")

BXP, Inc. (NYSE:BXP), which just changed its name last month from Boston Properties, covers its robust 6% dividend yield with funds from operations and has a well-leased office real estate portfolio.

Though the trust has a high asset concentration and is not as diversified as one would wish, BXP easily earns its dividend with funds from operations.

With a low payout ratio in the 50-percent range and a low valuation based on FFO, I think BXP offers passive income investors a durable 6% yield as well as a healthy risk/reward relationship.

Boston Properties: A Prime Office REIT With Strong Lease Metrics

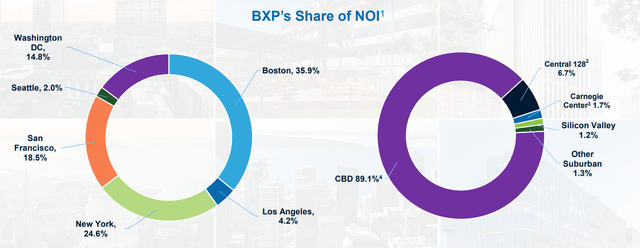

BXP is a publicly traded developer, owner, and manager of premier office buildings in the United States. The trust’s real estate portfolio consisted of 187 properties as of March 31, 2024, that were mainly concentrated in a small number of key office markets. The portfolio further consisted of 53.5 million square feet and produced $3.3 billion in annualized revenues for the trust.

BXP has a significant presence in Boston, New York, San Francisco, Washington DC, Los Angeles, and Seattle. The majority of the trust’s real estate exposure is in the central business districts of these cities, making BXP a concentrated prime office real estate investment trust.

BXP’s Share Of NOI (BXP Inc)

Office real estate investment trusts have made a boatload of negative news in the last two years as hybrid work arrangements and high interest rates have weighed on the valuations of office buildings, a consequence of higher vacancy rates and lower income projections. These trends in turn have repelled investors even though some trusts, like BXP, have strong lease metrics.

Furthermore, the central bank appears poised to slash interest rates in the short term as consumer prices trended down for the third consecutive quarter in June. With inflation pressure falling to just 3% in June, a key source of concern in the office market, the continuation of high interest rates, is set to fade as well, which might pave the way for a rerating of BXP’s shares.

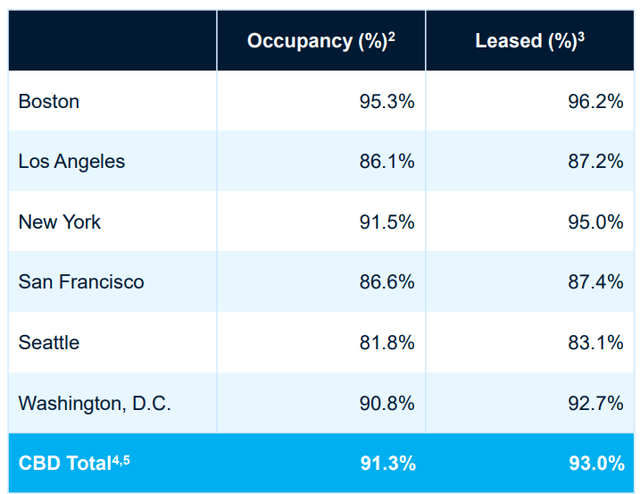

Despite all the fears in the market about the occupancies of prime office buildings, those buildings that are located in central business districts of America’s largest cities, BXP has had quite solid occupancy stats: BXP’s key properties had an occupancy of 91.3% in 1Q24.

Occupancy Rates (BXP Inc)

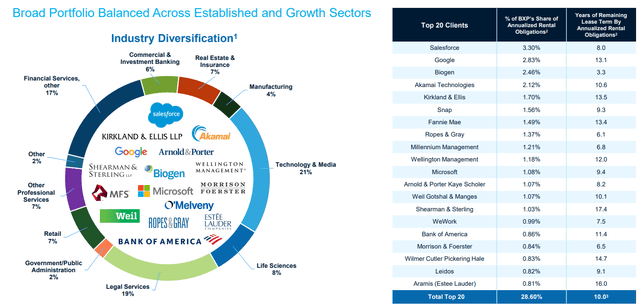

BXP is doing quite well with its office real estate investments because of the unique tenant composition of its portfolio: The majority of its tenants are tech companies (like Microsoft, Salesforce, or Google), financial services and asset management businesses, law firms, or banks.

Some tech companies are tapping into local talent pools in San Francisco and New York which, despite general pressure on the occupancy of office buildings, bodes well for the utilization of BXP’s office-centric real estate investment portfolio.

Top 20 Clients (BXP Inc)

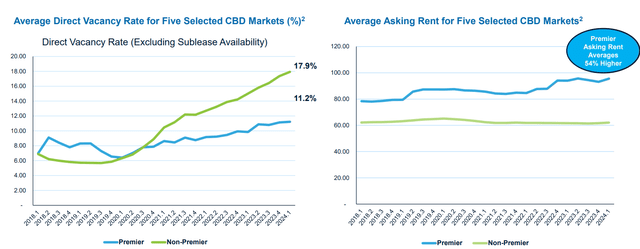

Furthermore, BXP’s focus on prime office buildings allows the trust to charge overall higher rents. The prime office market has not nearly been as badly affected by the office market downturn as the non-prime market.

According to BXP, the prime properties in the trust’s core markets can charge substantially higher rents than non-prime properties, in addition to having lower vacancy rates on average.

Average Asking Rent (BXP Inc)

Dividend Metrics Imply A High Margin Of Safety

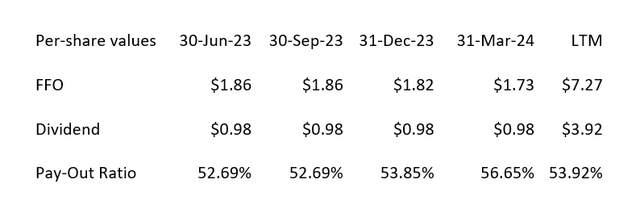

BXP has a low payout ratio in the 50-percent range, which lends the dividend a high degree of visibility and predictability. BXP earned $1.73 per share in 1Q24, which reflected a dividend payout ratio of 57%.

The office real estate investment trust paid out 54% of its funds for operations in the last year, which reflects a high margin of safety for BXP’s dividend.

The trust presently pays $0.98 per share for a 6% yield. Though BXP could afford to raise its dividend payout, it has paid a steady $0.98 per share per quarter dividend since the first quarter of 2020.

Dividend (Author Created Table Using Trust Information)

FFO Guidance And Multiple

BXP foresees $6.98-7.10 per share in funds from operations in 2024, which reflects a YoY growth rate of (3)%. Based on a stock price of $68.55, BXP is selling for a FFO multiple of 9.7x.

In the last year, BXP has sold for prices ranging between $50.64 and $73.97, implying FFO multiples of 7.2-10.5x. So the office real estate investment trust is presently selling at the higher end of this range. Competitors to which BXP could be compared are Alexandria Real Estate Equities, Inc. (ARE) and Vornado Realty Trust (VNO).

ARE sells for 13.5x 2024 guidance FFO, whereas VNO sells for 13.9x 1Q24 run-rate funds from operations, so BXP might be a more appealing choice for passive income investors. BXP is as cheap as it is as its portfolio is more concentrated in a small number of key real estate markets and, therefore, has higher risks.

If dividend growth is more of a pressing concern, I would choose Alexandria Realty Estate Equities as the trust is growing its dividend and raised its payout twice in the last year. Alexandria Realty Estate Equities also has a comparable dividend payout ratio of 55%, on a twelve months basis.

Why The Investment Thesis Remains Risky

As I have argued, BXP does presently not grow its dividend, and it hasn’t done so since 1Q20, which means investors are not getting the benefit of compounding higher dividend income over time.

In addition, the concentration of office properties in a small number of key cities/CBDs may make some passive income investors uneasy as there are obvious concentration risks reflected in BXP’s portfolio.

My Conclusion

BXP makes a surprisingly strong value proposition for passive income investors.

Despite pressure on the office sector due to hybrid work arrangements, the portfolio is overall well-leased. The tenant roster includes solid companies, particularly in non-cyclical industries such as software and tech, and BXP easily supports its dividend with funds from operations. As a matter of fact, the dividend payout ratio is quite low in the 50-percent range, and the valuation is moderate as well.

From a long-term strategic investment angle, I think an investment in BXP’s high quality prime office portfolio can make sense as long as passive income investors understand the risks. One shortcoming of BXP is that the real estate investment trust is not growing its dividend.

Taking into account the high occupancy rates, prime office focus, and solid tenant profile, I think the risk/reward relationship is favorable. Buy.

Read the full article here

")

")