ECTRIMS 2024 Investor Science Call Transcript")

")

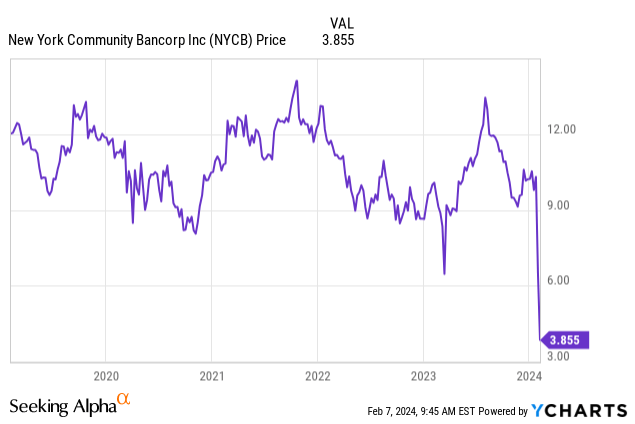

Nassau County-based New York Community Bank (NYSE:NYCB) shares plunged last week after the company announced a dividend cut and a Q1 loss. This week, the pressure ramped up as a chorus of Wall Street analysts issued downgrades. Yesterday, Moody’s cut NYCB’s credit rating to junk and warned of more downgrades, citing corporate governance and risks from commercial property. Worse, Bloomberg reported that the company’s chief risk officer and chief audit executive both resigned and that 30-day past due debt was up 48% quarter over quarter. NYCB stock has a few defenders as well, including analysts at BofA, and investors tempted by the low price of the stock. For their part, short sellers seem to have little interest in NYCB stock, with my latest data showing only 4% short interest or so.

What’s Going On With New York Community Bank?

New York Community Bank made decisions to grow rapidly over the past few years with acquisitions. Most notably, NYCB acquired a large chunk of the assets of failed Signature Bank (OTC:SBNY) during last year’s short-lived banking crisis. Before that, NYCB acquired Flagstar Bank, a large bank and mortgage servicer in 2022. NYCB made a series of huge bets, and more than doubled the size of its balance sheet since the pandemic.

Now, it’s turning out that these loans may not be so good. If you double the size of your bank in a short period of time, you’re taking a big risk. The risk here is that the roughly $105 billion liabilities are rock-hard for NYCB, but the bank’s reported $116 billion in assets are only worth what they are stated if the bank’s underlying assumptions about credit quality are sound. The worst of loans are made in the best of times, and I can personally attest from friends in the real estate business Signature Bank was known for making real estate loans that other banks wouldn’t touch. That’s likely part of why they’re out of business!

There’s a strong chance that NYCB will need to raise more money via bonds, and that just got a lot harder with Moody’s dropping the hammer on them with the credit rating downgrade. Bloomberg analysts have estimated the company’s credit needs in the $4-$6 billion range. This isn’t like last year’s banking crisis where depositors pulled money in a panic. NYCB put out an update showing that their deposits are solid, so that’s not an issue here. But credit is the issue here. A recent Goldman Sachs report stated that NCYB has heavy exposure to CRE with 56% of the bank’s total loans being commercial real estate loans. When you combine regulator concerns, resignations of key audit and risk personnel, a large increase in losses, and a rating agency downgrade, NYCB is probably going to need to be merged into another bank. For these reasons, I think buying the common stock could be like lighting money on fire.

If You’re Tempted To Buy NYCB, Buy Preferreds

One of the more thematic ideas I’ve found in investing is that the most public-facing way to invest in a company is usually the worst. Institutional investors are generally able to use corporate capital structure to protect their interests, and my research over the years has shown that junk debt far outperforms the stocks of junk-rated companies. Here, NYCB’s preferred stock (NYSE:NYCB.PR.A) is trading for $14.50 with a par value of $25. That’s good for a 9.5% yield. NYCB also has a second class of preferred shares (NYCB.PR.U) that I haven’t looked into as much, but the liquidity appears better in the A shares. If you know more about the U shares, share what you know in the comments!

Other banks in dicey situations have seen their preferred shares either wiped out (like First Republic) or saved (like PacWest). If the equity holders get anything at all, the preferred stockholders get par. Sometimes everyone gets wiped out, but buying preferreds for a deep discount to par effectively gives you a freeroll on the equity shareholders. A lot of times they’ll get close to wiped out and you’ll get paid off in full. This is still really dicey, but if you want to make a bet on NYCB surviving the current panic, buy the preferreds.

Will NYCB Spark A New Bank Crisis?

I doubt it. The Fed did an excellent crisis management job last year to quell bank run fears, and they can use a similar playbook this time around to reassure depositors. About a year has passed since last year’s flare-up and that means that banks that binged on duration before interest rates rose now have one less year of duration on their original bets to worry about.

I don’t think NYCB itself is going to unleash a domino effect of bank runs. The Fed’s implicit policy now is to protect bank depositors at all costs, and this is a policy that served them well in 2023 because it stopped people from pulling all their money out of the bank. Other countries have previously made this an unofficial or official policy as well, including Australia, Ireland, France, and Germany.

Also, I looked at the Federal Reserve’s weekly balance sheet where large new loans would be disclosed to banks, and I’m not seeing much in the way of emergency borrowing. What might happen, however, is that fresh scrutiny on banks causes more losses to be revealed at other banks in the commercial real estate sector, and then. I view this outcome as highly likely. Banks closing due to making bad loans and credit becoming less widely available is simply how the business cycle works, and that’s still coming down the pike after 14 years of 0% rates. So while I wouldn’t expect bank runs or anything crazy, I would expect bank failures to run well above average over the next 12-24 months, and for credit to continue to tighten.

Bottom Line

New York Community Bank stock has plunged following a week of terrible news. If you own the stock, I would take what you can get for it. If you’re tempted to bet on it, you’re more likely to succeed if you buy the preferred stock. Given how hard it’s going to be for NYCB to raise capital, I think the most likely endgame here is for NYCB to be bought out by another bank for a minimal price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

ECTRIMS 2024 Investor Science Call Transcript")

")

")