")

")

By Grace Su & Jean Yu, CFA

Sustainability Improvers Rise in Broadening Rally

Market Overview

Global markets surged in the fourth quarter, as disinflationary data, renewed hopes of an economic soft landing and declining bond yields in the U.S. and Europe overcame concerns over renewed hostilities in the Middle East and continued economic challenges in China. The benchmark MSCI World Value Index returned 9.3% for the quarter. A dovish policy pivot by the Federal Reserve helped to spur growth stocks ahead of value stocks, with the MSCI World Growth Index returning 13.3% versus the 9.3% return of the MSCI World Value Index.

While a fourth-quarter rally in the U.S. and Europe was driven by the belief that the central banks are done with raising rates and an easing cycle will be forthcoming, Asia Ex Japan was the top performing region in the benchmark thanks to strong returns in sectors leveraged to economic re-acceleration. Japanese stocks also continued their upward trajectory, though fears over a strengthening yen capped the rally. Lastly, performance in the U.K. was mixed, as strong performance in domestically-oriented stocks was offset by underperformance in more global sectors such as energy and health care.

Despite the market rally, positive sentiment was not universal. The fourth quarter also saw the outbreak of war in Israel and reprisal attacks on cargo ships in the highly trafficked Red Sea, resulting in elevated investor fears of a deteriorating geopolitical environment in the Middle East and a detrimental impact on global supply chains as ships were re-routed to safer, albeit longer, shipping channels. On the other side of the globe, the Chinese market continued to make new lows for the year as economic data continued to disappoint and failed to restore market confidence despite a myriad of measures rolled out by Beijing aimed at re-igniting the domestic economy.

Against this backdrop, the ClearBridge Global Value Improvers Strategy outperformed its benchmark in the fourth quarter, as strong stock selection and an overweight allocation to the industrials sector overcame our underweight allocation to the information technology (‘IT’) sector and headwinds to our holdings there.

The industrials sector saw robust performance from both secular growers as well as cyclical beneficiaries. Secular grower UBER Technologies, a ride hailing leader, and Vertiv (VRT), a data center electrification solution provider, continued to deliver earnings upgrades and saw their share prices re-rate. Japanese conglomerate Hitachi (OTCPK:HTHIY), having now successfully completed its transition from a dependance on heavy industries and tech hardware to IT services and energy, has re-entered a growth phase that has delivered strong earnings over recent quarters. We believe the company will continue to benefit from strong secular growth in its energy business as power grid modernization and renewable energy projects continue to accelerate, which should lead to upward movement as its share price and intrinsic value converge.

“We expect returns to broaden and include more of our improvement stories in 2024.”

Improvement in the overall cyclical outlook also propelled several other industrial holdings higher. Siemens (OTCPK:SIEGY), the global leader in electrification and industrial automation, saw new orders stabilize, indicating dissipating destocking headwinds, while enthusiasm over a soft landing alleviated demand concerns. Siemens continues to innovate and expand its offerings in power infrastructure and industrial automation, efforts that are increasingly influential in helping its clients reduce their carbon emissions.

With much of our industrials overweight currently being funded by an underweight in the IT sector, the tech rally in the fourth quarter proved the largest headwind to relative performance as many of the longer-duration tech stocks in the benchmark outperformed our holdings. While we remain vigilant for opportunities in the sector, the relative scarcity of investments that meet our criteria of being sustainability improvers while also having attractive valuations has proven challenging. In contrast, industrials continue to prove a fertile ground for stocks exposed to decarbonization and material recycling, where these opportunities have largely yet to be appreciated by the market. We expect these allocation decisions will result in some performance deviation from the benchmark over short periods, but the performance opportunities this positioning offers should allow the Strategy to generate attractive performance over a full market cycle.

From a regional standpoint, stock selection in North America and Japan were the greatest contributors to relative performance. Our U.S. holdings performed stronger than the broader market, helped by utility AES and Wells Fargo (WFC), in addition to Uber and Vertiv. Conversely, stock selection in the U.K. detracted from performance. This was largely due to CNH Industrial (CNHI), which has continued to suffer concerns surrounding the agricultural downcycle, and AstraZeneca (AZN), which delivered disappointing results on one of its pipeline products.

Portfolio Positioning

We were largely pleased with our positioning during the quarter and used opportunities to refine our positioning by adding one new holding.

We added a new position in NextEra Energy (NEE), an integrated electric utility business with a regulated utility operating in Florida and the world’s leading producer of wind and solar power. The company slowed its renewable growth outlook in late September and collapsed almost 30% in less than a fortnight. We saw this as an opportunity to invest in an excellent combination of a regulated utility and an experienced renewable operator with good long-term growth. Even at a reduced growth rate from higher financing costs, which we believe are likely to prove conservative in hindsight, we estimate the intrinsic business value to be materially higher than its current market price. NextEra exemplifies the type of sustainability reformer that we are looking for as it increases the proportion of renewable generation in its business mix, replacing fossil fuels with zero-emission wind, solar or other clean power sources, such as nuclear.

We also exited one position in the quarter, automaker General Motors (GM). Our original thesis postulated that General Motors would be able to leverage its extensive investment in EV designs and manufacturing to become a global EV leader in decarbonizing the auto industry. However, as competition has intensified, we believe the viability of General Motors’ strategy has become less clear and the company has cut its EV production targets multiple times, failing to deliver on our sustainability key performance indicators. As such, we elected to exit the position in favor of other, higher-conviction opportunities.

Outlook

The past few years have been challenging for ESG investors due to a strong rally in the energy sector following the outbreak of war in Ukraine in 2022, followed by the underperformance of clean tech in the face of rapid rate hikes over the last year. This unpredictability of macro and policy risks highlights the importance of maintaining portfolio exposure to a diversified set of ESG factors and is particularly important as the market has priced in a hopeful outlook for 2024 including better real income growth, less constraints from rising rates, margin upside from input disinflation, and a return of accommodative monetary policy.

While the last year’s market return was largely concentrated in mega cap growth stocks, we expect returns to broaden and include more of our improvement stories in the coming year. Rapidly declining inflation in the context of healthy economic growth and a strong labor market also provides a favorable market environment for value sectors overall as the Fed put is back on the table. Meanwhile, the valuation spread of value stocks relative to growth, as measured by large cap value spreads, is at historic highs.

We continue to see interesting opportunities across all three segments of the portfolio:

- Enablers are typically companies whose products enable greater energy efficiency and lower natural resource use by other companies across different sectors

- Reformers are typically companies actively improving their sustainability profiles

- Promoters are typically companies making an impact on sustainability by advancing the 17 United Nations Sustainable Development Goals (UN SDGs)

Many of our holdings, particularly in the enablers and promoters segments, enjoy secular growth tailwinds from mega trends such as infrastructure spending and the energy transition. Further implementation of the Inflation Reduction Act (‘IRA’) should be a structural growth driver. If the Fed eases monetary policy, these stocks should also benefit from declines in cost of capital. We also maintain high exposure to cheaply valued reformers, believing that potential rate cuts would favor discounted valuations. Our energy and materials holdings, which are investing to decarbonize, are good examples of this as strong profitability and capital discipline are allowing these companies to return significant amounts of capital to shareholders even as underlying commodity prices remain range bound. Lastly, utilities, especially ones with large renewable exposure, sold off precipitously last year, as higher interest rates cast doubt over their business model. As our constructive stance toward NextEra Energy suggests, the market’s overreaction to the increase in rates underappreciates the strong demand outlook and the resilience of these long-term, contract-based business models.

From a geographic perspective, we see attractive opportunities in key players involved in the energy transition on both sides of the Atlantic. Although the upcoming U.S. presidential election has raised investor concern over a potential repeal of the IRA if the Republican nominee wins, the fact that Republican states benefit the most from IRA-related job creation significantly dampens these risks. In continental Europe, the end of industrial inventory destocking could improve the cyclical outlook and allow for greater funding for the energy transition. The other large contrarian opportunity we see is the U.K., where Brexit and the cost-of-living crisis in recent years have deterred investor interest. However, as real wage growth and consumer confidence continue to improve, it is a market that could play catchup. Lastly, we are looking for opportunities to add to our Japan exposure as the economy exits the deflationary era and governance reforms likely serve up improvement stories. As always, the goal is to build a diversified portfolio of stocks where we believe risk/reward is mispriced and significant alpha generation is possible.

Portfolio Highlights

The ClearBridge Global Value Improvers Strategy outperformed its MSCI World Value Index benchmark during the fourth quarter. On an absolute basis, the Strategy had gains across nine of the 10 sectors in which it was invested (out of 11 sectors total). The industrials and financials sectors were the main contributors, while the energy sector detracted.

On a relative basis, overall stock selection benefited performance while sector allocation effects detracted. Specifically, stock selection in the industrials, utilities, communication services and materials sectors as well as an overweight to the industrials sector positively contributed. Conversely, stock selection in the IT, consumer discretionary and health care sectors, an underweight to the IT sector, a lack of exposure to the real estate sector and the Strategy’s cash position weighed on performance.

On a regional basis, stock selection in North America and Japan proved beneficial. Conversely, stock selection in the U.K. detracted.

On an individual stock basis, Siemens, Vertiv, Hitachi, Uber and Wells Fargo were the leading contributors to absolute returns during the quarter. The largest detractors were General Motors, Chesapeake Energy (CHK), Unilever (UL), Gerresheimer (OTCPK:GRRMF) and AstraZeneca.

ESG Highlights

An Enhanced Internal Engagement Initiative

Engagement to drive positive change in public equities has been a longstanding part of ClearBridge’s investment decision making and active ownership. As a long-term shareholder with an average stock holding period of five years, ClearBridge has cultivated strong and lasting relationships with company management teams. With this unique position and decades of industry experience, we’ve taken steps to better structure, measure and communicate the progress and outcomes of key engagements, and in 2022 we launched an enhanced internal engagement initiative, Engage for Impact (EFI).

The initiative encourages targeted engagements that we believe have a strong likelihood of creating positive impact, which we define as the creation of long-term positive environmental or social outcomes for the benefit of all stakeholders in public companies: their investors — our clients — and their employees, customers, suppliers and communities.

While we believe our work can often influence significant improvement at the company level, we also recognize we are one of many shareholders working to create change. In many cases this collective voice is what ultimately leads to positive, real-world impact. As a part of this new initiative, investment team members develop specific “asks” or areas of improvement for priority target companies. Progress against these “asks” is then monitored and reported on over time.

As long-term investors, our company engagements can take place over a multiyear period. Therefore, throughout the course of the engagement, we track and categorize company progress by stages (Exhibit 1).

Exhibit 1: Engage for Impact Progress Framework

Source: ClearBridge Investments.

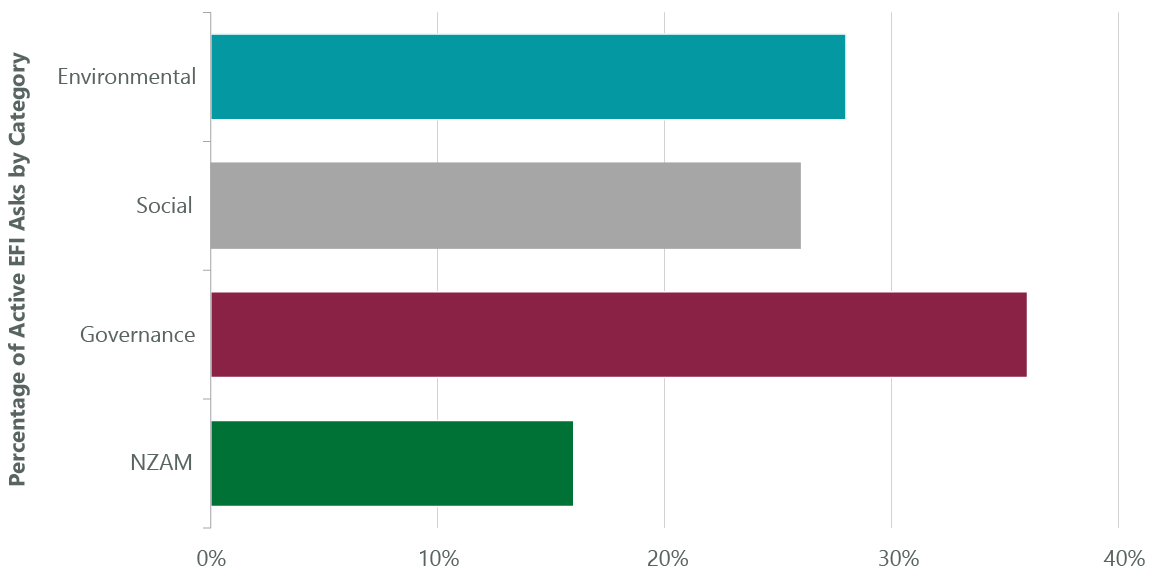

Using this framework, we can better monitor and track a company’s responsiveness and progress against key performance indicators and report on these outcomes over time. EFI engagements follow a consistent structure, prioritize topics closely aligned with value creation, represent a wide variety of sustainability topics (Exhibit 2), and are often rooted in firmwide focus areas like net zero, biodiversity, human rights, as well as diversity, equity and inclusion.

Exhibit 2: Engage for Impact Asks by Category

As of Dec. 31, 2023. Source: ClearBridge Investments.

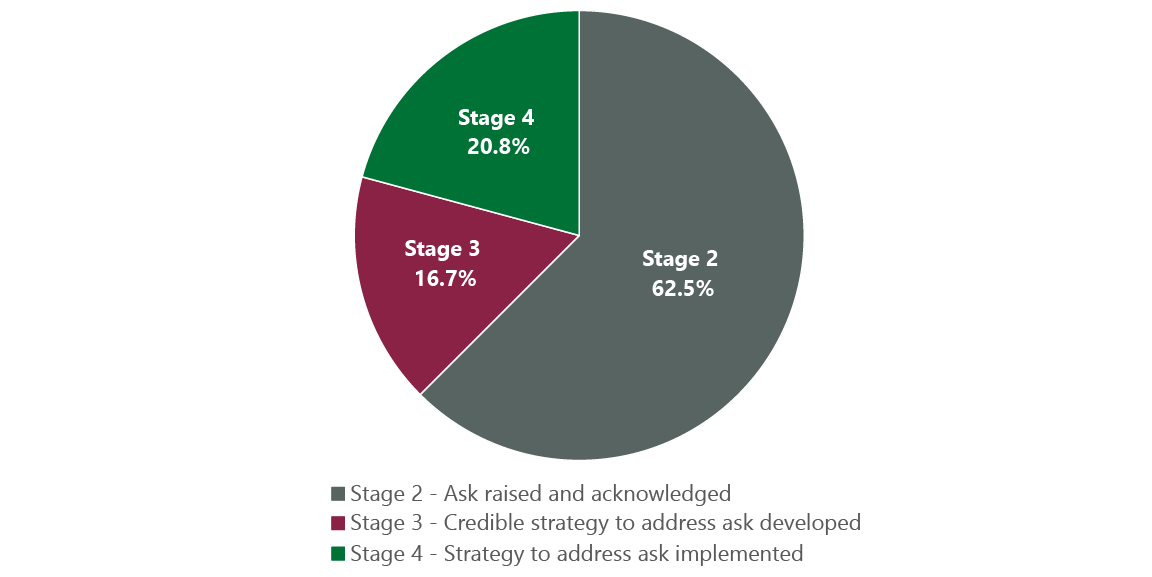

Given this enhanced initiative is still in the early stages, most of our EFI company asks are currently categorized as early stage or in-process (Exhibit 3). Examples of company asks focused on reducing emissions, improving labor relations, expanding electric vehicles (EVs), improving board effectiveness and implementing total shareholder return (TSR) metrics convey the spirit and overall benefits of the initiative.

Exhibit 3: ClearBridge Engage for Impact Asks by Stage

As of Dec. 31, 2023. Source: ClearBridge Investments. Stage 1 is not captured in the data because all EFI asks in the initiative have progressed past that stage.

Decarbonizing Aviation: United Parcel Service (UPS)

Reducing emissions is a common ask among ClearBridge’s company engagements broadly. For an EFI with United Parcel Service (UPS), we acted on the opportunity to formulate a specific ask for a reduction in Scope 1 and 2 emissions from its aviation fleet, which comprises ~300 planes. We actively engage with UPS on setting aggressive carbon reduction targets as its stock is held in a strategy that is in-scope for ClearBridge’s net-zero commitment.

In our engagements with UPS, we have discussed how due to heavy reliance on future technologies such as sustainable aviation fuel, the company recognizes it cannot credibly set a company-wide target approved by the Science-Based Targets initiative (SBTi) at this time. However, the company has acknowledged our ask as a key area of focus over the next 10-15 years and recognizes decarbonizing its aviation fleet is a key part of the global energy transition. It also recognizes the need to align all other parts of the business with a net-zero pathway in an effort to decarbonize. Efforts currently underway include investments in electrical vertical takeoff and landing aircraft and full electrification of its ground fleet, with a 2025 goal of 40% alternative fuel for ground vehicles, up from 24% today. We will continue to engage UPS as a stage 2 EFI to monitor progress against other reduction targets and continue to urge the company to decarbonize its aviation fleet.

Bettering Driver Relations and Expanding EVs: Uber

In stage 3 of an EFI the company has acknowledged the ask and has developed a credible strategy to address it. The company may even have begun and be well along in addressing it, as is the case with Uber and two asks we have formulated to: 1) improve driver satisfaction, and 2) expand its adoption of EVs toward achieving its net-zero goal.

We’ve engaged Uber since its IPO in 2019 as concerns over employee classification have led to questions of worker pay and benefits that we felt overshadowed other merits of its rideshare business, for example rideshare’s democratization of transportation and Uber’s impressive safety record.

In December 2019, we met with the company to discuss driver earnings and shared our view that drivers should remain contractors with added benefits and pay protection. At that time, Uber had already shifted its operating philosophy to a more conciliatory approach and improved relationships with contracted partners with guaranteed pay minimums, portable benefits and bargaining rights.

We continued the conversation as part of regular meetings with the company over subsequent years, and at a January 2024 meeting with Uber’s CEO, CFO and other representatives, we were pleased with progress made against both asks. Management highlighted improvements made to the driver experience, including technology, earnings and worker flexibility. Specifically related to driver earnings, the primary concern, drivers on the platform currently earn an average of ~$36 per utilized hour on a gross basis and low-$20s net of expenses and overhead. Up-front fares, which are now being rolled out globally, provide improved earnings transparency. On fairness, where drivers see anywhere from a 0% to 50% take rate (the percentage Uber takes of gross margins), Uber plans to share weekly reports with drivers clarifying take rates and distributing make-whole payments where appropriate.

To achieve its SBTi-approved net-zero goal by 2040, Uber is focusing on driver incentives and education to drive adoption of EVs across its platform. Results so far are promising and getting better: 4.7% of Uber’s trip miles driven in the U.S. and Canada are completed in zero-emission vehicles, even though EVs represent just ~1% of total cars on the road in the U.S.

Enhancing Board Quality and Operational Efficiency: Comcast (CMCSA)

Comcast is also at stage 3 in its EFI action as it is making measurable progress on EFI asks regarding 1) addressing some concerns from third-party governance research providers on overboarding and board effectiveness, 2) setting verified science-based targets and 3) addressing efficiency of operations, specifically as it relates to suppliers.

In December 2019, we engaged Comcast on a variety of ESG topics and raised the issue of board independence. We followed up in May 2020 when we discussed a proxy proposal on the split Chairman and CEO role. Following this meeting, Comcast improved the independence of its board, upping the percentage of independent director nominees from 80% in 2019 to 89% in 2022, as well as improving board diversity, from 40% of director nominees being diverse by gender or race in 2019 to 44% in 2022.

In December 2022, we continued the conversation around board effectiveness and engaged the company on its board structure, raising concerns around overboarding or having board members sit on too many boards, which may compromise their ability to serve the board effectively. This issue has been flagged by third-party governance research providers.

In a December 2023 engagement, Comcast shared that it was making progress addressing overboarding by bringing down the average tenure of its board by incorporating a policy on director overboarding into its corporate governance guidelines that limits the number of public company boards on which directors may serve. As part of the policy, no director who also serves as CEO at a public company may serve on more than three public company boards. A notable example is lead independent director Ed Breen, who is also the current CEO of DuPont de Nemours. He proactively sought to reduce the number of boards he sits on and chose not to stand for re-election to the board of International Flavors & Fragrances at the company’s 2023 annual meeting.

Also at our December 2023 meeting, Comcast disclosed its Scope 3 emissions for the first time and committed to setting a verified science-based target. The company has begun engaging suppliers on committing to set a verified target, and going forward, it will set clearer targets around Scope 3 emissions. Regarding our ask around operational efficiency, Comcast has reduced the electricity needed to deliver each byte of data across its network by 36% since 2019 and is pushing its suppliers to be more efficient.

Improving Incentive Metrics and Committing to Net Zero: Western Digital (WDC)

In a completed EFI journey, Western Digital has implemented a strategy to address asks we made over several engagements to 1) institute relative total shareholder return (TSR) incentive metrics to evaluate shareholder value creation compared to industry peers, 2) improve energy intensity levels of manufacturing in line with industry peers and 3) commit to a net-zero target.

Specifically, Western Digital reduced the energy intensity of manufacturing its products by >13% from FY21 to FY22. It added relative TSR metrics to its incentive comp, which we view as positive as it aligns management compensation with execution, whereas before management would benefit from the fact their industry is growing faster than the broader market. On the third ask, in June 2023 the company announced an ambitious target and has committed to net zero Scope 1 and 2 emissions across its operations by 2032. Its target includes goals to reduce Scope 1 and 2 emissions by 42% by 2030 and to reduce Scope 3 use-phase emissions/terabytes by 50% by 2030, both from a 2020 base year. Its targets were approved by SBTi in 2021, and since then Western Digital has achieved nearly 15% absolute Scope 1 and 2 emissions reductions.

We look forward to sharing more successful EFI case studies in the future as our EFI target companies continue to make measurable progress against our asks.

Grace Su, Managing Director, Portfolio Manager

Jean Yu, CFA, PhD, Managing Director, Portfolio Manager

|

Past performance is no guarantee of future results. Copyright © 2023 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance source: Internal. Benchmark source: Morgan Stanley Capital International. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance is preliminary and subject to change. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent. Further distribution is prohibited. |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")