")

")

")

Cadence Design Systems, Inc. (NASDAQ:CDNS), a primary player in the electronic design automation, or EDA, market alongside Synopsys (SNPS), reported its Q2 earnings for FY2024 after the bell yesterday. We reiterate our buy-rating but update our investment thesis. We wrote on CDNS back in January, forecasting “the stock outperforming the S&P 500 and SOX index in 2024” on “more optimistic [view] about CDNS’ FY24 guidance as the semi-slowdown eases and WFE spending recovers in 2024.” Since our January article, the stock is up 9%, versus the S&P 500 (SP500) up 16%; our positive thesis of better wafer fabrication spend driving spend on chip design was premature for 2024 but remains at play for 2025.

We think the cyclical industry downtrend in the semi-industry stretched out into the post-inventory correction environment, hence delaying our positive thesis. In other words, the end demand from smartphone, PC, auto, and industrial, to name a few, failed to rebound even after built-up inventory was worked down and demand-supply dynamics balanced. This is the result of multiple factors to do with capital expenditure and a higher interest rate environment for longer, but where CDNS is concerned, this is in big part the result of what CEO Anirudh Devgan described on the earnings call as being “tied to the R&D spend more than the revenue of…customers.” We think chip design spend will go up as Wafer fabrication equipment spend rebounds, which should take place in 2025 to support the now AI-led semiconductor industry.

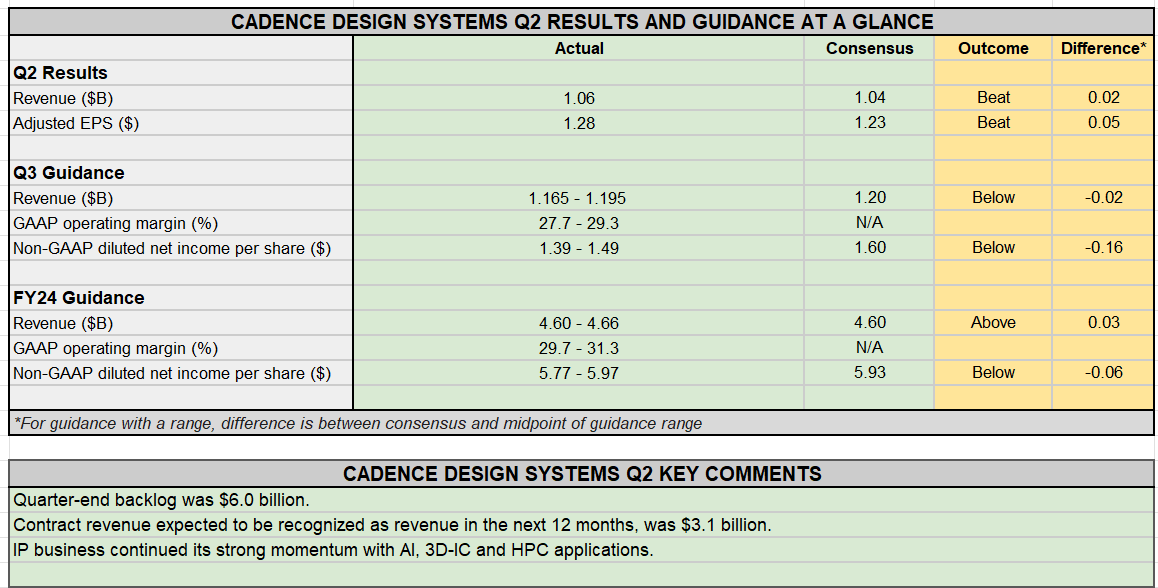

CDNS’ 2Q24 results beat estimates on top and bottom lines but fell short on guidance again. CDNS’ 4Q23 and 1Q24 results and outlook both triggered a post-earnings sell-off, as well, mainly on softer guidance. Last quarter, 1Q24, management guided for sales of between $1.03B and $1.04B, trailing consensus expectations of $1.11B. A quarter prior, in 4Q23, management’s guidance disappointed, forecasting $0.99B-$1.01B in sales versus a consensus of $1.09B. For the quarter reported yesterday, CDNS achieved revenue of $1.06B, ahead of consensus at $1.04B, and adjusted EPS of $1.28 versus expectations of $1.23.

This quarter, management’s guidance for Q3 was in the range of $1.165B to $1.195B, slightly below expectations and EPS of $1.39-$1.49, trailing consensus of $1.60. Non-GAAP operating margin was also forecasted to decline to the range of 40.7% to 42%. The softer outlook over the past three consecutive quarters and market sell-offs in reaction confirm that the negatives have been priced into both the stock and the outlook for FY24. We see a better FY2025 for CDNS as spend on chip design rebounds, and would recommend longer-term investors take advantage of the stock at current levels.

The chart below outlines CDNS’ results for the second quarter of FY24.

SeekingAlpha

Our buy rating on CDNS is now based on two factors:

The first is the expectation that better spending on chip design in 2025 will position CDNS better to beat guidance in 2HFY24. AI-driven demand for automation is a tailwind working in CDNS’ favor, in our opinion. CDNS and SNPS together make up ~70% of the EDA market, making both stocks uniquely positioned to benefit from upward WFE spending in 2025. The EDA market is estimated to grow at a CAGR of 10.5% between 2024-2025, and CDNS is well positioned with its customer base to benefit from what management described as “customers are ramping-up their R&D spend in AI-driven automation” through its Cadence.AI portfolio. CDNS’ customers include major semi-players such as Nvidia and Analog Devices, to name a few. We believe the company’s portfolio could enable it to gain “a little bit bigger piece of the pie from overall semiconductor, especially AI,” as described in the Q&A section on the call by Charles Shi.

And, the second is our belief that expectations have been revised down enough to enable a beat and raise in FY25. SA News noted the following on CDNS ahead of yesterday’s results:

“Over the last 3 months, EPS estimates have seen 0 upward revisions and 11 downward. Revenue estimates have seen 0 upward revisions and 11 downward.”

We think the negatives have been priced into CDNS’ outlook and market expectations for the stock, creating an attractive buy opportunity for longer-term investors.

Valuation & Word on Wall Street

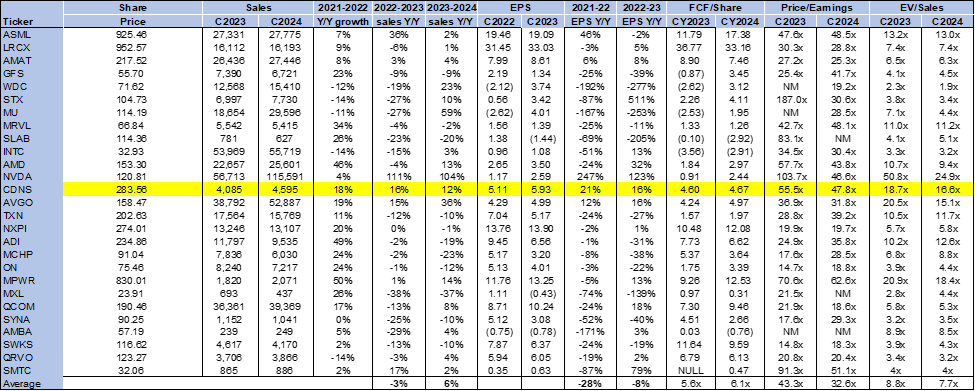

CDNS is trading at a premium multiple; the stock is actually trading above the semi-peer group average on both the P/E and EV/Sales ratio for C2024. On a P/E ratio, the stock is trading at 47.8x, compared to 43.9x in January and a peer group average of 32.6x. The stock is trading at 16.6x EV/C2024 Sales, versus 14.9x in January and the group average of 6.2x. We think the higher multiple is a result of the overall upward revision in earning expectations due to the AI hype, and CDNS is no exception to this. We understand investors’ concern about the higher multiple, but we don’t think this should cause investors to shy away from the stock.

The following chart outlines CDNS’ valuation against the peer group.

TechStockPros

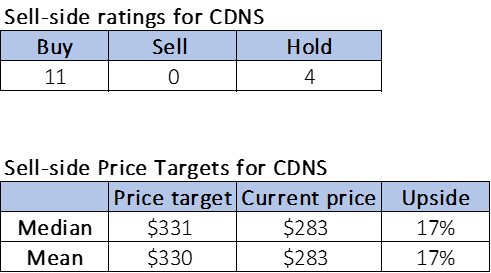

Wall Street analysts’ overwhelmingly bullish sentiment on the stock is also reflected in sell-side price targets hovering around $330-$331 per share, which represents a 17% upside from the current $283 per share. Of the 15 analysts covering the stock, 11 are buy-rated, and the remaining are hold-rated. The stock also has high institutional ownership, with 91% of its shares held by institutional investors, underscoring the momentum behind the bullish sentiment on the stock.

The following outlines Wall Street’s sentiment on the stock.

TechStockPros

What to do with the stock?

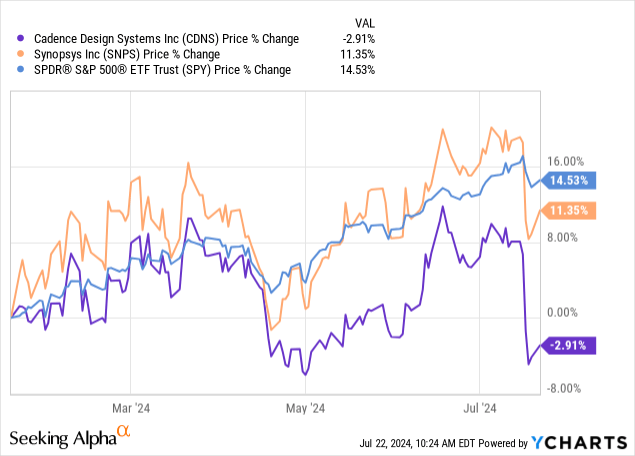

We like CDNS for longer-term investors, but SNPS remains our favorite pick among the EDA twins. The reason is its relative resilience during the industry downturn. CDNS and SNPS stock are closely correlated, but SNPS has proven to be more resilient; the chart below shows CDNS and SNPS against the S&P 500 over the past six months, with the former down ~3% and the latter up 11%, both underperforming the S&P 500 after the recent semi wide pullback last week.

YCharts

We think CDNS’ Intelligent System Design portfolio expansion strengthens its standing in the EDA market and will benefit it as we see spending rebound next year in reaction to a healthier demand market; management noted on the last earnings call the longer-term tailwinds from “hyperscale computing, autonomous driving, and 5G, all turbocharged by AI super-cycle, are fueling strong broad-based design activity.” CDNS provides a good buying opportunity at current levels and remains, alongside SNPS, a relatively resilient name. Management’s raised full-year guidance also foreshadows more potential upside in 2025; the company now expects FY24 revenue of $4.60B-$4.66B, raised from a previous forecast of $4.56B to $4.62B and $4.55B to $4.61B before that, while consensus is set for $4.59B.

We believe both management and Wall Street are being more conservative on Cadence Design Systems, Inc.’s near-term outlook after 1H24, and we think the stock is better positioned to outperform in 2025.

Read the full article here

")

")