")

")

This article was coproduced with Leo Nelissen.

If there’s one thing we have discussed in the past two months, it’s the market’s sudden belief that the economy is out of the woods.

The main reason why stocks started to fly in 4Q23 is the expectation that the Fed will turn very dovish this year, with expectations of no less than five rate cuts (it was six a week ago)!

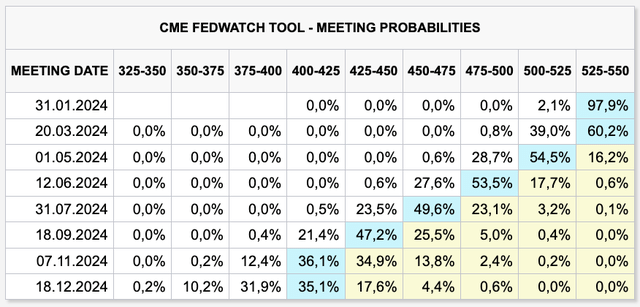

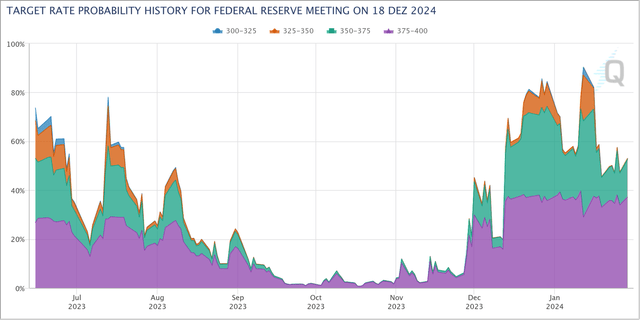

Using Fed Funds Futures, we see that the market expects the current rate range of 5.25% to 5.50% to be the terminal rate, followed by a number of consistent cuts to the 4.00% to 4.25% range on Dec. 18, 2024.

CME Group

What’s interesting is that the odds of a sub-4.00% Fed Funds Rate have risen from roughly 0% in October to 50% in January.

CME Group

Sure, inflation has come down a lot, and while we agree that some easing is certainly appropriate, the market may have gotten way too dovish.

Why?

- Core inflation is still close to 4%.

- Headline inflation seems to be bottoming.

- Oil is close to $80, with the high likelihood that supply/demand dynamics push it above $90-$100 the moment investors start to price in higher economic growth.

- Another reason is that tech stocks are red hot. Although the stock market is not a part of the Fed’s mandate, it’s highly unlikely that the Fed cuts six times into one of the strongest tech bull markets in decades.

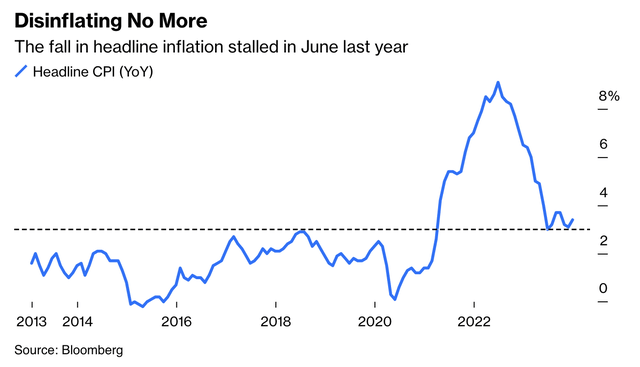

With regard to inflation, we see that headline inflation started to bottom. In this case, inflation is still above 3%, which is horrible news for the Fed.

Imagine an aggressive easing cycle when inflation is still above average!

A second wave of inflation would be likely, making the Fed’s job even harder.

Bloomberg

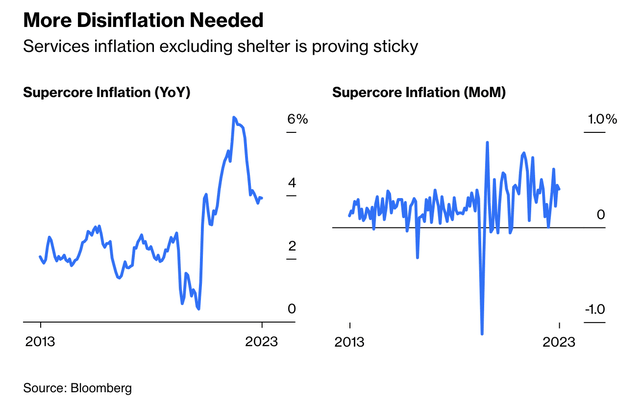

To use the words of Bloomberg’s John Authers (emphasis added):

“Headline CPI isn’t, and shouldn’t be, a measure that drives what the Federal Reserve does next. For that, we need to look at what’s now known as ‘super core inflation,’ covering the services sector, excluding shelter. These businesses are particularly sensitive to wages. This measure also suggests that disinflation has stalled. It’s not just about base effects, but also high on a month-on-month basis:”

Bloomberg

Please bear in mind that we’re not making the case that the market will crash. However, there are some implications:

- If inflation turns out to be sticky, the Fed will likely be forced to maintain rates higher than expected for a longer than expected period. This could force the market to adjust its expectations.

- Companies with elevated debt levels may be further away from a situation where they can use subdued rates to refinance, which could have significant economic implications.

That’s where real estate comes in – specifically office real estate.

A Storm Is Brewing In The Office Sector

What’s worse than a wall of maturing debt?

A wall of maturing debt hitting a sector already struggling with major issues.

We all remember what happened during the pandemic when lockdown mandates did a number on economic activity. Gasoline demand imploded, airports were empty, restaurants were closed, and people worked from home.

While gasoline demand is back, restaurants are open again, and Americans are flying more than ever, offices have not recovered, as secular headwinds like working from home have turned into lasting issues.

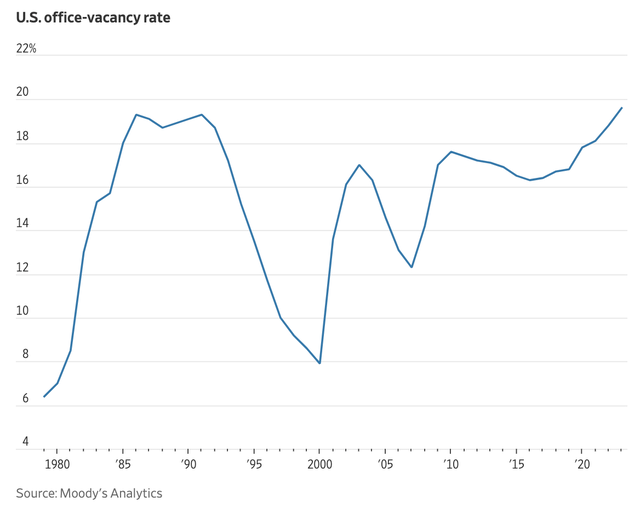

According to the Wall Street Journal, at a historic 19.6%, office vacancies in major U.S. cities have hit their highest point since at least 1989.

Wall Street Journal

This surge is emblematic of a larger trend, reflecting both the accelerated embrace of remote work due to the pandemic and the enduring consequences of the 1980s and ’90s office-market downturn.

Essentially, the current malaise finds its roots in the overbuilding of the ’80s and ’90s, when a construction boom, fueled by easy lending, led to speculative office projects, resulting in a glut of unoccupied buildings.

The aftermath of the savings-and-loan crisis in 1990 exacerbated the situation, leaving numerous offices vacant.

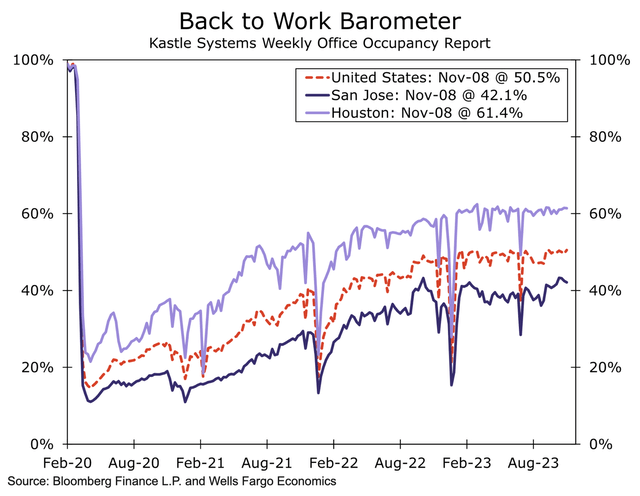

With regard to the current remote work situation, Wells Fargo noted in its 3Q23 report that the return to office is progressing slowly, with weekly occupancy around 50% of the pre-pandemic norm.

Wells Fargo

Meanwhile, a modest decline in job postings offering hybrid work suggests a potential reassessment of remote models. Slower hiring, particularly in office-using industries, indicates a focus on cost-cutting, potentially reducing future demand. Over the long run, technological advancements, including AI, pose a risk to office demand.

Even worse, supply won’t turn into a tailwind anytime soon as the same report shows that a substantial increase in supply, driven by sublease space and completed projects, is exacerbating the imbalance in the office market.

Net completions in 3Q23 were 7.5 million square feet, and 115 million square feet are currently under construction.

Hence, despite a recent decline in new groundbreakings, the supply overhang is likely to persist, affecting the market’s balance for the foreseeable future.

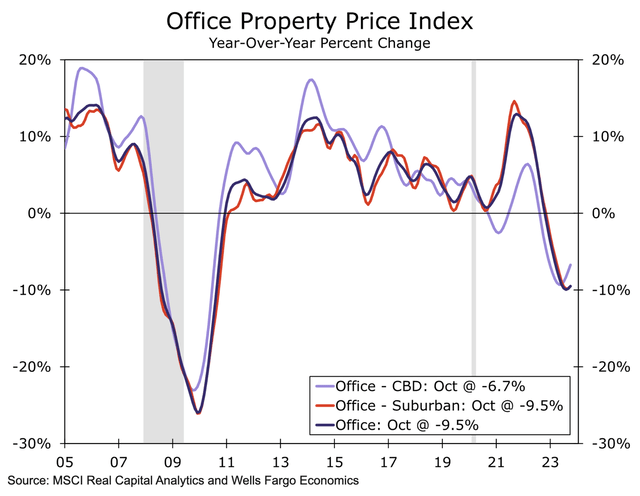

As a result of these headwinds, office property prices have dropped nearly 10% from their peak in June 2022, and transaction volumes are at their lowest since 2010.

Wells Fargo

Falling prices create challenges for property firms’ borrowing capabilities as decreasing asset values increase relative indebtedness.

To meet debt terms, companies may need to inject more cash, take on higher-interest borrowing, or sell assets in a declining market, complicating the refinancing of the $2.2 trillion of US and European commercial property loans due by 2025.

As one can imagine, this poses severe risks for a chain reaction that could go well beyond the office market.

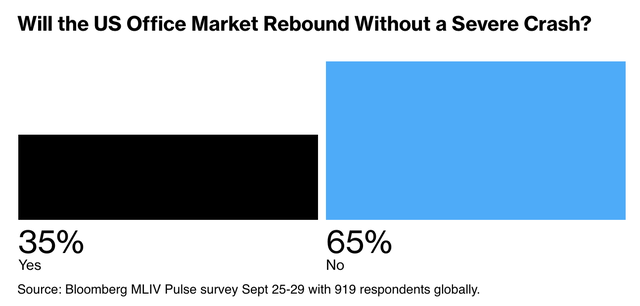

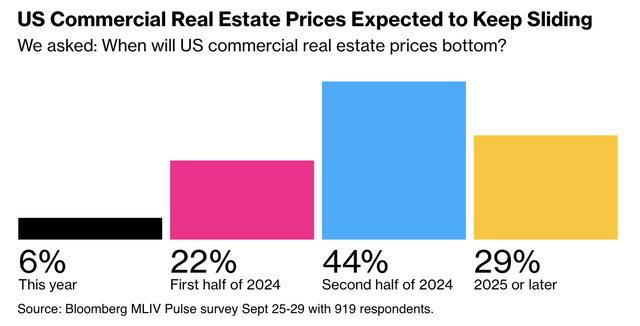

According to Bloomberg’s Markets Live Pulse survey, around two thirds of the 919 respondents anticipate a severe crash in the U.S. office market, with a majority predicting a rebound only after such a collapse.

Bloomberg

The grim outlook extends to the commercial real estate sector, expecting at least nine more months of declines, with prices not hitting bottom until the second half of 2024 or later.

Bloomberg

Needless to say, this forecast poses challenges for the $1.5 trillion of commercial real estate debt due by the end of 2025 – that’s in the U.S. alone.

Refinancing is expected to be difficult, particularly for the 25% of office buildings in the commercial property sector.

As a result, regional banks, holding approximately 30% of office building debt, are under stress, compounded by a decrease in deposits and funding capacity.

Smaller banks have experienced a deposit shrinkage of nearly 2% over the past 12 months, reducing their ability to lend at a time when lending demand will have to increase to service old debt.

In December, Bloomberg reported that a recent report commissioned for the National Bureau of Economic Research warns that declining commercial property values pose solvency risks for a wide range of U.S. banks.

Approximately 14% of all commercial real estate loans and a substantial 44% of loans on office buildings are in “negative equity,” surpassing property values.

This situation heightens the likelihood of borrowers defaulting as their stakes are rendered worthless.

The distress in commercial real estate markets could lead to anywhere from dozens to over 300 smaller regional banks facing solvency risks.

Furthermore, the report estimates that a 10% default rate on commercial real estate could result in around $80 billion in additional bank losses, increasing to an estimated $160 billion with a 20% default rate.

At some point, banks will have to be even more careful to lend money, tightening credit conditions at a time when more money is needed to keep the (office) CRE market from imploding.

Now What?

There are many ways to play this.

- Buying top-tier office REITs only to reduce bankruptcy risks.

- Not buying any office exposure to avoid elevated risks.

- Shorting offices.

- Buying distressed debt

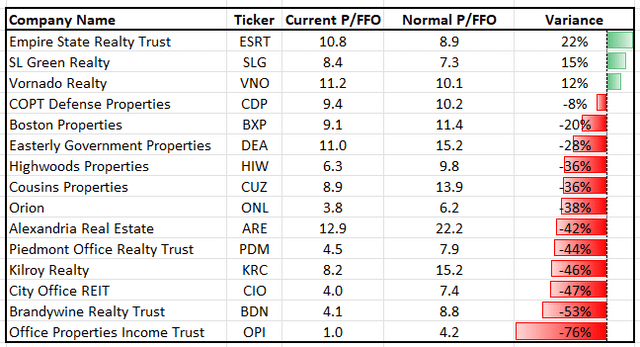

Point one is often discussed as we advocate for REITs like Alexandria Real Estate (ARE), which is technically an office REIT. However, it owns healthcare/biotech real estate, which is a market largely immune to ongoing issues.

Point two is our preferred way.

This is the safest way to play this as it means investors stay away from high-risk assets. In general, we have become more careful with cash deployment, given the unfavorable risk/reward created by the market.

Point three is for investors with a higher risk tolerance.

While a lot of weakness has been incorporated in stock prices in recent quarters, a situation of mass defaults could send (office) REIT prices much lower.

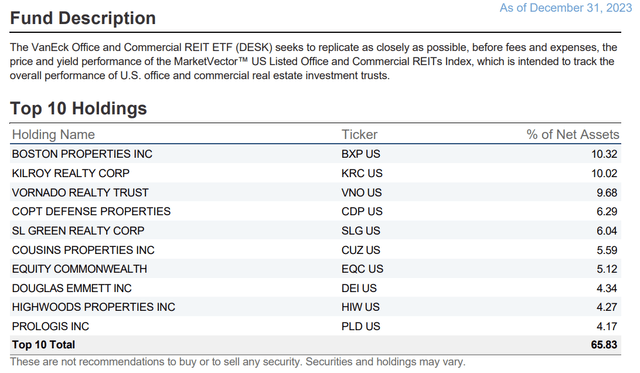

That’s where the VanEck Office and Commercial REIT ETF (DESK) comes in.

Incepted in September of 2023, this ETF seeks to copy the performance of the MarketVector™ U.S. Listed Office And Commercial REIT Index.

The ETF, which has a 4.7% SEC yield, has 27 holdings, with major exposure in Boston Properties (BXP), Vornado Realty Trust (VNO), Kilroy Realty (KRC), and SL Green Realty (SLG).

VanEck

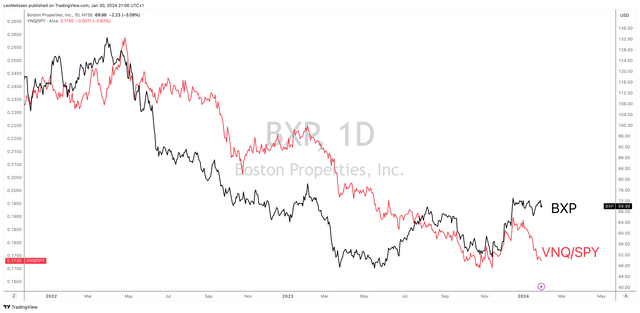

With that said, Boston Properties is up roughly 50% from its 2023 lows, as we can see in the chart below.

However:

- Office REITs have run into resistance again while the market has made new highs.

- In general, real estate has shown significant relative weakness, as the red line in the chart below shows. The red line displays the ratio between the Real Estate ETF (VNQ) and the S&P 500.

TradingView

Point four is buying distressed debt.

These developments are not bullish!

In general, we believe that investors need to be careful, as the market is not out of the woods due to sticky inflation and dovish Fed expectations.

Meanwhile, massive risks are building in the CRE industry, which could potentially trigger a chain reaction of defaults.

This is bearish for DESK and its components and could lead to much lower prices down the road.

Takeaway

Billionaire investor Barry Sternlicht and CEO of Starwood Property Trust (STWD) said that the office real estate asset class was previously worth $3 trillion and is now worth $1.8 trillion.

“There is a $1.2 Trillion of losses spread somewhere, and nobody knows exactly where it all is.”

He said that the office market is experiencing “an existential crisis” due to workers not returning to the office and that property owners are struggling to refinance loans as building values have declined. He said,

“So, the alternatives are the debt funds, which are having a field day.”

In the current economic landscape, our attention is drawn to the substantial risks surrounding office real estate.

The market’s optimism, fueled by expectations of dovish Fed policies, might be overlooking the red flags. With inflation remaining a concern and tech stocks soaring, the potential for an aggressive easing cycle poses a threat.

Zooming in on office real estate, the sector is facing a storm. The lingering effects of the pandemic, coupled with a historical oversupply, have led to a staggering 19.6% office vacancy rate—the highest since 1979.

Remote work trends, slower hiring, and technological advancements further challenge the sector’s recovery.

As prices plummet and transaction volumes hit a decade low, the $2.2 trillion of U.S. and European commercial property loans due by 2025 are at risk.

A looming crash in the office market could have cascading effects, stressing regional banks and potentially leading to a credit squeeze.

For investors, caution is paramount. Options range from strategic plays on top-tier office REITs to complete avoidance or even shorting.

In light of inflation uncertainties, the office real estate market demands a cautious approach that acknowledges the risks involved.

In general, real estate needs to be approached with caution, with a focus on safety and quality.

iREIT®

iREIT®

Note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Read the full article here

")

")

")