")

")

")

Q1 2025 Earnings Call Transcript")

")

Sometimes companies report extraordinary results, either extraordinarily awful giving shorts reasons to cheer or extraordinarily strong sending longs into enthusiastic exuberance. Cirrus Logic (NASDAQ:CRUS) just sent longs into the biggest celebration ever with its record December results. The company blew past guidance and analysts’ expectations. In the past, our articles, such as, Cirrus Logic In 2024 And 2025 Continued, focused mostly on future potential. This article focuses on the present and the importance of investor faith that with Cirrus Logic or other similar investments is essential. Unexpected reports come unexpectedly and, of most importance, to profit requires a reliance on informed faith. Otherwise, profits allude themselves. Shall we visit the celebration! It’s just next door.

The Quarter and Year

I believe the report blows away all expectations and worries, at least for now, with Apple (AAPL) and Cirrus. The next table shows guidance, analysts’ expectations and actual results for the last two quarters.

* Our estimate based on past Cirrus’ guidance history.

The December quarter revenue results blew away analysts’ estimates.

This next table summarizes other results from the quarter.

| Cirrus Quarter | Earnings (non-GAAP) | Margin | Tax Rate | Cash on Hand | Inventory |

| December | $2.90 | 51.2% * | 18.5% ** | $587M *** | $257 **** |

* One percentage higher than guided.

** Lower tax rate from 25% to 18% in the previous quarter, driven by an IRS definition revision. For the next three years, this rate should fall back into the middle teens.

*** In the past, Cirrus received cash for a previous quarter early in the next. If so, an additional $160M in cash from December is coming.

**** Inventory reduced from $353M.

Next, a table showing revenue and earnings for FY-2023 and FY-2024 follows.

In March of 2023, Cirrus earned $0.90 bringing the total to $6.30.

Our guess for March of 24 at $360M beats guidance and results in earnings of $360M times 0.51 margin minus $114M in non-GAAP expenses times an 18% tax rate divided by 55M shares, or roughly $1.00. Adding that with the above previous three-quarters, earnings for FY-2024 equals $6.4, unchanged year over year. Analysts predicted earnings in the middle $5s early last year. The difference is more than significant.

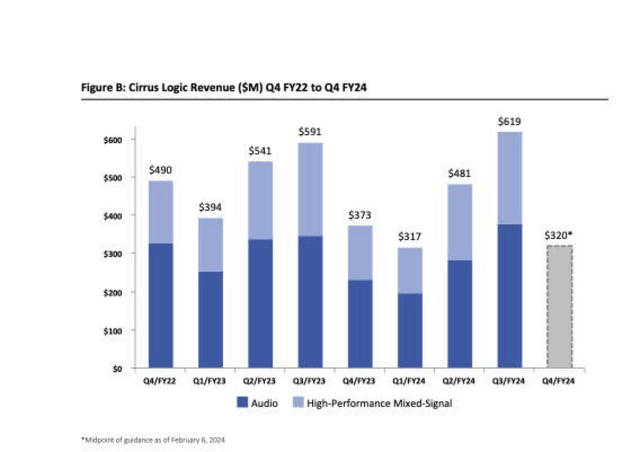

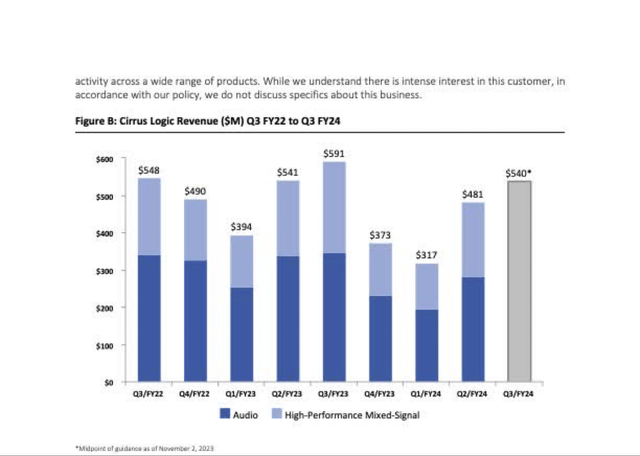

Defending our March revenue estimate, we included two revenue graphs located in Cirrus’ December Shareholder letter and September Shareholder letter. Cirrus most commonly guides its top end short, sometimes really short.

Cirrus Shareholder Letter Cirrus Shareholder Letter

Notice the change in the last revenue bar in September to the actual in the graph above it. Again, beats happen almost always driven by Cirrus’ guidance approach.

Estimating valuation is always important. With typical valuations for this type of technology company being in the 12-15 price to earnings ratio, Cirrus’ likely $6.5 in earnings at the high end calculates to $97. At the low end of 12 a slightly different approach seems fitting, 12 times $6.5 plus $10 per share in cash equals $88. A defensible price resides in the $90s. Future valuation certainly depends on growth, something that seems certain in our view, at least in ASPs.

Before the Report

Cirrus announced a reference design win with Microsoft (MSFT) and Intel’s (INTC) latest processor, Lunar Lake, scheduled for the 2nd half of 2024, the day before earnings. The reference includes a variety in possible content numbers for three Cirrus parts, Cirrus Logic CP9314 high-efficiency power converter, low-power CS42L43 SmartHIFI™ codec, and CS35L56 smart amplifiers.

In the list, Cirrus’ CP314 game changing power conversion offers significant advantages for battery powered devices. First, power conversion is different than management or charging. The battery voltage output is fixed, but the electrical components in mobile devices require several different voltage levels, thus these devices require step changes in voltages distributed on internal rails. The technology, based on Switch cap power conversion, is a mandatory function and can include two, three or more components per device. Management in the question/answer portion added,

“So it reduces the component count as well as really significantly increases the efficiency of the DC-to-DC conversion. So, your heat losses are much lower, you’re able to effectively get more done using less power drawn from the battery.”

This is a game changer in a potentially huge, yet to be determined market.

Discussions at the Call

Management and analysts openly discussed what could be interchanged about future growth drivers. Organized logically by Stifle, drivers include:

- 22m smart codec.

- Custom boosted amps.

- Laptop optimized products (audio, power/battery mgt.).

- Professional audio data converter,

- Camera controller.

- Augmented reality optimized products.

With respect to the new codec/amps, management offered this,

“And in terms of the overall content, we did talk about those four components that will have a newer generation compared to the prior phone model. So we’re pretty excited about the fact that we’re reducing the next generation of the codec and three instant stations for the next generation of the amplifier. And that’s what we expect will drive our performance in fiscal ‘25.”

Though clearly stated that an ASP increase is coming, management’s coy response on amounts leaves investors wondering. Is it bigger or less than might be considered?

On the camera controller, ASP increases this year come from greater product migration to the highest ASP product. In a coming year(s), a new camera control chip will be released with an even higher ASP than today’s offering.

On the PC markets, revenue growth begins first with a trickle in the latter half of the year, followed by massive potential.

Cirrus noted more detail on the headset market with an announcement that it is now shipping into a newly released (most likely Apple’s Vision Pro) product with two custom HPMS solutions. We believe that the two are camera and haptics solutions.

Cirrus isn’t telegraphing the amount of revenue growth in CY-2024 2nd half, but clearly is now expecting it. One sign supporting significant growth, after an eighty-person layoff in the company targeting bringing costs back in-line with business, shortly thereafter management reopened the employment door.

Charts

Understanding Cirrus, or for that matter any tradable entity, begs a look at the charts. We include four generated from TradeStation Security software.

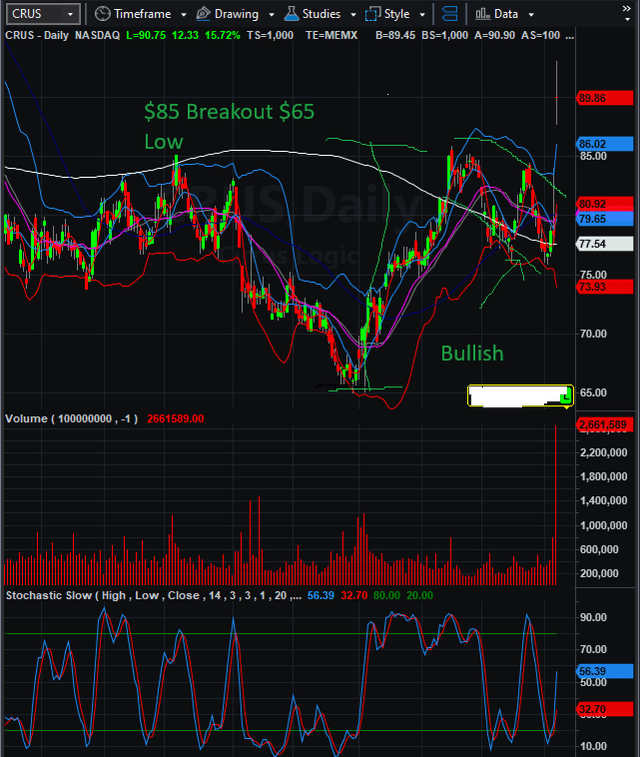

The first two charts are day bars, offering two different potentials.

TradeStation Securities

The above day bar looks at a shorter time view. The right-side pattern is a bullish consolidation before a breakout, which occurred the day after the extremely bullish report. The pattern move, $85 minus $65, the low, plus $85 suggests $105 in the future. The huge relative volume, red bar spike at the bottom, confirms the breakout.

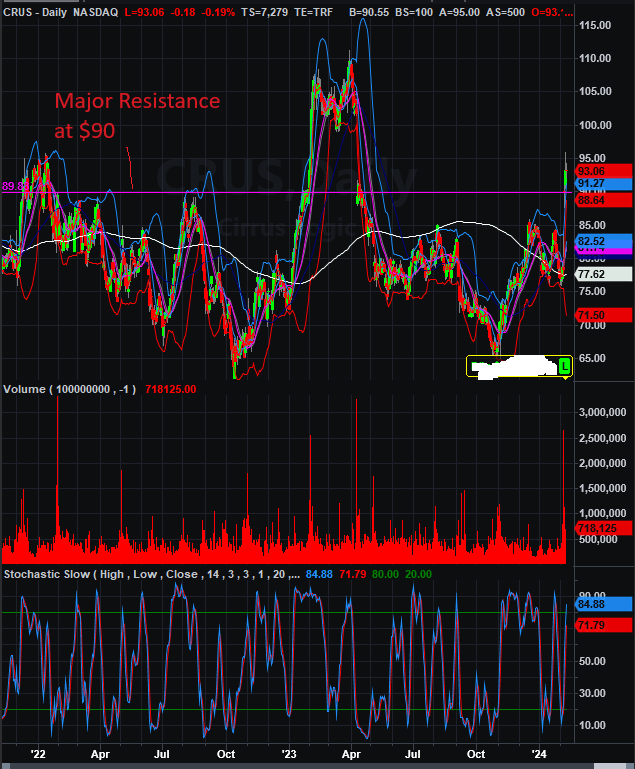

The next day bar looks at longer trends. In the past, $90, the magenta horizontal line, suggests that $90 is the major resistance point, once broken puts $90 minus $65 plus $90, or $115, in play.

TradeStation Securities

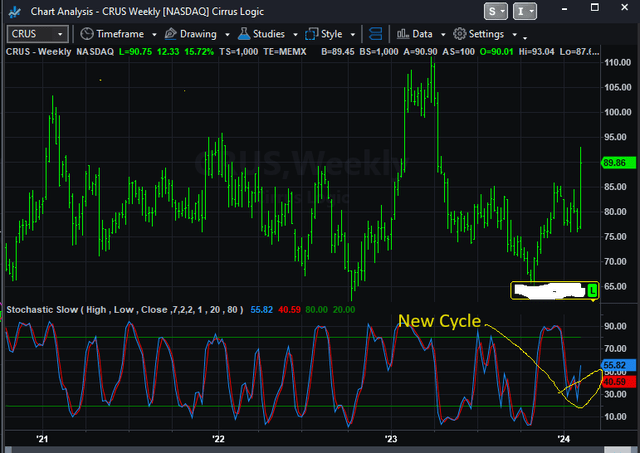

With regard to technical synergy, both the week bar, next, and month bar charts support the technical breakout. The weekly stochastic turned north, supporting a new upward cycle. A weekly cycle generally lasts between four to twelve weeks.

TradeStation Securities

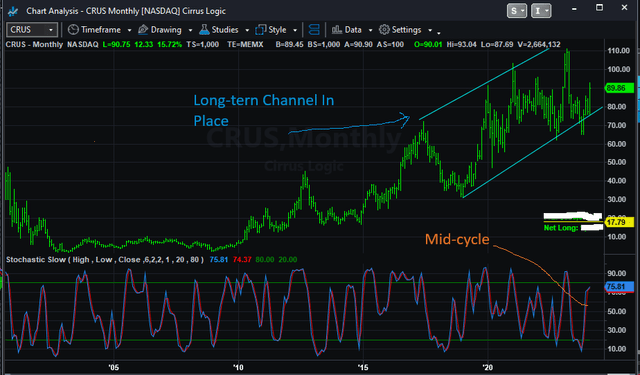

The last chart, monthly, included below, shows a stochastic at mid-cycle, still bullish, and the channel. At the top right, the two cyan trends mark the very long-term trading channel. The upper right price is just north of $120.

TradeStation Securites

The charts support upward movement, with day bars revealing breakouts at $85 and $90. In the near-term, prices at appropriately $100 are reachable. In the little more distant future, prices above $110 might be reached. Longer term, the channel suggests prices north of $120. Yes, we understand that fundamentals, in some form, must follow. Fundamentals, at least for a time (late 90s internet bubble as an example) may be nothing more than a story. In the case of Cirrus, we don’t think it is just about a story.

Risk

Risk from Apple unit sales did, and will continue, to exist. Ming-Chi Kuo claims iPhone 16 will badly fail in product improvements and thus experience meaningfully lower volumes. His thesis lacks credibility, in our view, claiming among other things, AI improvements in the new phone won’t be competitive. We know that Apple is working furiously on AI. Continuing, in trying to more fully disclose in total other recent comments, he also claimed December quarter iPhone sales in China would be down 20%-30%. That prediction was dead wrong. The real truth, in our view, is that Apple’s newest approaches will positively improve new AI and many other features. We just don’t know details nor how the market will react. And obviously, a recession might negatively impact unit volumes.

On recommendations and ratings, we began the article discussing that this is a prima facie case for if you don’t own it before the big news, you lose. For us, Cirrus is a buy on any weakness, prices near $90, a hold for prices near $100. This stock or other thinly traded stocks such as Calumet Specialty Products (CLMT) must be purchased on weakness and before news announcements in our opinion. When it comes, they move fast. We do expect Cirrus to hit $100 plus in the short-term and likely $120 longer-term depending on the ASP increase for the new codec series. Boy, the celebration is super fun, and we believe that more celebrations are in the works.

Read the full article here

")

")

")

Q1 2025 Earnings Call Transcript")

(NASDAQ:MU)")