")

")

Elevator Pitch

I rate CI&T Inc (NYSE:CINT) as a Hold.

There are both pros and cons pertaining to CINT’s attractiveness as an investment candidate, and this explains my decision to have a Hold rating awarded to the stock. CI&T’s current valuations are appealing, and the new AI platform could help to secure new client wins for the company. However, it is tough to ignore CINT’s meaningful customer concentration risk, and its exposure to Brazil which has an unexciting 2024 economic outlook.

Company Overview

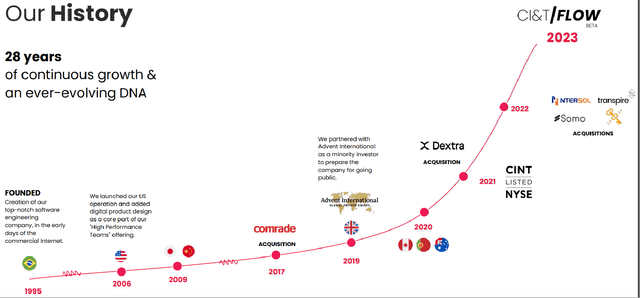

On the Investor FAQs page for its corporate website, CI&T describes itself as “a provider of strategy, design and software engineering services to enable digital transformation” that was started in “Campinas, Brazil” three decades ago.

CINT’s Key Corporate Milestones

CI&T’s Investor Presentation Slides

CI&T’s Selected Client Case Studies

CI&T Investor Presentation Slides

As disclosed in its Q3 2023 earnings presentation, CINT derived 29%, 20%, and 18% of its 9M 2023 revenue from the financial services, consumer goods, and technology & telecommunications industry verticals, respectively. The retail & industry goods, life sciences, and other industries contributed the remaining 12%, 11%, and 10% of CI&T’s top line, respectively for 9M 2023.

CI&T has been growing its multi-million Brazilian reais (or BRL) client base over time. The number of customer accounts generating yearly revenue in excess of BRL1 million for CINT increased by +27% YoY from 147 as of end-Q3 2022 to 187 at the end of September 2023.

Substantial Exposure To Brazil Is A Short-Term Headwind

CINT highlighted in its FY 2022 20-F filing that customers based in Brazil represented 44.6% of the company’s FY 2022 top line. It is pretty reasonable to think that CI&T’s business performance is closely linked to the economic outlook for Brazil.

Reuters published the results relating to its survey of economists in the second week of this month in a recent January 22, 2024 news article. The survey results pointed to consensus expectations of the Brazilian economy’s GDP growth slowing from 3.0% last year to 1.6% this year. Separately, Brazilian media publication Valor International’s latest economic poll conducted towards the end of the previous year suggested that GDP growth for Brazil is projected to moderate to between 1.0% and 2.5% in 2024.

The market sees Brazil achieving modest economic growth for the current year as evidenced by the results of surveys presented above, and this dim view of the Brazilian economy is reflected in CINT’s consensus financial forecasts. In specific terms, CI&T’s revenue is estimated to increase by just +2.2% in FY 2024 based on consensus data obtained from S&P Capital IQ.

Client Concentration Risk Materialized Last Year

CI&T’s significant exposure to the Brazilian market isn’t the only factor contributing to the weak revenue growth prospects for the company.

The consensus FY 2024 top line forecast for CINT was revised downwards by -24.6% in the past six months. This is most likely linked to CI&T’s disclosure at its Q2 2023 earnings briefing that “a budget replanning of our top client” led the company to reduce its full-year FY 2023 revenue growth guidance from +13%-17% in mid-May 2023 to +4%-8% in mid-August 2023.

It is worthy of note that the proportion of sales contributed by CI&T’s largest customer decreased from 15% (source: FY 2022 20-F filing) for full-year FY 2022 to 10% (source: Q3 2023 earnings presentation) in the first nine months of the prior year.

At the company’s most recent Q3 2023 earnings call, CINT shared that it has “successfully on-boarded 40 new clients that are generating revenue exceeding BRL1 million” in the past year. Nevertheless, CI&T’s 10 largest customers still accounted for 42% of the company’s 9M 2023 revenue.

As such, it is understandable that the sell-side analysts are conservative about CI&T’s top line growth prospects, taking into account the downside risks associated with a high degree of client concentration.

New AI Platform Could Help To Retain Existing Customers And Win New Ones

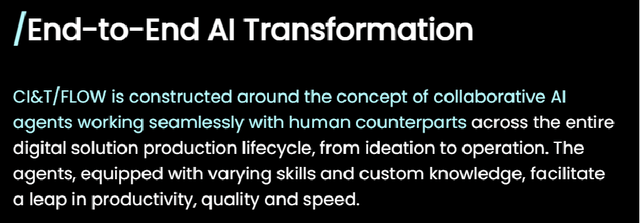

In July last year, CINT announced that it introduced “CI&T/FLOW, a new enterprise-grade AI platform” to the market that aims to “transform software and digital development workflows, accelerate productivity.”

The Value Proposition Of CINT’s AI Platform Known As CI&T/Flow

CI&T’s Corporate Website

The company shared at its Q3 2023 results call that “over 20 of our largest clients” and “more than 2,000 active users” have begun using the new CI&T/Flow platform. More importantly, CINT stressed at the most recent quarterly results briefing that the “early results (for the CI&T/Flow platform) have been very promising.” It is possible to infer that the new AI platform has delivered meaningful productivity improvements for its customers in the early stage of launch, considering CI&T’s recent management commentary.

In the preceding section, I touched on customer concentration risks for the company. Assuming that the CI&T/Flow platform is successful, CINT will be in a better position to keep its largest clients (improved value proposition with new platform) and also diversify its customer base by signing new deals. Beginning in 2024, CINT will open up the CI&T/Flow platform to new clients, after testing out the platform with key existing customers last year.

Valuations Are Attractive

CI&T’s valuations are reasonably appealing. The stock currently trades at 11.0 times consensus FY 2025 normalized P/E as per S&P Capital IQ’s valuation data.

The sell side is forecasting that CINT will register a revenue CAGR of +26.1% and a normalized EPS CAGR of +51.2% (source: S&P Capital IQ) for the FY 2025-2027 financial period. The bullish FY 2025-2027 consensus financial estimates are likely to have assumed the success of the new CI&T/Flow AI platform, a diversification of the company’s client base, and a stronger Brazilian economy.

Even if CI&T achieves just half of the expected intermediate-term earnings growth rate at around +25%, the stock’s low-teens P/E multiple still seems very attractive. As another comparison, CINT’s all-time historical mean P/E ratio was much higher at 25.3 times as per S&P Capital IQ data.

Concluding Thoughts

CI&T’s geographic and client concentration risks are significant. However these risk factors are already factored into CINT’s valuations to a considerable extent, and the company has a significant medium-to-long-term growth driver in the form of its new AI platform offering. A Hold rating for CI&T is warranted taking into account these different factors.

Read the full article here

")

")

")

")