")

")

Q3 2024 Earnings Call Transcript")

")

")

The REIT sector has experienced a small revival in the last quarter of 2023, following the Federal Reserve hinting that the hiking cycle is effectively over and 2024 will finally see interest rates actually decline. Although there is still a debate ongoing regarding how soon and how quickly rates will actually fall, it is pretty much a given that this is pretty good news for real estate companies. REITs must rely on debt in order to grow as real estate projects require a lot of capital to complete, therefore the sector has suffered a lot for the past few years. The Vanguard Real Estate ETF (VNQ), a good proxy for the REIT market as a whole, is up about 17% in the last 3 months, despite taking a break in the last couple of weeks as some investors probably took the chance to lock in some profit.

However, there is a sub-sector in the REITs world that for the most part was left behind. Residential REITs have recovered much less than other REITs, some of them in particular still trading at fairly depressed prices.

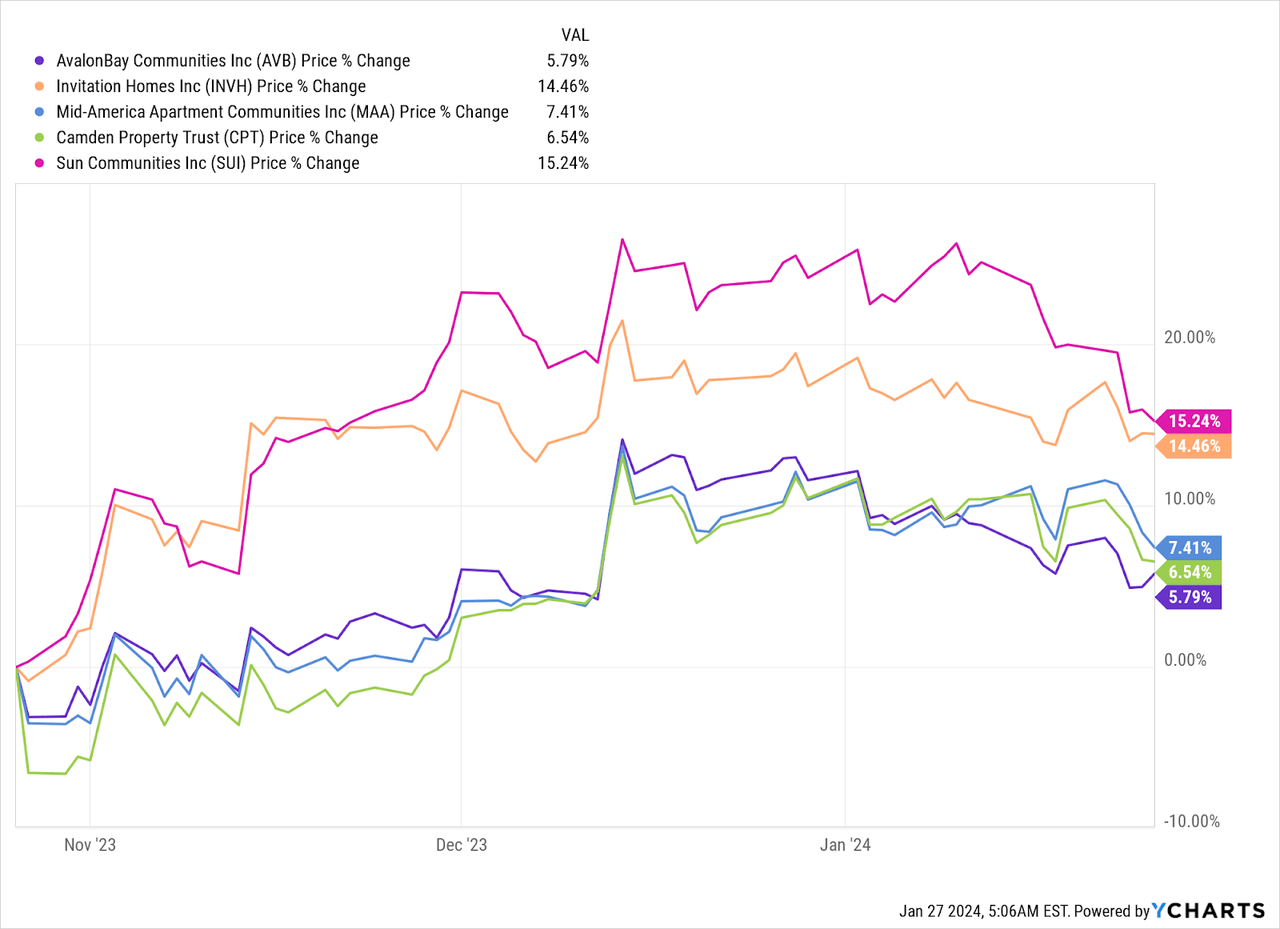

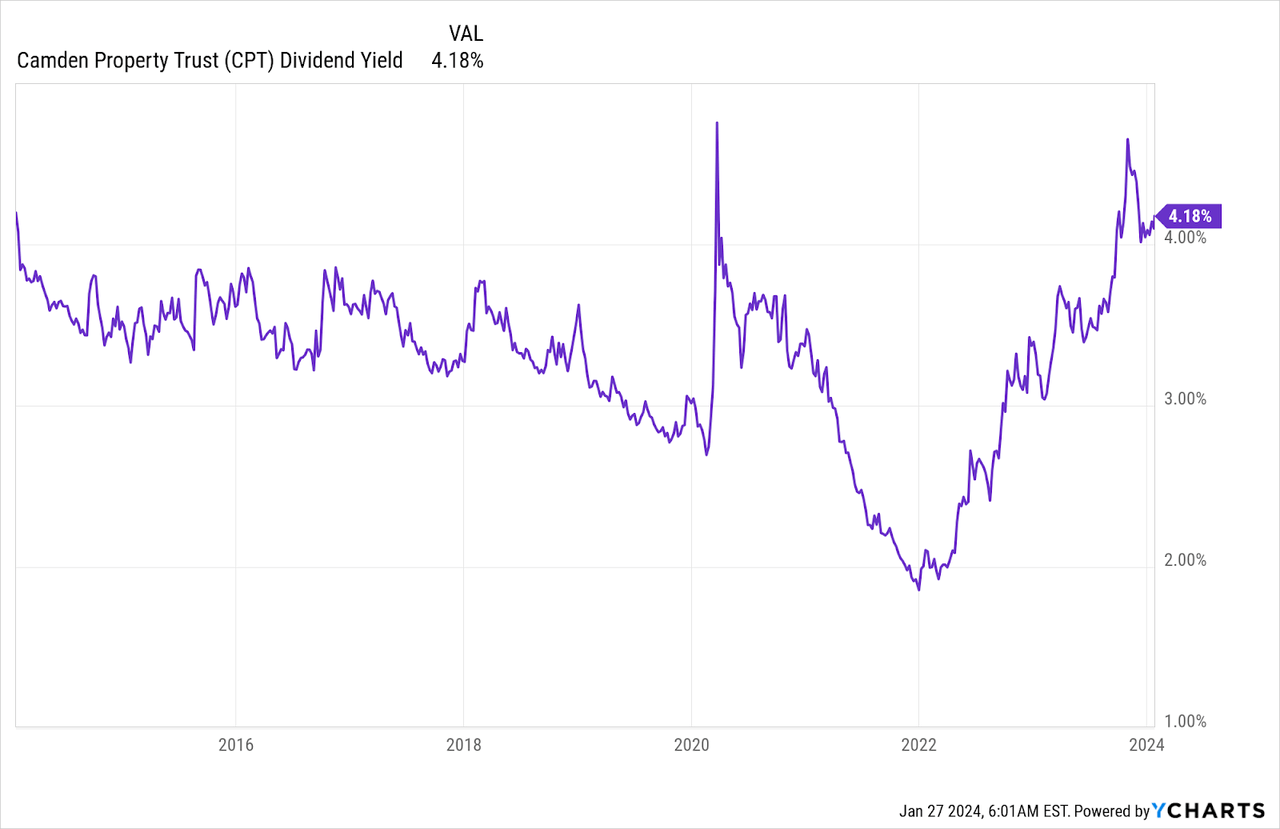

CPT has been a laggard compared to many peers (YCharts)

One example is Camden Property Trust (NYSE:CPT). The stock is still down nearly 50% from its all-time highs and currently provides a dividend yield of 4.1%. The company is currently facing headwinds primarily coming from higher interest rates and oversupply of housing coming in their markets; however, I believe these are temporary in nature and over the course of the next few years the company might experience a normalization. As a result, the stock might get repriced higher while investors still enjoy the steady flows of dividends.

2022 was a crazy good year, but it created problems

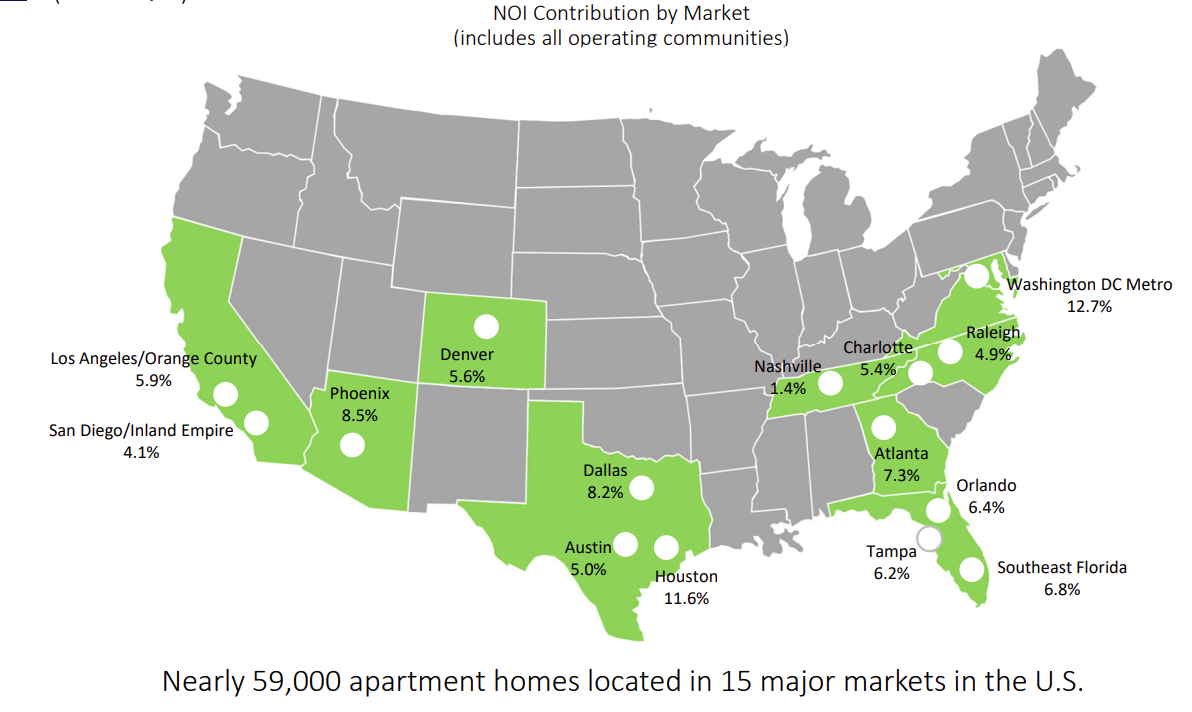

CPT residential portfolio (Camden Properties Trust Investor Presentation (3Q 2023))

Camden Property is focused exclusively on the Sunbelt region and owns apartment complexes. CPT went public in 1993 and over the decades has been one of the prime examples of the steady and reliable growth that investment vehicles such as REITs can achieve, with obvious caveats such as the Great Financial Crisis or COVID. Nevertheless, the company has seen relentless growth and has reached today over $10 billion in market cap and an impressive portfolio of high quality housing communities located in increasingly popular markets.

Multi-family residential properties are experiencing several structural tailwinds that should overall favour Camden going forward. There’s been an exodus of workers towards some of the states in the Sunbelt region attracted by good weather and possibly better tax advantages; rent demand is further bolstered by positive job growth and the historical unaffordability of housing for a lot of people who are then forced to rent for longer.

On the supply side it appears that new projects are slowing down considerably. The market during 2022 seemed to have focused a lot on potential issues derived from oversupply in the region, however management commentary during the latest quarterly conference call gave reassuring details on that regard:

On the supply side, starts have peaked and the capital markets hurricane has begun to reduce new starts. Annualized August starts fell 42%. Witten Advisors projects starts will fall to 250,000 units in 2024 and just above 200,000 units in 2025. Completions will be elevated through the end of 2024, but demand drivers should allow for an orderly lease absorption in our markets.

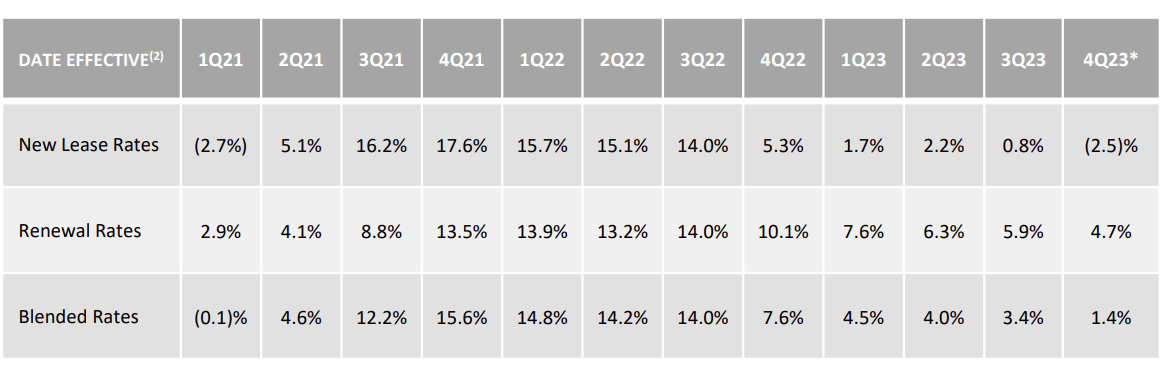

Camden has experienced incredible conditions during 2022 thanks to government stimulus, migration towards Sunbelt regions and tight housing supply, resulting in the best year in the company’s history according to management’s direct commentary. Despite this, the stock underperformed as the market was solely worried about the Federal Reserve’s hiking campaign as well as the oversupply issue. 2023 was, for the most part, the year of normalization from an operational point of view. The latest part of 2023 saw new lease growth trending negative (-2.5% in October) and management has also hinted that the number might further go down. However as previously mentioned, this comes from the backdrop of historical double-digit rent growth in 2022 and thus it can be interpreted as a normalization more than a deterioration. Occupancy rate across the company’s portfolio remains excellent at more than 94%.

New leases have exploded in 2022, but are now normalizing (Camden Properties Trust Investor Presentation (3Q 2023))

I think there are clear indications that both major headwinds (interest rates and oversupply) are starting to fade. As we already mentioned, the Federal Reserve has clearly signaled a change in strategy which already resulted in a better credit market (more of that later). The supply issue will still take time to resolve: although data suggest that new housing projects have significantly dropped in the Sunbelt region, those currently in construction will eventually get to the market during 2024 and early 2025. Management has estimated that 16% of Camden’s portfolio is affected by new competition in the multi-family field and that will most likely still take a toll on rent growth for 2024, although no official guidance was provided yet.

This issue is however temporary in nature if we are to believe that people will continue to move to these sought-after markets and jobs will continue to grow, which appears to be the case. With more and more people coming in, the new supply will be absorbed and the low number of new housing projects should mostly normalize the market by 2025.

Robust financial profile

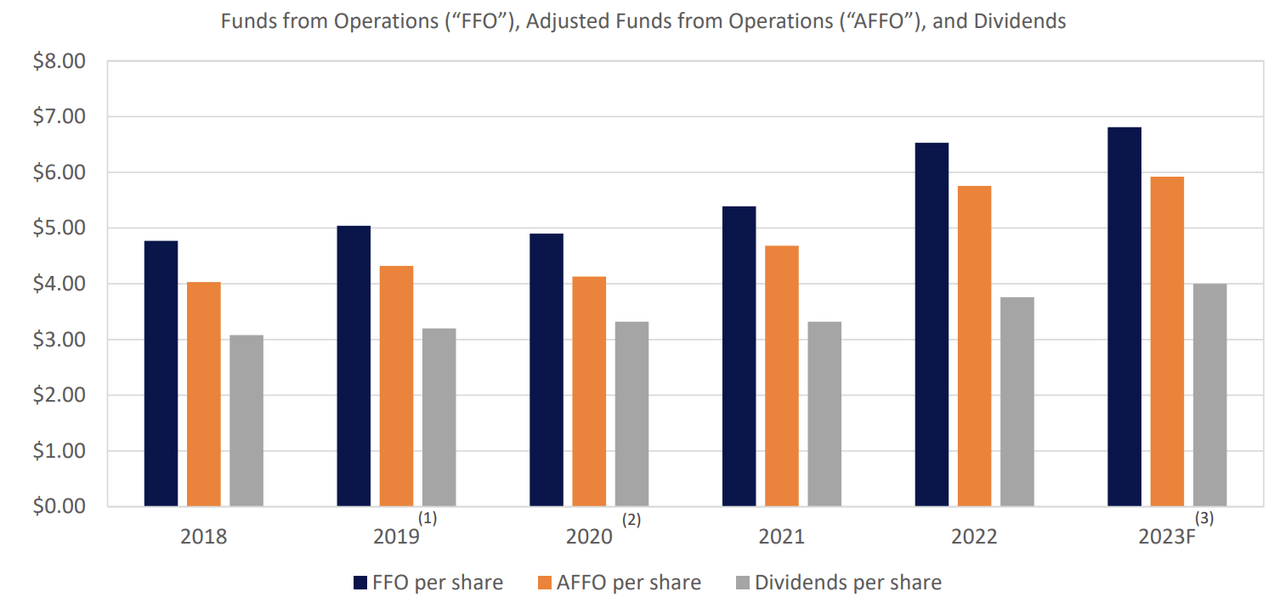

The company has achieved excellent operational results over the last years, constantly growing rent, earnings and consequently their dividend.

Constant growth over years (Camden Properties Trust Investor Presentation (3Q 2023))

So far in 2023 Camden Property has achieved about 5% revenue growth, while FFO per share should come in at about $6.81 per share, an increase of about 3.3%. In the TTM, the company has generated $1.5 billion in revenue and $749 million of FFO, while the debt profile is well managed as Net Debt to Annualized Adjusted EBITDAre stands at a reasonable 4.1x.

Currently the company pays a quarterly dividend of $1, for a yield based on current prices of 4.1%. The yield is also well covered as the FFO Payout ratio stands at just 57% currently. The yield is not tremendously high, however it is worth noting that this REIT has historically traded at significantly lower yield which might indicate a possible undervaluation. As in the last 10 years, the company had an average yield of about 3.3%, a normalization finalizing during 2025 might translate to roughly 20% stock appreciation.

CPT dividend yield in the last 10 years (YCharts)

The easing of the credit market might become a tailwind

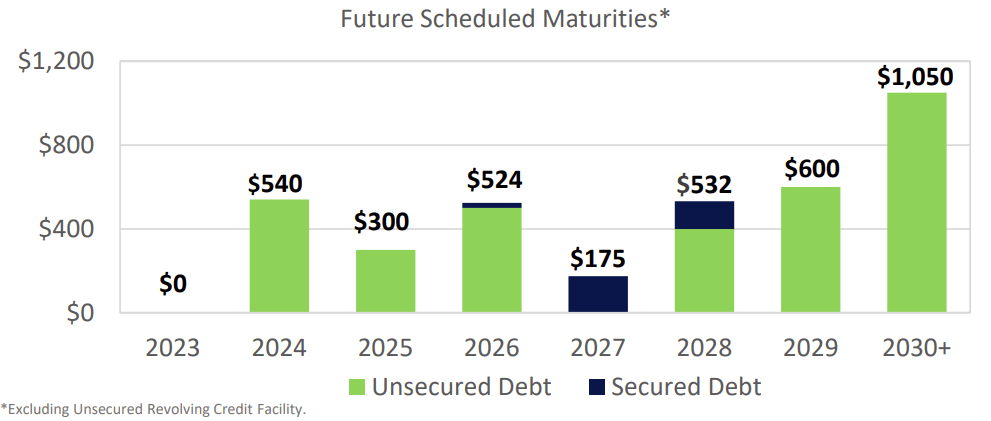

Camden Property currently holds $3.6 billion in debt, 77% of which is fixed. The weighted average interest rate of all the debt held by the company is 4.2% and its weighted average maturity is 5.8 years. As expected, the rise in interest rates has directly hit the company’s financials as interest expenses jumped from $97 million in FY2021 to the trailing twelve months figure of $130 million, an increase of about 34%. In reality, these expenses might rise further in the near future as the company has significant maturities in 2024, 2025 and 2026 ($540, $300 and $524 million respectively).

Future debt maturities (Camden Properties Trust Investor Presentation (3Q2023))

An example of the increase in interest expenses was the new 3-year unsecured notes issued in October 2023 at an interest rate of 5.85%, much steeper than the current company’s debt profile as highlighted above. However, just few months after in January 2024 the company raised additional capital by issuing unsecured notes maturing in 10 years at an interest rate of 4.9%. In my opinion, that is a very clear positive sign, indicating a general relaxation of the credit market in anticipation of the Federal Reserve’s pivot towards more dovish monetary policy. As the Fed will go forward with an actual cut to the federal funds rate, it is possible that the next rounds of refinancing done during 2024 and 2025 will result in a more normalized interest rate, similar to what CPT’s management was used to.

Additionally, a more hidden tailwind that might materialize as the Fed lowers their rates is that CPT kept a significant portion of their debt at a floating rate. Management has actually highlighted how that was a conscious choice as interest expenses were generally low anyway for a business of this size and when rates will go lower, the floating rate debt will allow interest expenses to go down in real time, directly flowing into increased FFO.

Key Takeaways

It is very interesting to see how COVID disrupted the residential markets in the Sunbelt region, from one side boosting demand and allowing CPT to realize their best year in record in 2022; on the flip side though, that has created clear headwinds as now the demand has moderated, but the craziness of the past couple of years has still pushed other companies into starting new residential housing projects that will affect the supply side of the equation, forcing Camden Property to lower a bit their rent for new leases.

However, I believe the oversupply issues will normalize slowly starting from 2025, while interest rates will most likely head down over the course of this year and probably into the next one as well. Once these headwinds disappear, what is left is a stable, growing company that is currently trading almost 50% down from their peak reached at the end of 2021. Granted, the stock’s valuation at the time got clearly out of hand and currently is not particularly cheap at a Price to FFO of about 14x. But the depressed price and the higher than normal dividend yield are clearly signaling that the market is discounting the temporary headwinds we talked about in this article.

I would not be surprised if CPT might start to get slowly repriced higher during 2024 once the narrative around oversupply and interest rate improves; ultimately, I see 2024 as a good entry point for investors looking to slowly accumulate CPT shares if looking for more exposure to the residential market recovery.

Read the full article here

")

")

Q3 2024 Earnings Call Transcript")

")