUBI for short, the company reported $1.66 in earnings per share. After adjusting for several non-core items including unrealized gains on equity investments and severance payments, EPS would have been approximately $1.48.

Compared to consensus estimates of $1.43, CUBI seems to have had a great quarter. The main difference, I believe, to consensus estimates were on revenues, which outpaced estimates by $3 million, which would have translated to $0.11 in EPS, but a $0.05 miss on expenses.

Investor Presentation

On the earnings call, management reiterated full year guidance for the company and gave more detail on some balance sheet transactions executed and decisions made during the quarter.

My takeaway overall is that these were positive developments. Net loan growth was 2.8%, a modest gain and the growth reflected a mix-shift out of securities and cash balances rather than outright balance sheet growth and in fact, total assets fell nearly 2%. Within categories, growth came within the bank’s specialty lending verticals, representing a continued mix-shift from consumer into commercial. Specific contributors were fund finance, healthcare and equipment finance. On the conf. call, management reiterated its guidance of achieving 10-15% growth for 2024, backed by a strong loan pipeline of roughly $400M-$500 million booked into Q3’24.

Regarding deposit growth, deposits fell 1.5% against last quarter. CUBI is now in phase 2 of its deposit transformation, reducing higher cost business unit deposits in favor of lower cost core relationships. Deposit costs ticked down for the quarter by 5 bps to 3.40%, but I was surprised that NIB fell by 5% last quarter to 25% of total balances. Management noted on the call that the blended rate of deposits on-boarded is ~3% with 25-30% coming in NIB balances, and they remain optimistic the deposit franchise strategy will reduce cost of deposits further in lieu of rate cuts.

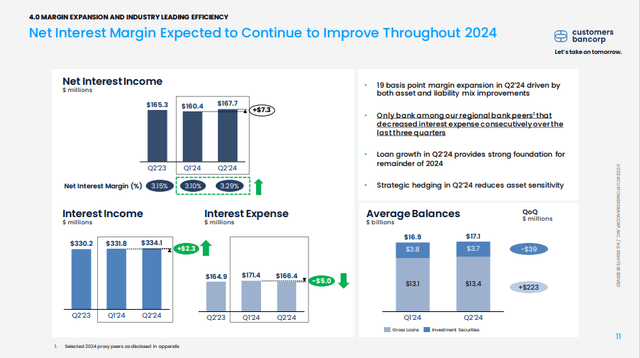

In my view, one of the positive parts of CUBI’s Q2’24 results was that NIM was up 19 bps compared to last quarter to 3.29%. Overall, the margin benefited by a mix-shift into higher yielding loans and a 5bps reduction in average deposit costs as the deposit franchise strategy plays out. Moreover, the NIM included a 5bps boost from prepayment income on loans & securities. Nevertheless, the company did quite well on this measure, which suggests to me that would mean a slightly higher run-rate moving into the second half of the year. Given this, NIM should be on track for further expansion and I think it’s becoming more likely that management can hit the high end (or even exceed) the previous guide to reach the higher end of the 3.20-3.40% range by year-end.

Investor Presentation

Regarding efficiency ratios and costs, I think CUBI saw positive developments on this front as well. After adjusting for one-time items including $2.6 million in severance, comp costs increased by $6.4M over the last quarter. Management noted that the new teams are fully baked into run rate in Q2’24 results and targets early 2025 as breakeven. Expenses translated to an efficiency ratio of 53.5%, a ratio much better than we’ve previously seen out of CUBI.

Typically, a high-efficiency ratio indicates that a bank is spending less to generate each dollar of revenue, meaning it is operating more efficiently. Conversely, a higher ratio suggests higher expenses relative to income, which might indicate inefficiencies or higher operating costs. On the earnings call, management said that they expect an elevated efficiency ratio in 50%s for a few quarters, but I wouldn’t be surprised to see that trickle down to the 40% range long-term, which would be more in line with peers.

On credit, I believe CUBI’s credit continues to look strong. This quarter, NPAs were up modestly off of low absolute levels to 23bps of assets from 17bps in the previous quarter. NCOs have been fairly stable over the last few quarters, and came in at 56 bps annualized in Q2’24. Provisioning of $18 million, resulted in a contraction in reserve levels from 1.12% to 1.08% last quarter. In my view, credit remains in good shape at the bank.

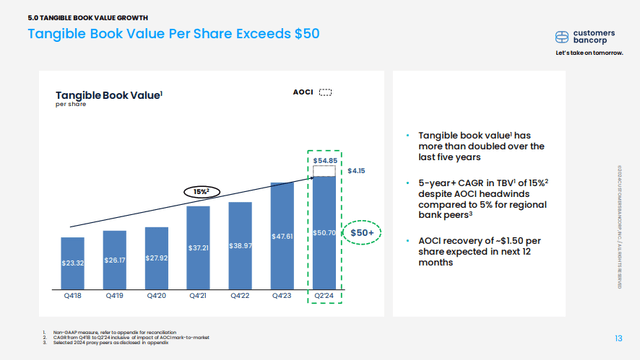

Lastly, on capital, CUBI had a CET1 ratio 12.8% up from 12.5% last quarter, both of which are above the company’s 11.5% target. The TCE ratio ended the quarter at 7.7%, also ahead of the 7.5% target. TBVPS grew 3% compared to last quarter to $50.70, now above the $50 level. Finally, CUBI announced a new buyback program in June. That said, in my view, the priority is clearly organic growth, and I’d expect that significant use of the buyback program is unlikely for now.

Investor Presentation

Valuation and Wrap Up

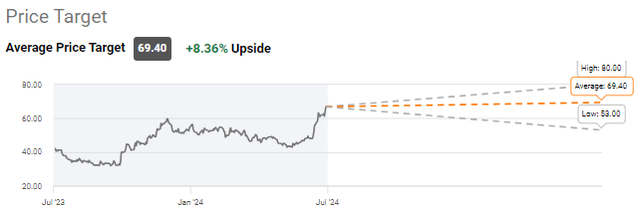

Based on the 10 sellside analysts who cover CUBI’s stock, there are 8 ‘buy’ ratings and 2 ‘hold’ ratings. The average price target is $69.40 with a high estimate of $90.00 and a low estimate of $53.00. From the current price to the average price target one year out, this implies approximately 8.4% upside, not including the dividend.

Seeking Alpha

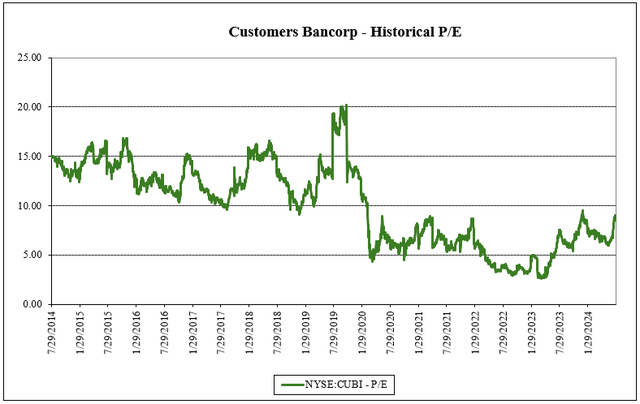

From a valuation perspective, CUBI has traded within a range of 2.6x to 20.2x P/E. Most of this variation can be attributable to the 2020-2022 period, where EPS shot up in 2021 by 148% before declining 35% the following year. Accompanied by large swings in the share price, this created a wide range between the high and low range. On average, however, the company has traded at an average P/E multiple of 10.0x (source: S&P Capital IQ). At the current valuation of 9.0x P/E, CUBI appears to be trading at a discount to its historical average valuation.

Author, based on data from S&P Capital IQ

In my view, even though CUBI trades slightly above book value at 1.16x, the company appears cheap on a P/E multiple. Why? With $7.61 of EPS for the most recent LTM period, analysts are forecasting EPS of $8.64 in 2026, growing at a 5.2% CAGR (source: Bloomberg), given this, I find the valuation to be quite compelling.

Altogether, given a strong second quarter, particularly on net interest margin and efficiency ratios, I think investors ought to take another look at CUBI. For a company that can continue to grow EPS from here, I find the valuation at 9.0x P/E attractive, despite a small premium to book value. As such, I rate shares as a ‘buy’.

Read the full article here

")

Business Update Conference Call Transcript")