By Jeffrey Bailin, CFA & Aram Green

Small Caps Start Comeback, But Challenges Persist

Market Overview

The third quarter saw a reversal of an enduring period of large cap and growth leadership, relative to smaller cap and value stocks. The latter had a torrid July, initially catalyzed by higher odds that Donald Trump would regain the White House following the first debate and an attempt on the former president’s life. While the election odds dramatically shifted after Vice President Harris subsequently won the Democratic nomination, cooling inflation data supported a view that the long-awaited interest rate cutting cycle was imminent. Markets were buoyed by the Federal Reserve deciding to lower benchmark rates by a greater than expected 50 basis points at its September meeting. Broader macro datapoints, while mixed and suggestive of anemic growth in large swaths of the economy (the consumer, housing/non-residential construction, industrial production/manufacturing), have been solid enough to sustain hopes of a soft landing.

The benchmark Russell 2000 Growth Index was up 8.41% in the quarter, lagging the Russell 2000 Value Index (+10.15%), but exceeding the Russell 1000 Growth Index (+3.19%). Some of the strongest performance in the benchmark came in areas like biotechnology (+11.38%), lower quality (i.e., no sales, low return on equity) and the lower-size tiers of the small cap market.

Against this backdrop, the ClearBridge Small Cap Growth Strategy (MUTF:LMOIX) underperformed its benchmark in the third quarter. In prior rotations, the initial reaction, often catalyzed and enhanced by ETF flows, is a rally for low-quality stocks in which active managers struggle to fully keep pace. This occurred in the fourth quarter of 2016, following Trump’s election victory, and the fourth quarter of 2020, sparked by COVID vaccine clarity. Over subsequent quarters, as the small growth asset class garners momentum, we believe a fundamental, quality and long-term approach is well-positioned.

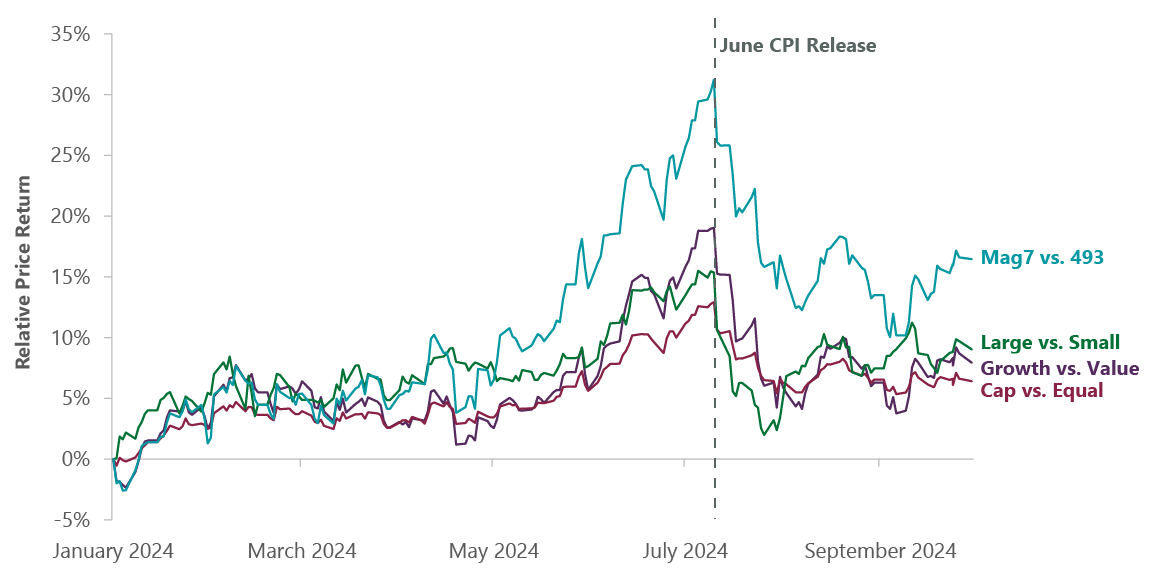

Exhibit 1: Rotation Has Begun

| Data as of Sept. 30, 2024. Sources: S&P, Russell, UBS, and Bloomberg. Note: Mag7 vs. 493 is the UBS Mag 7 relative price return vs. UBS S&P ex Mag 7; Cap vs. Equal is the S&P 500 relative price return vs. S&P 500 Equal Weight; Large vs. Small is the Russell 1000 relative price return vs. Russell 2000; Growth vs. Value is the Russell 1000 Growth relative price return vs. Russell 1000 Value. |

This pattern looked to be on display in the third quarter of 2024. Despite strong performance from a handful of new additions to the portfolio, underperformance was driven by focused leadership in the benchmark (biotech, smaller cap, lower-quality names with no sales and bond proxies like real estate) as well as a handful of portfolio holdings exposed to weakening consumer spending.

We are encouraged by the high proportion of positive returns on new ideas added over the last five quarters of elevated new idea generation, with solid contributions to overall performance despite their representing a modest portion of the Strategy’s assets. We have made progress on developing new ideas in biotech, with strong performance from some of our initial investments in the area as we manage the risk from biotech’s increased weight in the benchmark. We have seen success in high-potential, earlier-stage companies like Vaxcyte (PCVX) and Insmed (INSM), as well as commercial stories with multiple pipeline candidates like Mirum Pharmaceuticals (MIRM), offering some offsets relative to our underweight in a period of biotech outperformance. We continue to identify further potential investment opportunities in the segment.

Looking at recent top detractors, a key theme has been a pressured consumer. While much of the top-down macro retail and consumer datapoints have been benign, underneath the surface we believe there are signs that several years of robust inflation and spending have taken their toll, particularly on low-income consumers and in big-ticket categories. We see evidence of in a decelerating cosmetics market, anemic home renovation spending, restaurants declining to take price and a notable shift to a narrow set of value-oriented channels (i.e., Walmart or Amazon.com).

This has been reflected in weakness in a variety of holdings with direct or indirect exposure to the consumer. We’ve heard discussions from our management teams of a more selective consumer who is allocating spend more thoughtfully, deferring certain purchases and being more selective around where that shopping is occurring. These pressures have shown up in portfolio holdings exposed to higher-ticket purchases like TREX (large decking projects), automotive/leisure vehicle markets (Fox Factory, Allegro MicroSystems), potentially deferrable purchases like eyeglasses (National Vision) and general low-income consumer spending destinations (BJ’s Wholesale Club). For several of these challenged stocks, there has been no change in competitive differentiation, unit economics or long-term growth potential and as such we are willing to hold positions through the tougher macro environment. In instances where we do not see a visible medium-term path for management to drive improving results, or where competitive dynamics, profitability or capital allocation priorities have changed, we have trimmed or made plans to exit positions.

On the positive side, the Strategy continued to see strong contributions from stock picking in the financials sector, with a variety of business models executing at a high level. Companies like Hamilton Lane (HLNE) and Shift4 Payments (FOUR) are executing on idiosyncratic growth levers in secular growth markets, while PJT Partners (PJT) will benefit from a more robust M&A environment amid lower rates. Additionally, multiple investments in the software sector are showing differentiated growth against a difficult backdrop, with unique platforms, such as Zeta Global (ZETA), Klaviyo (KVYO), Varonis (VRNS), Intapp (INTA) and OneStream (OS) contributing positively.

It is worth noting that, following the annual Russell rebalance, SuperMicro Computer (SMCI) left the benchmark this quarter and promptly saw its share price decline 49%. Pressure on the shares arose from concerns around the dilutive impact of AI server margins and the accompanying cash burn, market share loss and a trifecta of accounting and corporate governance issues. These very issues were at the heart of our due diligence on the stock throughout 2023.

Portfolio Positioning

We continued to deliver strong new idea generation, adding four new investments in the quarter: OneStream (through participating in its IPO), Abercombie & Fitch (ANF), Wintrust Financial (WTFC), and FTAI Aviation (FTAI).

- OneStream is a horizontal software company focused on back-office solutions for the office of the CFO. With a largely organically built platform offering, selling to the enterprise and competing against a variety of entrenched legacy providers, OneStream offers best-in-class growth and ramping profitability.

- Abercrombie & Fitch is a global retailer with two primary brands, A&F and Hollister, providing apparel and accessories targeting millennials and Gen Z, respectively. Following multiple years of mis-execution, the company has repositioned its brands for durable growth, rationalized its store footprint, and is growing profitably with a nimble, fast-follower fashion strategy.

- Wintrust Financial is a Chicago-based bank that has successfully grown organically and through modest M&A over its history, branching out into Wisconsin and Michigan. Wintrust stands out with a leading niche premium finance business which is a short-tail, low-credit-risk asset class. With a strong management team and favorable local competitive positioning, the business maintains attractive intermediate-term growth potential.

- FTAI Aviation is an aerospace company that offers both engine and aircraft leasing services, as well as an aftermarket for engine products and services. With a focus on several widely used and aging engine platforms, the company’s differentiated modular approach to aftermarket products, along with the unique assets from its leasing business, offers meaningful revenue and earnings growth potential.

Early in the third quarter, portfolio holding Envestnet (ENV) announced that it was being taken private by Bain Capital (BCSF) and as such, we exited our position. We exited several other stocks, some for market capitalization considerations following the Russell rebalance (i.e., Monolithic Power), as well as Calavo Growers (CVGW), Cryoport (CYRX), National Vision (EYE), Iridium Communications (IRDM), nLight (LASR) and Inari Medical (NARI) due to idiosyncratic fundamental considerations.

Outlook

The ClearBridge Small Cap Growth Strategy remains committed to identifying idiosyncratic companies with growth opportunities and attractive returns irrespective of the macro backdrop. The guiding principles that have also informed our investment process and philosophy remain at the core of our process to exercise “judgment and patience” to ensure that we have 1) the right balance of opportunity and risk in the Strategy and 2) appropriately capitalized investments with substantial intermediate- to long-term growth opportunities.

Volatility and reversals remain the norm thus far in 2024, although the third quarter appeared to signal that, at least for the U.S. economy, inflation has cooled, while the labor market has remained just healthy enough to support the start of the long-awaited rate-cutting cycle. There is continued optimism that the economy might see a soft or “no-landing” scenario, although we are mindful of risks from the upcoming U.S. election and a set of fraught geopolitical conflicts. Historically rate cuts have been positive for small cap stocks, and with earnings growth for smaller caps set to eclipse that of their large cap brethren over the next two years, coupled with historic lows in relative valuations, conditions are aligning for better asset class performance. We are encouraged by a firmly positive hit rate on new ideas added over the last five quarters and believe the Strategy has an appropriate balanced spectrum of growth businesses.

Portfolio Highlights

The ClearBridge Small Cap Growth Strategy underperformed its benchmark in the third quarter. On an absolute basis, the Strategy posted gains across six of the nine sectors in which it was invested (out of 11 sectors total). The primary contributors to absolute performance were the financials, information technology and health care sectors, while the detractors were the consumer staples, energy and consumer discretionary sectors.

Relative to the benchmark, overall stock selection and sector allocation detracted from performance. In particular, a lack of investment in the real estate sector as well as stock selection in the consumer staples, consumer discretionary, industrials and health care sectors were the largest detractors to performance. Positive stock selection in the financials and IT sectors provided a partial offset.

On an individual stock basis, the leading contributors were positions in Hamilton Lane (HLNE), Zeta Global, Shift4 Payments, Surgery Partners (SGRY) and Vaxcyte. The primary detractors were e.l.f. Beauty (ELF), Progyny (PGNY), PagerDuty (PD), Medpace (MEDP) and Trex.

Jeffrey Bailin, CFA, Director, Portfolio Manager

Aram Green, Managing Director, Portfolio Manager

|

Past performance is no guarantee of future results. Copyright © 2024 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance source: Internal. Benchmark source: Russell Investments. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and/or Russell ratings or underlying data and no party may rely on any Russell Indexes and/or Russell ratings and/or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication. Performance source: Internal. Benchmark source: Standard & Poor’s. |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here