")

(NYSE:BRCC)")

Most companies in the stock market are echoing signs of an incoming U.S. recession, especially in the consumer space. Weakening demand from both its direct-to-consumer business as well as its wholesale partners has punished BRC Inc. (Black Rifle Coffee (BRCC)), a specialty coffee distributor known for its patriotic brand and army veteran affiliation.

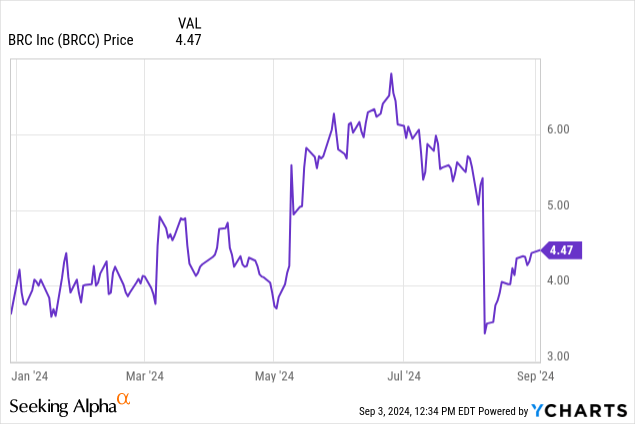

Year to date, BRC has now nearly wiped out all of its gains. At one point in early May, the stock had shot up to nearly $7; now, the stock sits more than 35% below that peak. The question for investors now is: is there a path for recovery ahead for BRC?

I last wrote a bullish note on BRC in mid-June, when the stock was still trading above $6 per share. At the time, while acknowledging several execution risks for this small-cap company, I had argued that the company’s impressive wholesale channel growth plus its gross margin efficiencies warranted a buy. Since then, however, BRC has reported very weak Q2 results that showed a decline in its consumer segment and a sharp slowdown in wholesale. As a result, I’m cutting my rating on BRC down to a neutral stance.

Now, I see a more balanced bull and bear case for BRC. The core risks that have emerged are:

- DTC declines may impede wholesale adoption. BRC’s major growth strategy is to pull back on investing into its DTC franchise (which includes online sales of coffee beans plus a small cafe network) and focus on selling to resellers, particularly grocery chains. By 2025, the company is still maintaining its expectation that its products will be carried in every major grocery chain. And yet if its DTC brand is declining (coffee club subscribers are down y/y), wholesalers may also think twice about ordering BRC inventory.

- Political risk. There’s no doubt that the U.S. is heading into a divisive November election season. Black Rifle Coffee, as inherent in its name, isn’t shy about its political stances, particularly on firearms. While this may accrue a loyal, hardcore fan base among its customers, it may also alienate others amid a heated political climate.

Still, there are opportunities as well, which include:

- Form factor expansion through partnerships. The company recently struck a distribution agreement with Keurig Dr Pepper (KDP) to produce BRC-branded coffee pods, which increases its potential for market adoption by customers who are a fan of instant coffee brews.

- Wholesale focus may be the best path to profitability. BRC is already profitable on an adjusted EBITDA basis. Not worrying about maintaining a large coffee chain network that has expensive labor costs in a wage-inflationary environment may be the best path for BRC to scale its bottom line.

We note as well that BRC is additionally planning to expand into the energy drink category in 2025. At the moment, I view this as neither a clear positive nor negative. The company notes that energy drinks are a massive $20 billion category, so this clearly extends BRC’s addressable market. But at the same time, this is BRC’s first major foray outside of coffee, which may drain considerable resources and dilute the company’s brand image.

BRC Energy (BRC Q2 shareholder deck)

All in all, I’m far less impressed with BRC’s growth prospects, especially considering its wholesale slowdown – hence my ratings cut. Yet with the sharp slide in the stock since May, signs of stabilization in the wholesale business or near-term contributions from when energy drinks launch early next year may be all that it takes to spark a rebound rally here.

Q2 recap

Black Rifle’s Q2 results sparked a major selloff in this stock. Take a look at the Q2 results below:

BRC Q2 results (BRC Q2 shareholder deck)

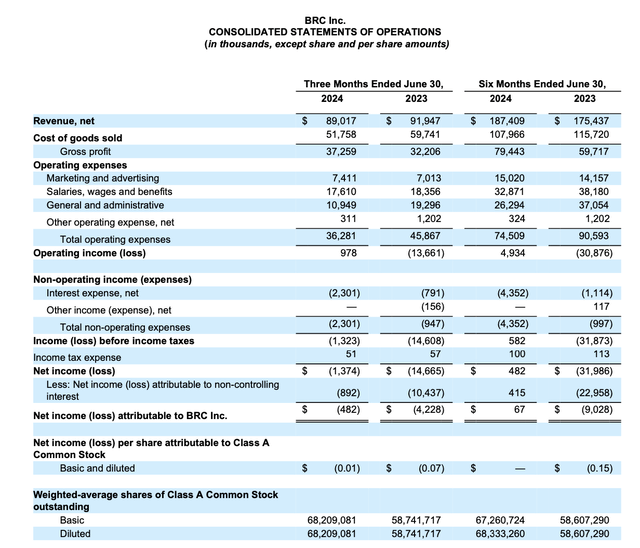

Revenue declined -3% y/y to $89.0 million, sharply missing Wall Street’s expectations of $100.9 million (+13% y/y) by a huge sixteen-point margin. This decelerated 21 points relative to much stronger 18% y/y growth in Q1.

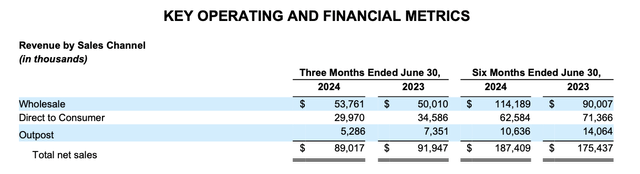

The big driver behind BRC’s growth slowdown is a sharp downturn in wholesale revenue growth trends, which grew at only an 8% y/y pace in Q2: versus a 51% jump in Q1:

BRC channel results (BRC Q2 shareholder deck)

The company attributed this disappointment to a slower-than-expected uptake of its products among its wholesale grocery distribution partners. Still, the company does note that it has committed launch dates from many of its partners, and that management continues to expect the wholesale channel to be a significant driver of growth in the next 12-18 month window.

According to CEO Chris Mondzelewski’s remarks on the Q2 earnings call (key points bolded):

Sales growth was lower than we expected for two reasons. First, we cut investment in our direct-to-consumer or DTC business. Post the pandemic, consumer behaviors have shifted, as we look across the entire industry fewer consumers are choosing to buy products directly from DTC sites. As this occurs, we find that our dollars spent in driving DTC awareness are less effective and so we have chosen to allocate these dollars where we get a higher ROI.

I’m proud of our team’s discipline in creating clear principles around when to pull back on this spending and as our growth shifts to other channels and other products, we will see the benefit of this. The good news is that consumers are continuing to seek out our products. Their shopping behavior is shifting back to either traditional or online retail. This takes me to my second point.

While we continue to expect consumers to be able to find our products in almost every major grocery retailer in the U.S. by the end of 2025, the rollout will be a bit slower. While commitments and discussions are going as planned, some retailer shelf resets that we expected to happen in 2024 are shifting to 2025. Given our strong performance on shelf, we continue to have very effective conversations with every major retailer in the country […]

At this point, we have committed launch windows for the largest five grocery chains between now and Q2 2025.“

Committed launch windows, however, certainly don’t guarantee volume. It’s clear that BRC’s consumer demand is weakening, with DTC channel revenue down -13% y/y in the quarter and Outpost revenue (which is revenue earned from the company’s 36 cafes, including 18 that are franchised by other operators) down -28% y/y. The company also counted only 202.1k coffee subscriptions at the end of the quarter, down -16% y/y and shedding roughly 7k subscribers relative to the end of Q1. Ultimately, these results may induce BRC’s partners to order less inventory for their stores.

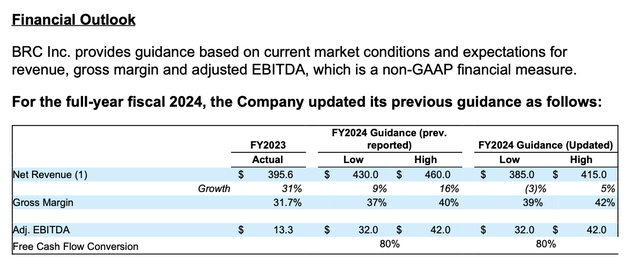

As a result of these disappointments, we note that BRC drastically took down its growth expectations for the year, now at a flattish range of -3% to +5% in revenue growth for the year, from a previous expectation of 9-16% y/y growth:

BRC outlook update (BRC Q2 shareholder deck)

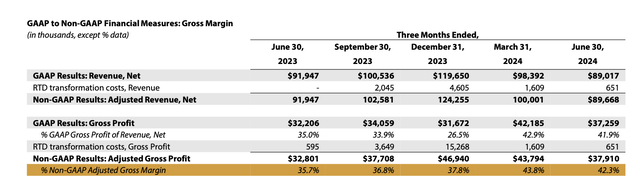

The good news: BRC’s pace of gross margin expansion is still impressive. Q2 gross margins of 42.3% rose 660bps y/y, though they did recede 150bps sequentially from Q1:

BRC gross margin (BRC Q2 shareholder deck)

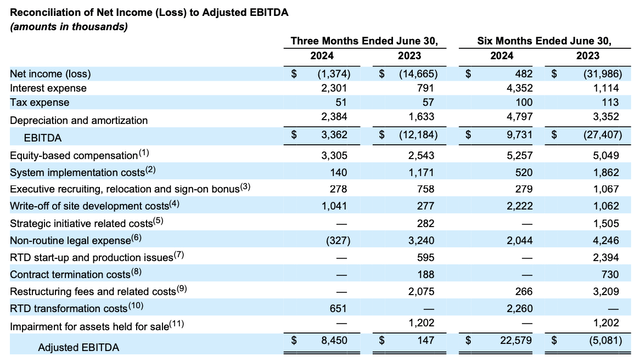

Adjusted EBITDA of $8.5 million also represented a 9.5%, versus roughly breakeven in the year-ago quarter:

BRC adjusted EBITDA (BRC Q2 shareholder deck)

Valuation and key takeaways

At current share prices near $4.50, Black Rifle Coffee trades at a market cap of $944.7 million. After we net off the minimal $9.6 million of cash and $66.5 million of debt on Black Rifle’s latest balance sheet, the company’s resulting enterprise value is $1.00 billion.

Against the midpoint of the company’s $32-$42 million adjusted EBITDA range for the year (which it maintained despite the revenue guidance cut), the stock trades at 27.8x EV/FY24 adjusted EBITDA – which doesn’t represent obvious value. It’s clear that a bet on BRC represents a bet on an uncertain 2025: which will be determined by the success of the company’s ongoing wholesale rollouts that ran into thorns in Q2, as well as the upcoming January launch of the energy drink category.

All in all, I don’t feel confident enough in the company’s latest trends to continue banking on a rally here (especially with a potential recession looming around the corner), even though some catalysts for possible upside next year exist.

Read the full article here

")

")

")

")