")

Brookfield Corp. (NYSE:BN) recently reported results, and we thought it was a good time to check our thesis, and in particular the insurance segment Brookfield Reinsurance (NYSE:BNRE). As a reminder, BN and BNRE are entangled because BNRE shares are exchangeable for BN shares as described here, and they have identical distributions. For this reason, when we write about BNRE we analyze the entire Brookfield Corporation, but with extra focus on the insurance segment, or as it is now called, wealth solutions. Since we wrote that BN/BNRE was so undervalued that the real estate was basically offered for free, shares have delivered a more than 55% total return, outpacing the S&P 500 index (SP500)(SPY) by a meaningful margin. At the end of the article, we have updated our valuation model to see if shares remain undervalued.

Financial Results

One of the major milestones the company achieved during the quarter was closing on the acquisition of American Equity Life (AEL). Brookfield Corp. contributed Brookfield Asset Management shares (BAM) from its own balance sheet. We view this development as particularly attractive to BAM shareholders, as assets under management (AuM) will grow thanks to its parent company’s investment. Another important development during the quarter was the agreement to acquire a majority stake in the global renewable energy platform Neoen in collaboration with its renewable energy subsidiary Brookfield Renewable (BEP)(BEPC). The company’s ownership in Brookfield Asset Management declined by 2% to 73% as it used roughly $1 billion in BAM shares as part of the payment for the AEL acquisition. The asset management subsidiary continues growing at a rapid pace, reaching $1 trillion in AUM and $514 in fee-bearing capital. Management expects strong fundraising in the second half of the year with the anticipated closure of its latest flagship funds, which should further increase BAM’s earnings.

One area where we were surprised by the strong divergence is with the real estate investments. The company has separated them into two buckets, the highest quality that it plans to hold indefinitely and calls core real estate, is performing surprisingly well. The other bucket, which the company calls transitional real estate, is showing weakness, particularly the office investments. The company reported a low occupancy of only 83.6% for its transitional office segment, and a seven-year average lease. We believe that occupancy could fall further in this segment as leases expire. Fortunately, with an estimated equity value of roughly $4.6 billion, this real estate segment makes only about 13% of the total equity value of the company’s real estate business. Transitional retail appears to be doing better, with an occupancy level of approximately 93.1%. Brookfield puts more emphasis on its core real estate portfolio, where it saw a 3% growth in same-store net operating income (NOI), and more impressively, new signed leases were about 23% higher compared to expiring ones.

The company reported ending the quarter with deployable capital of close to $150 billion, which means the company is very well positioned in case that market dislocations surface attractive investment opportunities.

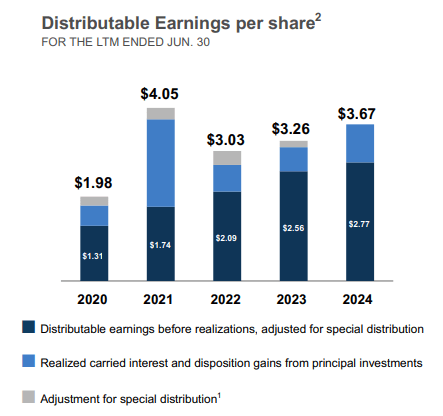

Finally, distributable earnings (DE) before realizations increased by 11% year-over-year. Distributable earnings for the last twelve months were $3.67 per share. While this is still below the record high delivered in 2021, it is important to note that in 2021 the company took advantage of high valuations to sell investments, which resulted in abnormally high realized carried interest and disposition gains.

Brookfield Investor Presentation

Wealth Solutions

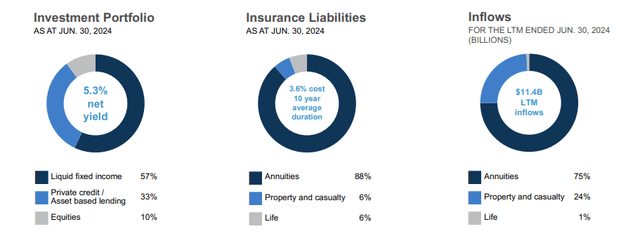

The company reported that with the closing of the AEL acquisition, insurance assets have grown to over $110 billion, and that its originations rate is now approximately $3.5 billion per month through its annuity channel. Most of the value the company is generating is through its asset allocation expertise. The company is currently earning about 2% more than its average cost of capital, which it expects will go down to 1.7% due to the AEL acquisition, but should trend closer to 2% once it makes adjustments to AEL investment portfolio. Taking everything together, the company believes it can grow annualized earnings from $1.4 billion to $2 billion. Given the strong results, Brookfield is looking into further growing this business segment. The company values this business at almost $22 billion, which, we think, is reasonable given how fast it is growing.

Brookfield Investor Presentation

Future Growth

Besides the wealth solutions segment, other areas where the company is creating significant value include its renewable energy and infrastructure investments (BIP)(BIPC). As a result, the company has acquired in recent years more than ten renewable operating and development platforms and three data center businesses. Management is convinced that there will be trillions of dollars of investment opportunities in the coming decades for renewable energy, data centers, and infrastructure development.

Brookfield does have an impressive track record of compounding its balance sheet capital at more than 20% for the past three decades. The carry it generates from capital invested for external investors also helps, which boosts returns and can be reinvested back into the business, or returned to shareholders. Accumulated unrealized carried interest reached $10.7 billion, or a 13% increase over the last twelve months.

Succession

We believe one of the characteristics shared by truly great companies is that they are extremely careful with maintaining a good business culture, and are extremely careful when planning leadership succession. Most companies announce CEO changes from one day to the next, as it recently happened with Starbucks (SBUX). On the other hand, it is extremely rare to see companies like Berkshire Hathaway (BRK.A)(BRK.B) where the successor is named years in advance and given increased responsibilities in a gradual manner.

As part of its succession planning, Brookfield has identified 36-year-old Connor Teskey as the next CEO of Brookfield Asset Management, but the change will be done when the company believes he is ready to take charge. One reason for choosing a young leader is because the company prefers to have someone lead over several decades, and with new, fresh ideas. Still, for the time being, Bruce Flatt will remain CEO of Brookfield Corporation.

Valuation

While shares are trading at a higher price compared to the last time we analyzed the company, the estimated net asset value (NAV) has also increased significantly. We are doing a sum-of-the-parts (SOTP) valuation using the most recent data, with some adjustments compared to what the company shares in its supplemental. The main changes we have made is that we do not include target carried interest, but only the net accumulated unrealized carried interest. We also use the IFRS valuation for the transitional real estate investments, and we use the most recent share prices for the public subsidiaries. We estimate NAV at $68 per share, lower than the $83 calculated by the company. Interestingly, the current share price still appears to assign no value to the real estate investments.

The company appears to agree that shares are undervalued, and is therefore buying back shares in a meaningful way. So far, in 2024, it has repurchased close to 20 million shares for about $800 million, an average price of $40 per share.

| Business | # of shares (millions) | Share Price | Value |

| BAM | 1194 | $41 | $48,954 |

| BEP | 302 | $24.71 | $7,462 |

| BIP | 207 | $30.96 | $6,409 |

| BBU | 142 | $20.15 | $2,861 |

| $65,686 | |||

| BPG (Brookfield Property Group) | $23,729 | ||

| Wealth Solutions | $21,450 | ||

| Other Investments and accumulated carry | $18,191 | ||

| Total Investments | $129,056 | ||

| Working capital, net of corporate cash and other | -$177 | ||

| Debt and preferred capital | -$19,156 | ||

| NAV | $109,723 | ||

| Diluted shares | 1,597 | ||

| NAV per share | $68 | ||

| NAV per share ex. BPG | $53 |

Risks

One important risk with Brookfield is that it tends to be highly leveraged, even if most of the leverage is non-recourse at the subsidiary or project level. The risk is mitigated given the wide diversification, and high-quality of most of its assets. This is reflected in the ease with which the company has been able to refinance large amounts of debt. We were particularly impressed with the approximately $160 million of 60-year subordinated notes it managed to issue for Brookfield Infrastructure Partners. Needless to say, not many companies can secure financing with such a long duration.

Conclusion

Despite an increase of more than 50% in little over a year, we continue to see Brookfield as undervalued given that shares continue to trade significantly below their net asset value, which has increased significantly in the past year. Surprisingly, it appears that the market continues to value the real estate investments at next to nothing. While the lower quality office investments show signs of deteriorating fundamentals, the higher-quality portion continues to see NOI growth and positive leasing spreads. The asset management business is also experiencing positive fundamentals with rapid AUM growth. Finally, the wealth solutions business is growing rapidly and is now a meaningful source of value creation. The company appears to see shares as undervalued given the significant amounts of capital used to repurchase shares.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")