")

")

Introduction and investment thesis

Shares of CrowdStrike Holdings, Inc. (NASDAQ:CRWD) lost 40% of their value within two and a half weeks after the widely reported global outage swept through 8.5 million Windows devices, going down as one of the most significant cybersecurity events in history. One day after the news came out, I came to the following conclusion:

“However, after recent negative headlines came to light, I think shares could stay in the penalty box for a while. Besides negative publicity, I think CrowdStrike could potentially face negative financial consequences from businesses worldwide, which had to suspend their operations for hours. Until these issues settle, and the market gets a precise update on what to expect, uncertainty will prevail, which is the worst enemy of investors.”

Even though it became clear quickly that CrowdStrike’s financial liabilities are mostly capped by the fees paid by their customers, there were some companies who decided to file a lawsuit against the company with uncertain consequences. Adding the possibility of losing customers and slowing new acquisitions, this uncertainty pressured shares for a while. The big turnaround came on the 5th of August, where a significant intraday loss has been reverted into a small gain. This turnaround didn’t run out of steam until the publication of FY25 Q2 earnings, which could have been regarded as a make-or-break release in the light of recent events.

As the incident occurred on the 19th of July and the Q2 quarter ended on the 30th of July, the most interesting data points in the Q2 release are the Q3 and FY25 guidance and the development in remaining performance obligations. Based on this data, it appears that customers remained loyal to the company, as the FY25 revenue guidance has been trimmed by only 2.4%. Meanwhile, on the bottom line, CrowdStrike expects $123 less non-GAAP operating income for this fiscal year, mainly resulting from additional costs related to the outage. This equals only $0.5/share, which is not a significant amount as well. I think investors can breathe a sigh of relief, and with this, I reset my initial Strong Buy recommendation for the stock.

CrowdStrike retains customers’ trust

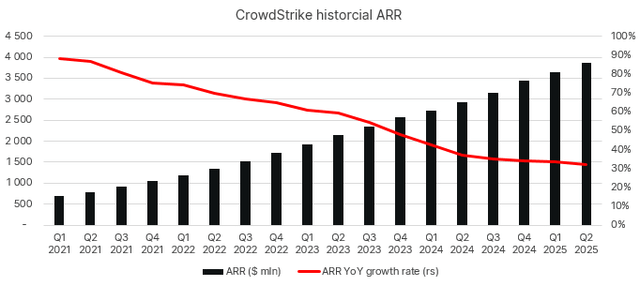

Most market participants agreed that CrowdStrike’s response to the incident has been exceptional, which received confirmation in the current Q2 earnings release. Q2 reported numbers have been only slightly impacted by the outage, as there have been only 8 business days left from the quarter after the outage. However, it’s still worth taking a brief look at them to examine business momentum going into the incident. Looking at the company’s key topline growth metric, annual recurring revenues (ARR), their YOY growth continued to stabilize slightly above 30% coming in at $3.86 billion:

Created by author based on company fundamentals

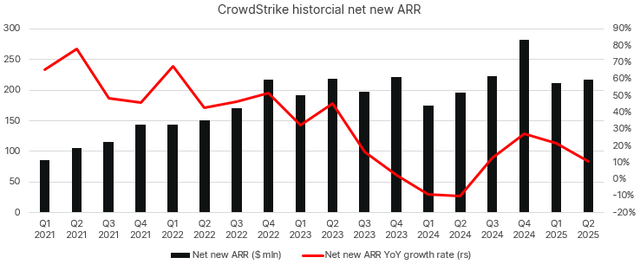

I believe this seems encouraging at the first sight, as the previous tendency of stabilization continued. Looking at the growth of new ARR reveals a somewhat softer picture for the first sight, showing stagnation compared to the previous quarter with $218 million:

Created by author based on company fundamentals

However, it’s important to note that looking at seasonal tendencies net new ARR tends to increase only slightly from the Q1 to the Q2 quarter, so it would be too early to draw a far-reaching conclusion from this. Although we must admit that the YOY growth rate fell from 22% to 11%, which is something to bear in mind for the future.

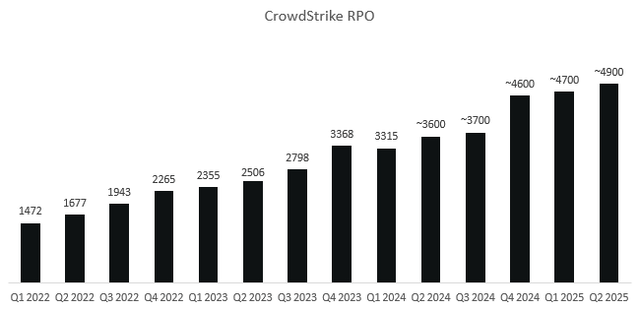

Looking at customer commitments, we could have witnessed continued growth over the quarter, meaning that customers didn’t pull significant future business from CrowdStrike immediately following the outage. Remaining performance obligations reached ~4.9 billion based on the company’s supplemental financial information, which is mostly in line with seasonal tendencies:

Created by author based on company fundamentals

This is also a good sign that top-line growth prospects remained strong.

However, the most influential data point in the Q2 release has been the guidance for Q3 and FY25 in my opinion, as it already incorporates CrowdStrike’s most up-to-date perception regarding the impact of the incident on fundamentals.

The most important data points for which the company guides in this regard are total revenue and operating income:

Created by author based on company fundamentals

In the Q1 earnings release, CrowdStrike guided for total revenue of $3.993 billion for FY25, which has been trimmed only by 2.4% to $3.896 billion in the Q2 release. I believe this indicates that the company doesn’t count on losing significant current or future business, furthermore, this could also result from the impact that sales reps had to deal with the outage instead of generating new business.

Looking at operating income, the picture is not so rosy for the first sight, as the previous guidance of $903 million has been trimmed by 13.6% to $780 million. I believe the majority of this will be only a one-time extra cost to compensate customers and the additional costs incurred in managing the incident. CrowdStrike has 242 million shares outstanding, so these additional costs make up $0.5/share. In the light of the fact, that at the time of writing the share price is still ~$70 below the pre-incident close, I think these costs can be regarded as not material as well.

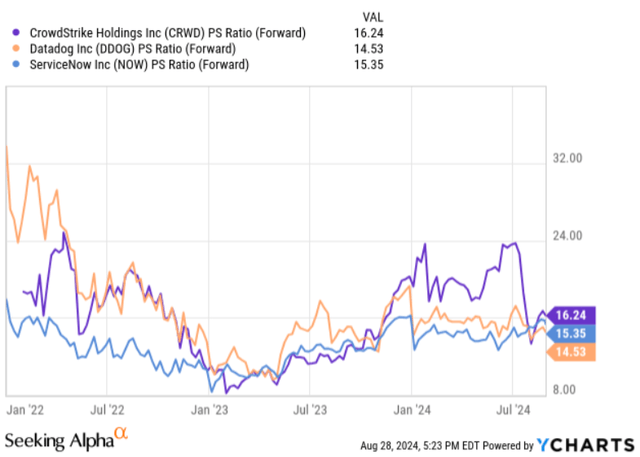

Based on the above, I believe CrowdStrike will continue to operate as a Rule of 60 (annual revenue growth rate + FCF margin) company over the upcoming quarters, which is still quite unique in the SaaS space. Comparing the company’s current valuation to other leading SaaS companies, we can see that the significant valuation gap diminished based on forward Price/Sales multiples, although it seems there hasn’t been such a material deterioration in fundamentals:

Seeking Alpha – YCharts

Both Datadog (DDOG) and ServiceNow (NOW) are leading companies in their respective businesses with a projected Rule of 55, and Rule of 53 for this year, respectively. Currently, it appears that CrowdStrike will be able to maintain its Rule of 60 metric, which deserves a higher valuation premium in my opinion.

This shows that in the light of reassuring news that the global outage didn’t divert CrowdStrike Holdings, Inc. from its growth path, there could be further upside for shares. Although there are still some risks lingering around the incident, I believe the current risk/reward setup provides a good entry point for shares.

Read the full article here

")

(RSKD)")