")

")

")

Introduction

Per my December Brookfield Asset Management Ltd. (NYSE:BAM) article, there is logic in holding BAM. Since that time, we have new information from the 1Q24 filings, the 2Q24 filings, and the September Investor Day presentation.

My thesis is that Brookfield Asset Management Ltd. has nice growth opportunities in front of them.

The Numbers

Per the September Investor Day presentation, management hopes to grow the business substantially over the next five years such that it becomes twice its size:

BAM growth summary (September 2024 Investor Day Presentation)

Using the rule of 72 where the annual rate of return times the number of years to double equals 72, this means we divide 72 by 5 to conclude the business should compound at a rate between 14 and 15% if management delivers.

In the 2Q24 call, Brian Bedell from Deutsche Bank (DB) asked a helpful question about organic growth rather than acquisitions. He also wanted a breakdown of what portion of the growth will be fee-bearing. BAM President Connor Teskey said most of the growth will be organic and much of it will be fee-bearing because the biggest components, insurance and credit, tend to be fee-bearing in nature:

We expect the vast majority of our growth to come organically. And from that standpoint, we’re incredibly encouraged by the fundamentals that we’re seeing within our business to deliver on that. One really interesting dynamic within the last quarter has been the strength in our fundraising was really across our complimentary strategies. And those tend to be new or earlier vintage funds that there is a lot of effort to get them off the ground. But then they tend to scale much more meaningfully in the future.

Tailwinds

Per BAM’s September Investor Day presentation, there were about $25 trillion in alternative assets under management, or AUM, in 2022 and this is expected to increase to $60 trillion or more by 2032. Broad tailwinds benefit BAM’s institutional business:

Tailwinds (September 2024 Investor Day Presentation)

Track Record Of Returns

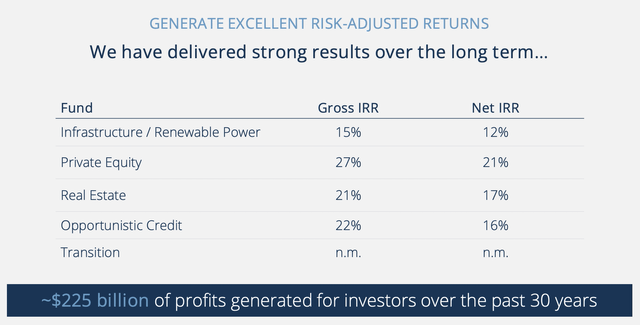

One of the reasons BAM has a good track record of returns is because they choose the right sectors at the right time. On the energy side, BAM allocated capital shrewdly over the years by sticking with hydro until the economics of solar and wind improved. The September Investor Day presentation shows their track record of adapting. Years ago they centered on railroads/ports, hydro, and pipelines. These days they’re focusing on telecom towers/data centers, solar/batteries/nuclear power solutions and logistics/housing/hospitality. Per the September Investor Day presentation, their returns across the board have been impressive:

BAM returns (September 2024 Investor Day Presentation)

Partnership Approach And New Products

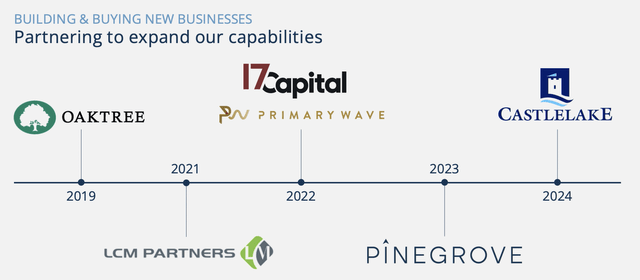

Regarding the above growth items, I like to talk about the #3 partnership and #4 new products together because of the overlap. Management plans to do a combination of building and buying to see growth from new areas such as financial infrastructure, healthcare, and AI. Partnering is a big part of BAM’s plan:

BAM partnerships (September 2024 Investor Day Presentation)

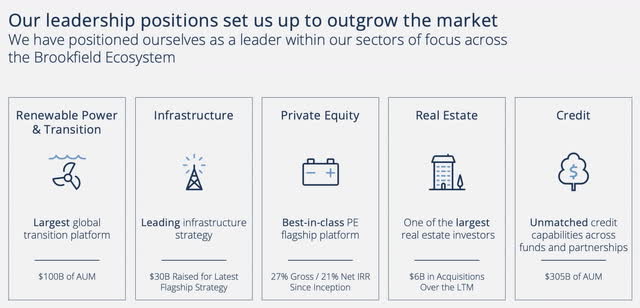

Ecosystem

Per the 2Q24 letter, few companies have an ecosystem like Berkshire with the breadth of operating experience on the industrial side. For example, they used to discuss the fact that not many companies knew how to operate a dam when they were more heavily investing in hydropower. Their ecosystem has allowed them to launch six private equity funds over the years, giving rise to over $130 billion of investments with a gross IRR of about 27% and a net IRR of about 21%:

This success in private equity has been driven by our disciplined investment approach, focusing on acquiring businesses that provide essential products and services and that generate resilient cash flows. We have particular expertise in industrial businesses, where few have operating capabilities to do what we do, offering us a competitive advantage.

One of the reasons BAM President Teskey is on track to become BAM CEO is because he was influential in bringing about the Oaktree acquisition, which helped speed up the addition of Credit to BAM’s ecosystem:

BAM ecosystem (September 2024 Investor Day Presentation)

Valuation

Excluding amounts not attributable to BAM, trailing twelve-month (“TTM”) fee-related earnings (“FRE”) are $2,281 million per the 2Q24 supplemental. Historically, management has valued this at 25 to 35x, which implies a valuation range of $57 to $80 billion when rounded to the nearest billion.

Per the 2Q24 supplemental, the Total carry eligible capital/target carried interest, net to BAM, net of costs is $783 million. I think the valuation is 10x this amount, or $7.8 billion.

Summing up and rounding to the nearest billion, I think the total valuation range is about $65 to $88 billion.

I think sites like Yahoo don’t include the shares held by BN for their market cap number, so there are inconsistencies depending on the type of lens used to view the market cap. The 2Q24 supplemental shows 1,630.6 million diluted shares, so we get a market cap of a little more than $72 billion when multiplied by the September 11 share price of $44.27. The market cap is within my valuation range and I think the stock is a hold.

Disclaimer: Any material in this article should not be relied on as a formal investment recommendation. Never buy a stock without doing your own thorough research.

Read the full article here

")

")

")