")

One of the most important companies in the cryptocurrency market in the United States is Coinbase (COIN). If you like Coinbase, you can buy the stock and sell it at a profit if you’re correct about the company’s future. If you really like it, you can leverage up with the GraniteShares 2x Long COIN ETF (CONL) which I just covered for Seeking Alpha recently – though I’ll reiterate that I think that’s a bad idea, personally. Obviously, there are also options strategies that individual traders/investors can play as well.

But if these various methods of market wagering aren’t enough, now one can even bet on people betting on COIN stock through options with the YieldMax COIN Option Income Strategy ETF (NYSEARCA:CONY).

Fund Details

CONY is casino draped in an income ETF wrapper. The goal of the fund is indeed to return capital to shareholders through distributions. However, since Coinbase doesn’t actually pay a dividend to shareholders, distributions from an ETF that exists solely to play COIN options has to come from the premiums in the options strategy. Therefore, the fund never actually holds COIN stock. Rather, it has a synthetic long position from writing call options that cap any gain the ETF has if COIN stock takes a significant run higher.

| Fund Information | CONY |

|---|---|

| Gross Expense Ratio | 0.99% |

| AUM | $633.3 million |

| 30 Day SEC Yield | 4.61% |

| Inception | 8/14/23 |

Source: YieldMax

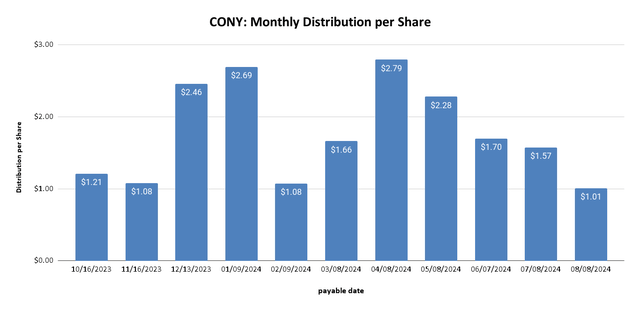

For an actively managed fund, the 1% gross expense ratio isn’t terrible. For instance, the previously mentioned GraniteShares 2x Long COIN ETF has a 1.1% expense ratio. The 30-Day SEC Yield is nothing to sneeze at but that yield is far from predictable. In fact, the general trend in the fund’s distribution has been down the last several months:

CONY Distribution, rounded to penny (YieldMax, Author’s Chart)

At just $1.01 per share, last month’s distribution was the lowest since the fund was launched a year ago. This wouldn’t be as big of a concern if the price of the fund itself was stable. That has not been the case.

Fund Performance

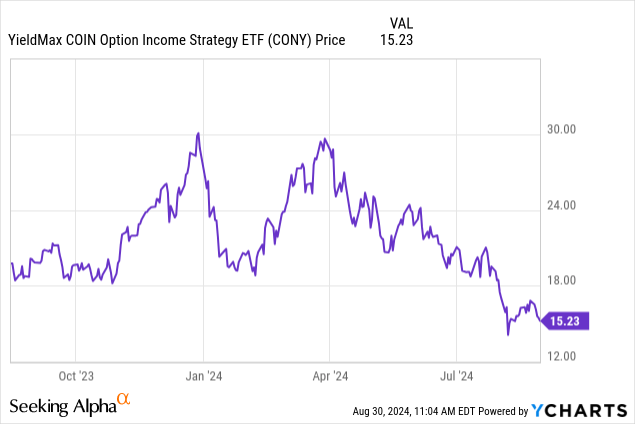

The value of shares in CONY has been cut nearly in half from the peak earlier this year:

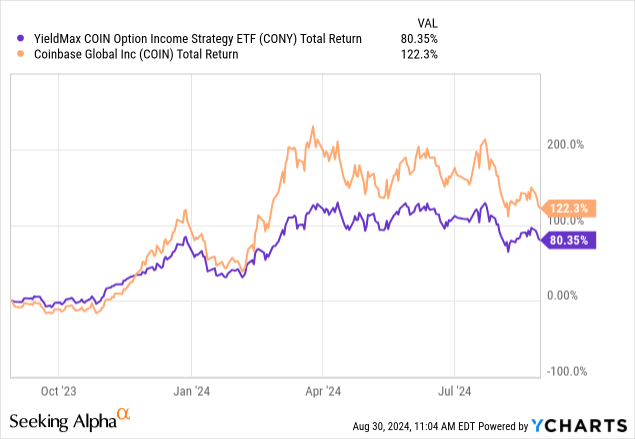

In a way, this is somewhat by design because the fund’s distributions have been so large in previous months. The more appropriate way to judge CONY is by total return. Yet, even here we see a potential issue:

While 80% is certainly nothing to sneeze at in a single 12-month period, the total return of the fund has underperformed the stock that it’s designed to provide synthetic long exposure to. And this is if CONY longs have been holding the ticker for 12 months. For CONY shareholders who bought the fund at the highs in COIN stock, it’s difficult for me to see a benefit to this strategy:

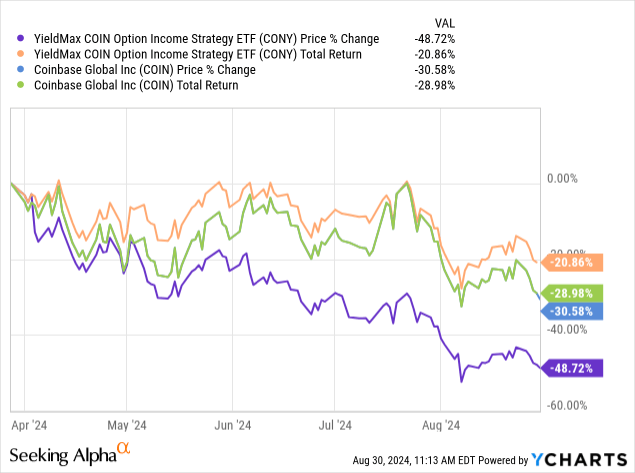

In the chart above, I’m showing COIN against CONY since the end of March. The total return for CONY is admittedly less bad than that of COIN at just 21%. But I’m still scratching my head as to why anyone would do this instead of just buying Coinbase directly if they want long exposure to the company. The total return for CONY underperforms the stock when it rises and still goes down when it falls. If you expect the name to fall, you wouldn’t want CONY exposure either. And I don’t think the fall in COIN is over yet.

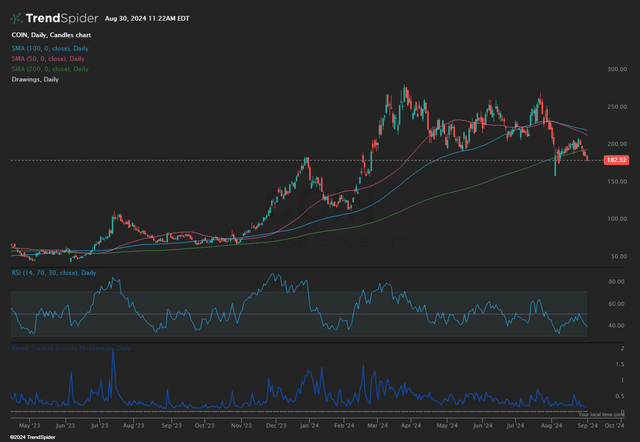

Coinbase Chart and Valuation

I try not to make my Seeking Alpha articles too TA heavy. But this is not a very good-looking chart to me:

COIN Daily Chart 8/30/24 (TrendSpider)

I see a stock with 50 and 100 day moving averages curling lower toward the 200. I see a stock that just fell below that 200 and now seems destined to revisit the early-August lows of $161 – indicating 10% downside from current levels. And I see a stock that has virtually no interest from the retail traders who would be theoretically more likely to put a bid on the name through calls indiscriminate of valuation.

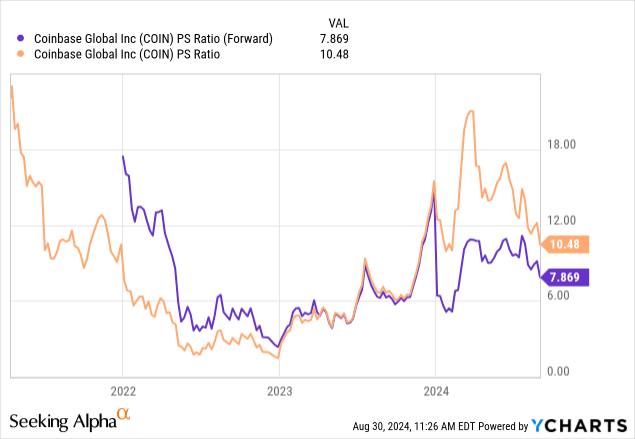

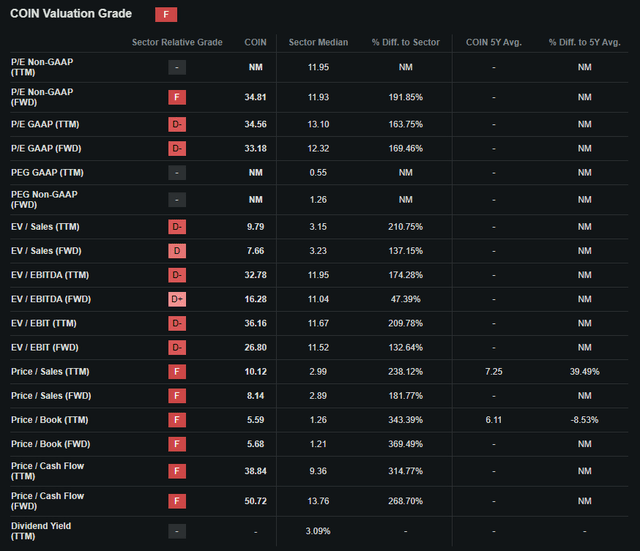

Speaking of which, COIN’s valuation is way too high, in my opinion:

10x trailing twelve months and 8x forward sales is not cheap in the financials sector and is, frankly, indicative of a stock that could very easily get cut in half and still be overvalued. As I mentioned in my CONL article from earlier this month, COIN has the “F” valuation grade from Seeking Alpha and either a “D” or an “F” in every individual metric:

COIN Valuation 8/30/24 (Seeking Alpha)

Final Takeaway

If CONY harkens to the Selena Gomez scene in The Big Short to you, you are not alone. Perhaps calling CONY a ‘derivative of derivatives’ is an oversimplification as the goal of the fund is to ultimately return value to shareholders through distributions. It’s just that the way those distributions are produced potentially carries more risk than from simply longing the stock directly if you’re bullish COIN. In my view, income investors will do better generating returns from stable, predictable investments rather than playing the ponies with synthetic long strategies in cryptocurrency exchange stocks. I believe CONY is an avoid.

Read the full article here

")