")

Back at the start of July, Dane Bowler delivered a thorough review of Chimera Investment Corporation’s (NYSE:CIM) operations and detailed the opportunities that may exist in CIM’s spectrum of preferred equities. At the time, market conditions described that the preferred Series B (NYSE:CIM.PR.B) and Series D (NYSE:CIM.PR.D), which had recently converted to paying floating rate dividends, seemed to be the clear choice for total return. Later a couple of Labor Department reports, however, moved financial markets and interest rates significantly and, with that, each preferred issue warrants a fresh review.

The Fed Stands Pat in July, what will they Do Next?

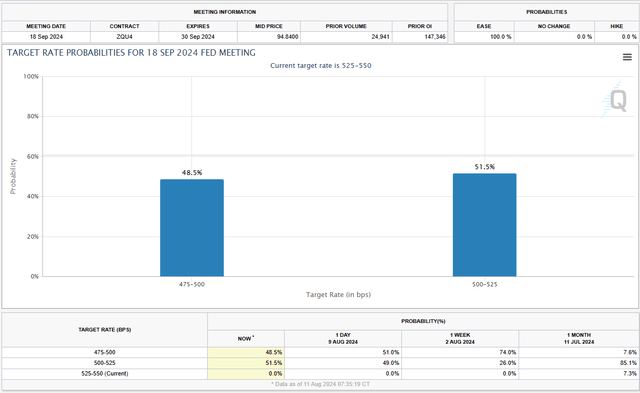

At the time of Dane’s last review, 10Y US T-Note and adjusted 3 Mo SOFR approximated 4.25% and 5.56%, respectively. In the interim, slowing employment and benign CPI reporting have raised speculation that the Fed will act decisively and cut rates to ease the restrictive stance of monetary policy.

CME Group

The result has led to increased volatility in stock and bond markets and significant reductions in interest rates.

S&P Global Market Intelligence

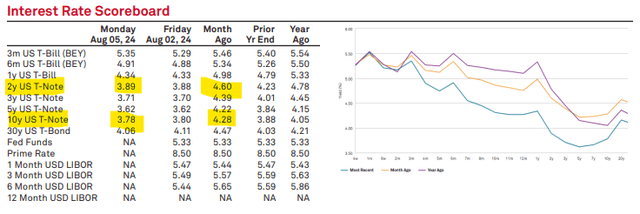

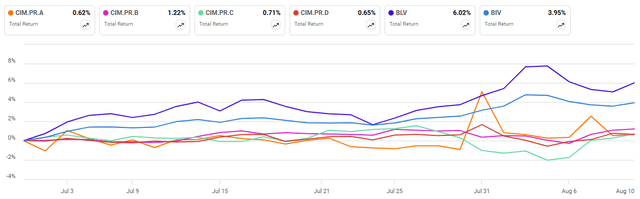

With 10Y T-Note yields declining by 50 basis points, related fixed income instruments rallied sharply, but the CIM preferreds’ pricing only moved slightly. The Vanguard Intermediate-Term Bond Index Fund ETF Shares (BIV) and Vanguard Long-Term Bond Index Fund ETF Shares (BLV) reflect yield change and the associated pricing in the bond markets. Because these CIM preferreds are all presently or soon-to-be callable, their peak pricing is tethered to their $25.00 par value liquidation preference price. The purpose of our exercise here is to see how returns might be affected by macroeconomic and market changes so that we can respond intelligently with new investment.

SA charting

The Degree and Pace of Interest Rate Changes Will Influence Returns

Since the July article, prices of CIM common and preferreds have drifted higher; the common shares are up on Chimera’s strong 2Q operating results, while the preferreds are likely higher on investors moving to lock in yields in anticipation of declining interest rates.

Portfolio Income Solutions

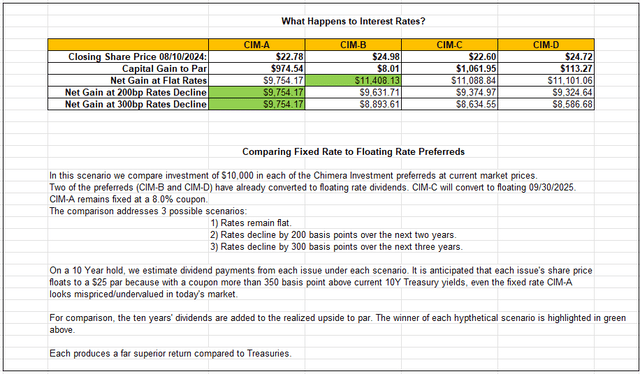

Our exercise is structured to measure likely results of a $10,000 purchase of each preferred at the 08/10/2024 closing price. We estimate results for 3 scenarios:

* No change in interest rates over the next two years

* 200 basis point reduction in Fed Funds rate over the next two years

* 300 basis point reduction in Fed Funds rate over the next three years

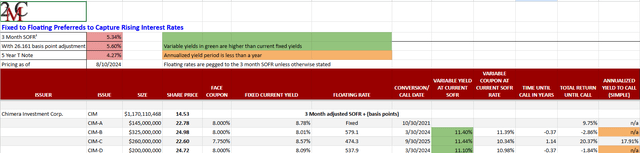

The test anticipates a 10-year hold, and the floating rate dividends are adjusted to mirror changes in the Fed Funds rate (which should be reflected in SOFR). The capital gain to par anticipates that each issue’s market price will approximate $25.00 in each scenario because even the fixed coupon CIM.PR.A at par produces a yield of more than 400 bp over current 10Y T-Notes.

2MCAC The above information is provided for illustrative purposes only.

The winner of each scenario is highlighted in green above. An investor’s decision will be steered by where she thinks interest rates are headed. The test comes up short in that it has a static, extended holding period which doesn’t accommodate variances in pace or extent of interest rate changes. That shortfall is somewhat mitigated by maintaining an active vigilance and presence in the market.

Action Plan

By its interest/yield paying nature, the fixed income portion of any portfolio always has new money to invest. With changes anticipated on the near horizon, an active/ready posture could be highly beneficial in today’s environment. If you believe interest rates are going to decline significantly, locking in high yields for the long run is a smart move. With the under-covered, liquidity-impaired arena of preferred stocks, you can not only lock in high yields, but do so at prices that have capital appreciation potential as well.

Our experience is that each of the Chimera preferreds has traded for prices that make it a superior choice to the issuer’s others. In switching to floating rates, the Series B and D currently pay yields in excess of 11%, but the capital gains opportunity does not exist when they are trading at par. The Series A and C trade for prices that deliver current yields in excess of 8.5% and still pose double-digit capital appreciation potential, but price matters.

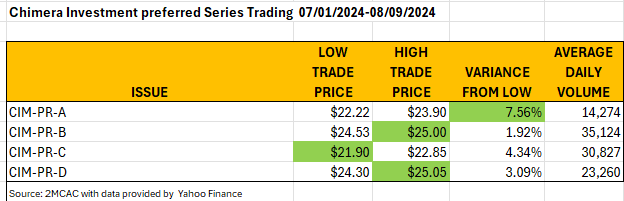

The table below details the trading activity of each of the Chimera preferreds since Dane’s article appeared in early July until August 9th’s market close. Though share volumes are low, some astute trader bought CIM-PR-A shares at an alpha delivering price of $22.22 (it wasn’t me). Just last week, shares of CIM-PR-C were purchased for as little as $21.90.

2MCAC

We currently hold shares in each of the preferreds that, we believe, were purchased advantageously at different points in the cycle. If interest rates do decline, each issue is headed for the same terminal $25.00 destination. Series B and D have already arrived. Series A and C offer the discerning fixed income investor an opportunity to lock in superior yield and potential appreciation.

While each issue is headed for the same $25.00 price, they will reach it at different times. Our scenario ran on a 10-year total return comparison. If interest rates decline even slightly, we suspect Series A and C will arrive at $25 trading within 24 months. At today’s pricing, the discounted Series A and C are superior choices for new money.

Be careful trading out there.

Read the full article here

")

")