")

")

Welcome to another installment of our CEF Market Weekly Review, where we discuss closed-end fund (“CEF”) market activity from both the bottom-up – highlighting individual fund news and events – as well as the top-down – providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the fourth week of January. Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

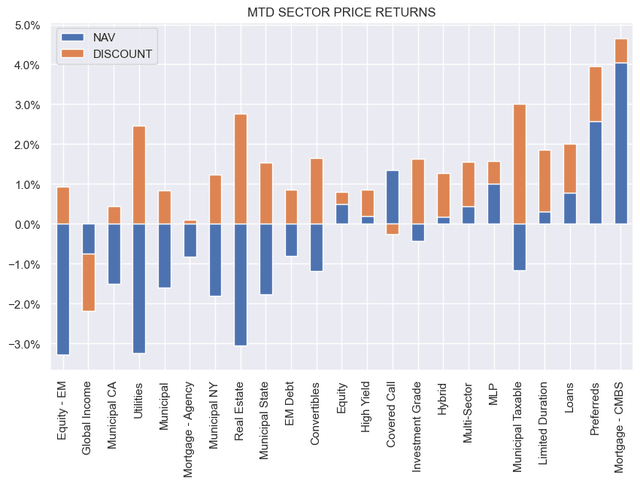

All sectors were up on the week with MLPs and Preferreds in the lead. Month-to-date, performance is more mixed, particularly for NAVs. However, discounts have tightened for all but two sectors, reflecting a strong level of risk sentiment.

Systematic Income

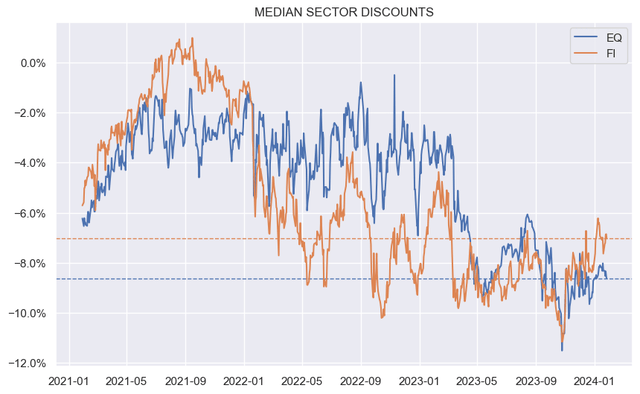

Fixed-income CEF sector discounts have come in around 4% off their recent wides with equity CEF sector discounts lagging.

Systematic Income

Market Themes

We had a discussion with a member about a discrepancy in total NAV returns of a particular CEF between the service, CEFConnect and SA. The key things to keep in mind is that CEFConnect shows returns up to the previous month i.e. if you were to look at the 1Y total return of UTG in January you would see that it only goes up to 31-Dec i.e. you’d be looking at the 31-Dec-22 to 31-Dec-23 return not one from yesterday to a year ago.

SA

The other thing to keep in mind is that many data providers including the one that powers SA do not do a good job with NAV ticker distributions and often these are missing entirely. This means that if you look at price and total price returns for XUTGX – the NAV ticker symbol for UTG – they are the same. They are, of course, not the same for the price ticker UTG as total return exceeds price return for any period that includes at least one distribution.

SA

When total NAV returns are calculated on the service what happens is that the distributions of the price ticker UTG are copied over to the NAV ticker XUTGX which then calculates total NAV returns correctly for the NAV.

Market Commentary

A number of fund families raised their distributions this month – a welcome change from the seemingly unending series of cuts across many funds last year.

MFS Muni CEFs – CMU, CXE and CXH – hiked by 4-5%. The distributions have been fairly volatile and they’re back to roughly what they were a year ago through several ups and downs.

Flaherty preferred CEFs – FFC, FLC, DFP, PFO and PFD – joined in and hiked the distribution by 1-5%. Flaherty funds tend to manage their distributions monotonically i.e. only hiking or only cutting over a relatively long period. This suggests that we have likely seen the bottom in these funds’ distributions.

Stance And Takeaways

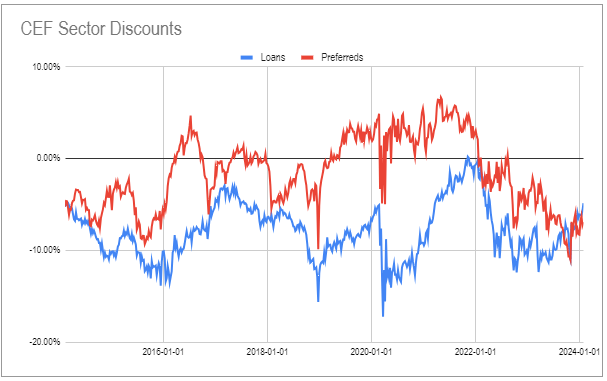

Sector valuations are beginning to catch up with the differentiated performance across many CEF sectors. For example, the significant outperformance of Loan vs. Preferred CEFs (20% total return differential over the last year) means that loan CEFs are now beginning to find favor. We can see that loan CEFs are now trading at tighter discounts on average than preferred CEFs – a fairly unusual dynamic historically.

Systematic Income

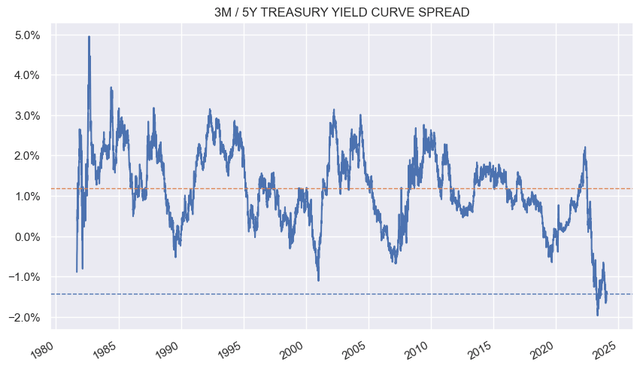

At the moment the yield curve still favors floating-rate assets. However, once it begins to flatten, it can make a lot of sense for investors to begin rotating out of floating-rate CEFs, particularly when distributions start to be cut, in order to be ahead of the eventual repricing wave which tends to follow rather than anticipate performance.

Systematic Income

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Check out Systematic Income and explore our Income Portfolios, engineered with both yield and risk management considerations.

Use our powerful Interactive Investor Tools to navigate the BDC, CEF, OEF, preferred and baby bond markets.

Read our Investor Guides: to CEFs, Preferreds and PIMCO CEFs.

Check us out on a no-risk basis – sign up for a 2-week free trial!

Read the full article here

")

")

")