")

")

Swiss Re (OTCPK:SSREF) is a leading global reinsurance company. Based in Switzerland, the company has a widespread international presence, with 51.4% of its premiums collected in the USA, 30.6% in EMEA, and the remaining 18% from other regions.

The company operates through three divisions: P&C (Property & Casualty) reinsurance (51.4% of premiums), L&H (Life & Health) reinsurance (34.4%), and corporate solutions (14.2%).

Company’s data

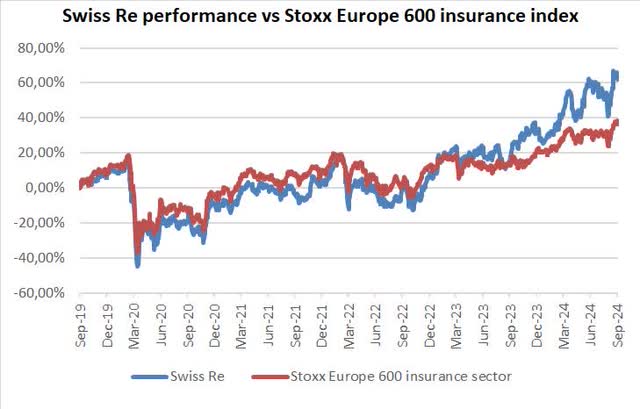

Swiss Re has shown strong performance year-to-date (+21%), reaching a peak of CHF 118.3, its highest since 2007. The stock has outperformed its European peers – measured against the STOXX Europe 600 insurance index – over both 1-year (+21% vs. +13%) and 5-year (+62% vs. +36%) horizons.

Radaecowatch.com

Latest Company Results

Swiss Re’s Q2 2024 results exceeded consensus expectations, reinforcing our positive outlook on the stock. Net income amounted to $2.088 billion (+16.8% year-over-year), driven by a substantial increase in net income from the L&H Re division (+46.2% y/y). In the P&C Re sector, net profit remained stable at $989 million (compared to $973 million), as insurance revenue declined 0.8%, impacted by a reduction in some casualty lines, partly offset by price increases. The P&C combined ratio came in better than expected, at 84.4% (consensus: 85.6%). During the earnings call, CEO Andreas Berger reaffirmed the company’s target of achieving a $3.6 billion net income in 2024, representing a 21.1% increase from 2023.

Investment Thesis

In an environment of rising market volatility, where investors are seeking to diversify away from tech stocks, we believe Swiss Re presents a compelling investment opportunity. The following factors support a strong case for investing in Swiss Re:

- Solid Medium-Term Growth Prospects: The global insurance market is projected to grow at an annual rate of 5.5%, in line with expected global GDP growth. We expect Swiss Re’s net premiums earned to grow at a 5.7% CAGR over the next decade, consistent with its average growth over the past 10 and 20 years. Additionally, we estimate Swiss Re’s EPS to grow at a 4% CAGR, with a net margin (net profit/premium earned) stabilizing at 6% in the medium term in line with the last 20-years average and below the 6.5% achieved in 2023.

-

High Dividend Yield

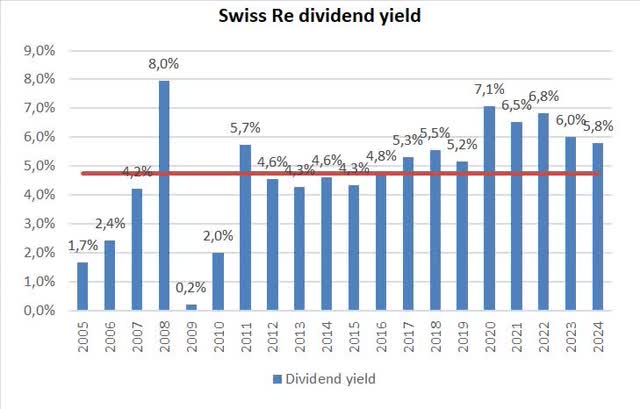

Swiss Re paid a CHF 6.21 dividend for 2023, yielding 5.4%. With net income expected to continue growing, we anticipate further increases in annual dividends in the coming years, making the stock appealing to income-focused investors.

-

Robust Balance Sheet

The company maintains a strong financial position, demonstrated by its solvency ratio of 306% at the end of 2023. This provides Swiss Re with the capacity to absorb unexpected losses while still delivering returns to shareholders.

Valuation

We value Swiss Re using a DCF model and a multiple valuation methodology. In the DCF model, we apply a 9% cost of equity and assume a 4.0% long-term dividend growth rate, consistent with projected net income growth. This results in a target price of CHF 133/share ($160.9/share), reflecting a 16.6% upside from the September 6th closing price. Swiss Re currently trades at a 5.8% expected 2024 dividend yield, above its 10-year average of 5.6% and significantly higher than the 20-year average of 4.5%. A reversion to the long-term average would imply a price increase to CHF 145/share ($175.4), reflecting a potential 26.6% upside.

Company’s data

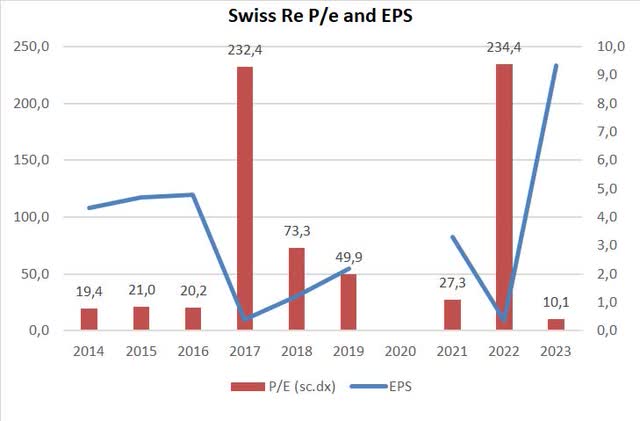

In terms of the P/E ratio, Swiss Re is trading at a 10-year low, reflecting volatility in past years.

Company’s data

The View from the street

Although Swiss Re’s H1 2024 results exceeded expectations, equity analysts covering the stock remain cautious, with 6 Buy, 7 Hold, and 3 Sell recommendations. However, throughout 2024, analysts have consistently raised their price targets for Swiss Re, suggesting that they have underestimated the Company’s strength. The consensus target price now stands at CHF 115.73, up from CHF 100.95 at 2023-end. We believe further positive results in upcoming quarters could drive upward revisions in analysts’ forecasts, boosting the stock price.

Risks

We identify two primary risks to Swiss Re in the medium term:

-

Exposure to Natural Catastrophes

Swiss Re is exposed to significant losses from events like hurricanes, earthquakes, and other natural disasters. These unpredictable events can substantially affect profitability, even with reinsurance protections in place.

-

An interest rates decline

A sharp decline in interest rates could reduce investment income, substantially grown over the last few years. Investment income rose from USD 2.9 billion in 2022 to USD 4 billion in 2023. For H1 2024, investment income increased from USD 1.612 billion to USD 2.073 billion year-over-year. Declining interest rates would reduce this crucial revenue stream.

Conclusion

Swiss Re is a market leader in the reinsurance sector, with strong prospects for medium-term growth. Its business model is resilient even in the face of potential economic slowdowns, while its solid balance sheet and high dividend yield make it an attractive option for risk-averse investors. In light of heightened market volatility, Swiss Re represents an excellent diversification opportunity. In our view, high and rising dividends are an important element supporting the Buy case in the stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")