")

")

")

Written by Nick Ackerman

Crescent Capital BDC, Inc. (NASDAQ:CCAP) is a business development company (“BDC”) focused on debt investments, primarily first-lien investments with floating rates. They run a $1.6 billion portfolio spread across 183 companies. Like many BDCs lately, CCAP has been running higher, but still sports a slight discount to its last reported net asset value. We should be getting the next update with their earnings coming up in early August.

A “higher for longer” rate environment has seemingly been pushing up BDCs, as they continue to be an area that benefits from the higher rate environment. That said, based on the latest Fed projections, rate cuts are expected, and some caution could be warranted. On the other hand, we aren’t expecting rates to go back to zero – at least not without the economy really starting to tank. So this can be an area of the market that can still produce some attractive yields for investors.

CCAP is one of those that currently has an attractive yield of 8.67% based on the regular quarterly dividend, which was recently raised in the latest quarter. They’ve also been able to pump out special dividends to help boost that regular yield even higher. Paying out specials is a nice way to be able to provide flexibility in the future should they need to cut back on those, but still be able to preserve the regular quarterly payout.

About CCAP

CCAP is an externally managed BDC managed by Crescent Cap Advisors. This can sometimes give some investors pause because there can be some conflicts of interest when a BDC is externally managed. In this case, I’m not too familiar with the Crescent Capital Group, as I’ve never heard of them. They are a rather niche credit-focused alternative asset management investment firm with around $40 billion in AUM. They’ve been around for “over 30 years.”

This BDC was incepted on February 5, 2015, with $1.6 billion being managed. To get to this size, they had a bit of help when they merged with First Eagle Alternative Capital BDC in 2023, and in 2020, they merged with Alcentra Capital.

CCAP focuses on the core middle market and lower middle market investments; these are investments that are between $35 to $200 million EBITDA and $10 to $35 million EBITDA, respectively.

A Look At Leverage And Portfolio

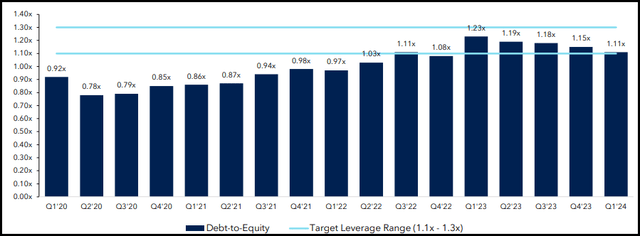

Like all BDCs, they utilize leverage in their strategy. This increases volatility and risks, but it also comes with providing greater potential yield and returns. The latest debt-to-equity ratio came to 1.11x, which puts it just into its target leverage range. This ratio has been coming down in the last year.

CCAP Debt-to-Equity (CCAP)

One of the key features that helped most BDCs during this higher rate environment is that they carried a large portion of fixed-rate borrowing costs combined with a portfolio that was primarily floating rate-based. That simply saw the spreads they were earning widen significantly when the Fed was raising rates aggressively, and it is where we still are today.

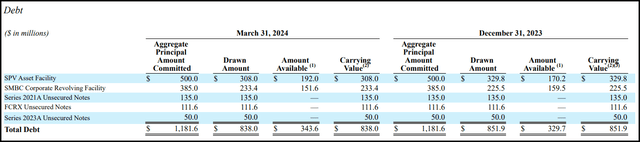

In looking at the total debt employed from the various instruments for CCAP, we are leaning more toward employing floating rate debt.

CCAP Leverage (CCAP)

The SPV Asset Facility and SMBC Corporate Revolving Credit Facility are the largest batches of leverage, and they come with floating rates. However, they do still have some unsecured notes coming with fixed costs. Still, as of March 31, 2024, about 65% of their borrowings were floating compared to fixed rates.

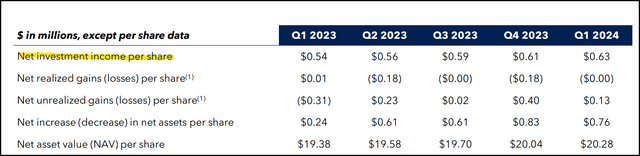

Fortunately, it is not all bad news for CCAP investors because this is also paired up with a portfolio that is overwhelmingly floating rate-based underlying loans. That makes up 98% of the underlying portfolio, with 90% of their portfolio also being first-lien. That’s resulted in seeing net investment income rise over the last several years. 2022 saw NII come in at $1.93 compared to $2.30 for 2023.

Even over the last year, we continue to see NII per share climb from $0.54 on March 31, 2023, to $0.63 as of March 31, 2024.

CCAP Financial Metrics (CCAP (highlights from author))

Analysts expect CCAP to report an NII of $0.58 in the next quarter, which would be a decline sequentially but year-over-year would be up from the $0.56 they posted in Q2 2023. For 2024, analysts expect NII at $2.33, up from the $2.30 posted last year. That could be pressured if we get more rate cuts than expected later this year.

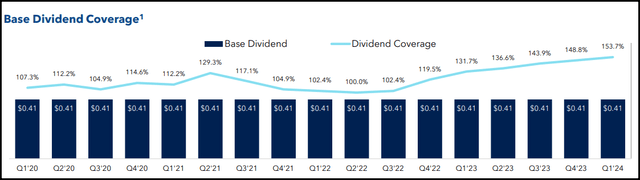

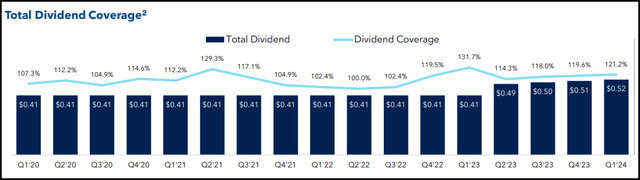

With high NII, that has come with high dividend coverage for this name, as they haven’t ramped up their regular quarterly dividend nearly as much as NII has increased. However, they did finally increase it to $0.42 in the latest quarter, an increase of 2.4%.

CCAP Regular Base Dividend Coverage (CCAP)

This is ultimately what has allowed them to pay out several specials throughout the last year.

CCAP Total Dividend Coverage (CCAP)

Specials should never be relied on, but given such strong coverage, we could anticipate they are likely to continue for the time being. That could even be the case if we only get a few rate cuts that are projected over the next year, as coverage would remain quite strong.

Another positive factor with such strong dividend coverage, even when considering the specials, is that it can allow for some growth in the NAV per share. Whatever is retained is going to stay within the portfolio and be calculated into the NAV. That’s one of the reasons why we can see NAV rising as well over the last year.

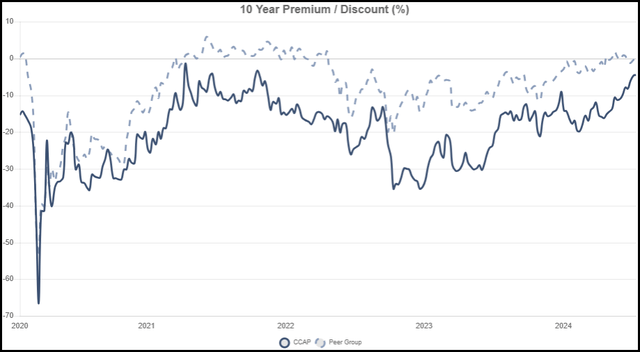

With shares pushing higher, it has narrowed this BDC’s discount from where it was. However, if NAV is expected to keep rising higher, that could be an appropriate reason why investors may choose to continue to narrow the discount and keep bidding up shares.

CCAP Discount/Premium History (CEF Data)

Non-Accruals And PIK

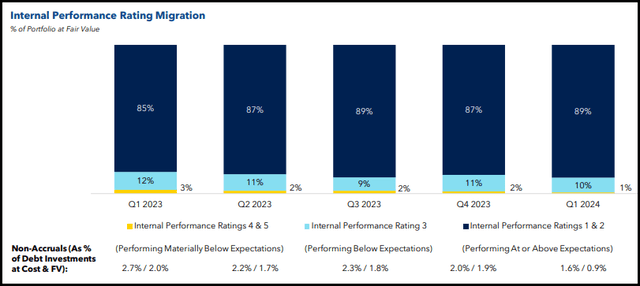

Another common feature of BDCs is non-accruals. Investing in smaller companies that may not be as financially sound always comes with some problems eventually. It is trying to manage those problems and keep them limited, so the winners outweigh the losers by a significant degree. For CCAP, non-accruals haven’t been too much of a problem in the latest quarters. Thirteen investments may be non-accrual, but that doesn’t represent a very large portion of their total debt investments based on cost or fair value.

As of March 31, 2024, we had thirteen investments across seven portfolio companies on non-accrual status, which represented 1.6% and 0.9% of the total debt investments at cost and fair value, respectively. As of December 31, 2023, we had seventeen investments across nine portfolio companies on non-accrual status, which represented 2.0% and 1.9% of the total debt investments at cost and fair value, respectively. The remaining debt investments were performing and current on their interest payments as of March 31, 2024, and December 31, 2023.

That’s one of the benefits of having such a diversified basket of loans spread across 183 portfolio companies. Quite a few of them can turn sour without rocking the boat too much.

The non-accruals listed above are also reflecting a downward trend of non-accruals as well, which is great to see. The majority of their portfolio they consider to be running strong in their 1 and 2 rating buckets, which is performing at or above the management’s expectations. That could suggest that they see minimal disruptions, at least in the near term.

CCAP Internal Portfolio Rating (CCAP)

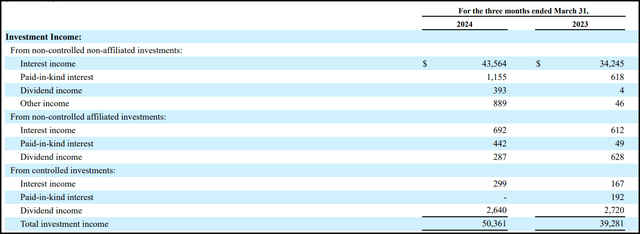

Another factor to consider for a BDC is the paid-in-kind interest. Too high of PIK can be a concern as it’s not really generating cash flows that can support the payout even if dividend coverage looks high. So total investment income and net investment income can rise materially, but it might not matter if PIK is also rising exponentially.

CCAP Investment Income Breakdown (CCAP)

In the case of CCAP, that does not appear to be a problem, as PIK accounted for 3.17% of total investment income for Q1 2024. On a relative basis, that was a material rise from the 2.19% reported in the same quarter a year ago, but on an absolute basis is rather negligible. For all of 2023, PIK accounted for 2.28% of total investment income.

Conclusion

CCAP sports an attractive regular dividend yield of around 8.7%. That may not be the highest yield available in the BDC space, but it is strongly supported by significant NII. It’s also enough to be able to provide regular special dividends, and they are likely to continue to be in such a position going forward as well, even if we get a few rate cuts. When including these specials, the yield based on the last year comes up to 10.47%.

Of course, it is all up to what management wants to do with the excess earnings. Continuing to pay some excise tax may be appropriate if it helps strengthen the underlying NAV and bolsters even stronger future cash flows to investors.

With a shallow discount currently, it might not be a screaming buy, but it also seems like one of the BDCs that is in a relatively strong position overall. If they can continue to grow NAV, then even a shallow discount can look quite enticing for investors today to consider building a position in this name.

Read the full article here

")

")