")

Security is always excessive until it’s not enough.” – Robbie Sinclair

Today, we put Beazer Homes (NYSE:BZH) in the spotlight. One of the many perplexing things in the market in 2023 was how well home builder stocks performed in light that existing home sales for the year posted their lowest levels since 1995. New home sales did rise four percent on the year it should be noted. Home builders also benefited from lower input costs such as lumber as inflation pressures ebbed. In addition, low inventory levels keep average home prices high even with over seven percent average 30-Year mortgage rates for most of the year.

Seeking Alpha

Beazer rode these tailwinds to a solid gain for shareholders in 2023. The shares still have a low valuation based on earnings. Can the equity continue to rally or could the shares become a ‘value trap‘ if sledding gets tougher for the housing market in 2024. An analysis follows below.

Company Overview

This large home building concern is headquartered in Atlanta, GA. Beazer Homes builds communities primarily in Arizona, California, Nevada, Texas, Delaware, Indiana, Maryland, Tennessee, Virginia, Florida, Georgia, North Carolina, and South Carolina. The stock trades around $29.00 a share and sports a market capitalization of approximately $900 million. Beazer’s fiscal year begins on October 1st. Beazer’s fiscal year starts on October 1st.

November Company Presentation

Fourth Quarter Results

Beazer Homes posted its Q42023 numbers on November 16th. It was a stellar quarter for the company by some metrics. The company had a GAAP profit of $1.80 a share, more than 40 cents a share above expectations. 19 cents a share of this was due to tax credits. Revenues did fall 22% on a year-over-year basis to just over $645 million, but that was some $18 million north of the consensus.

November Company Presentation

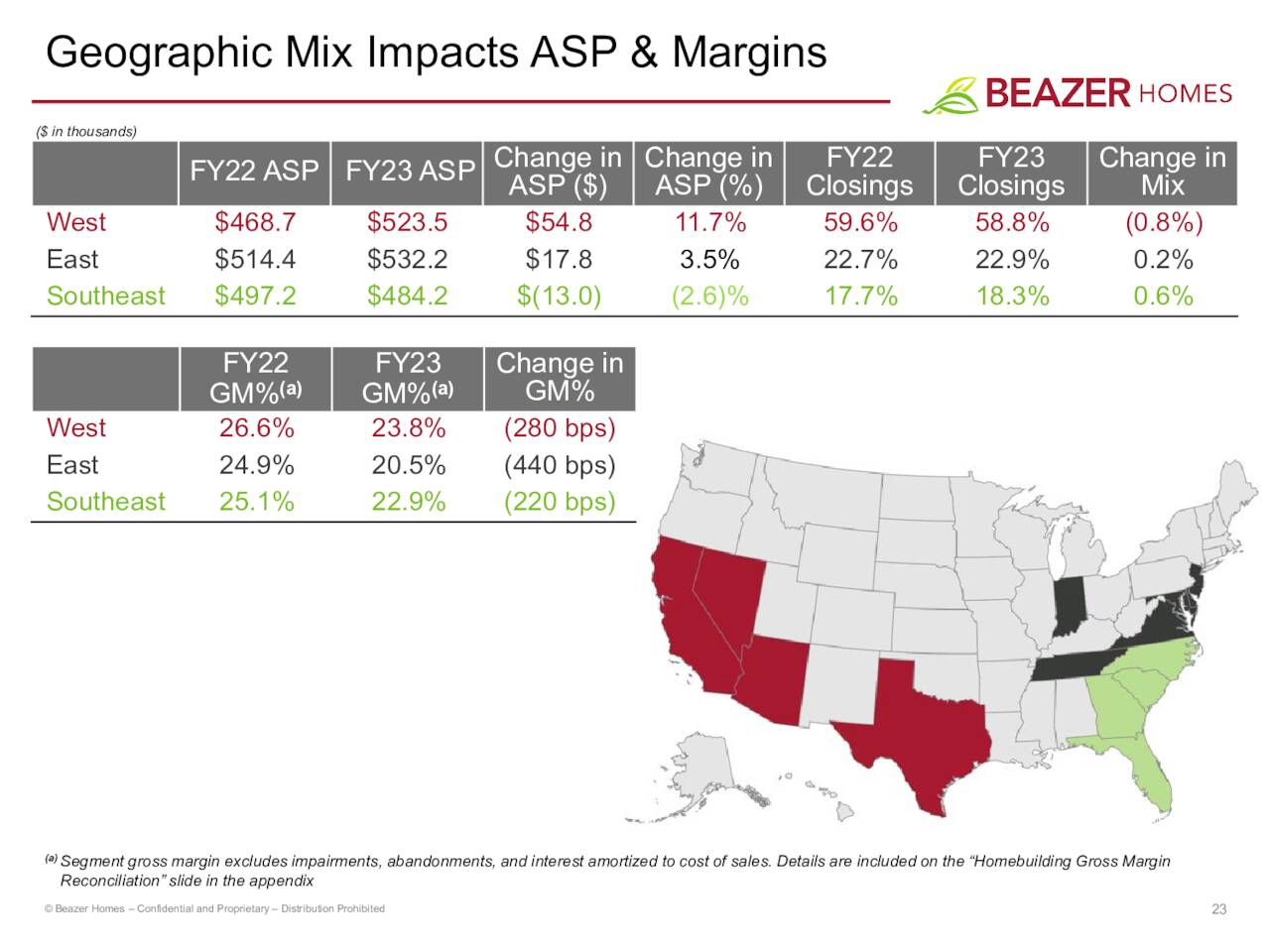

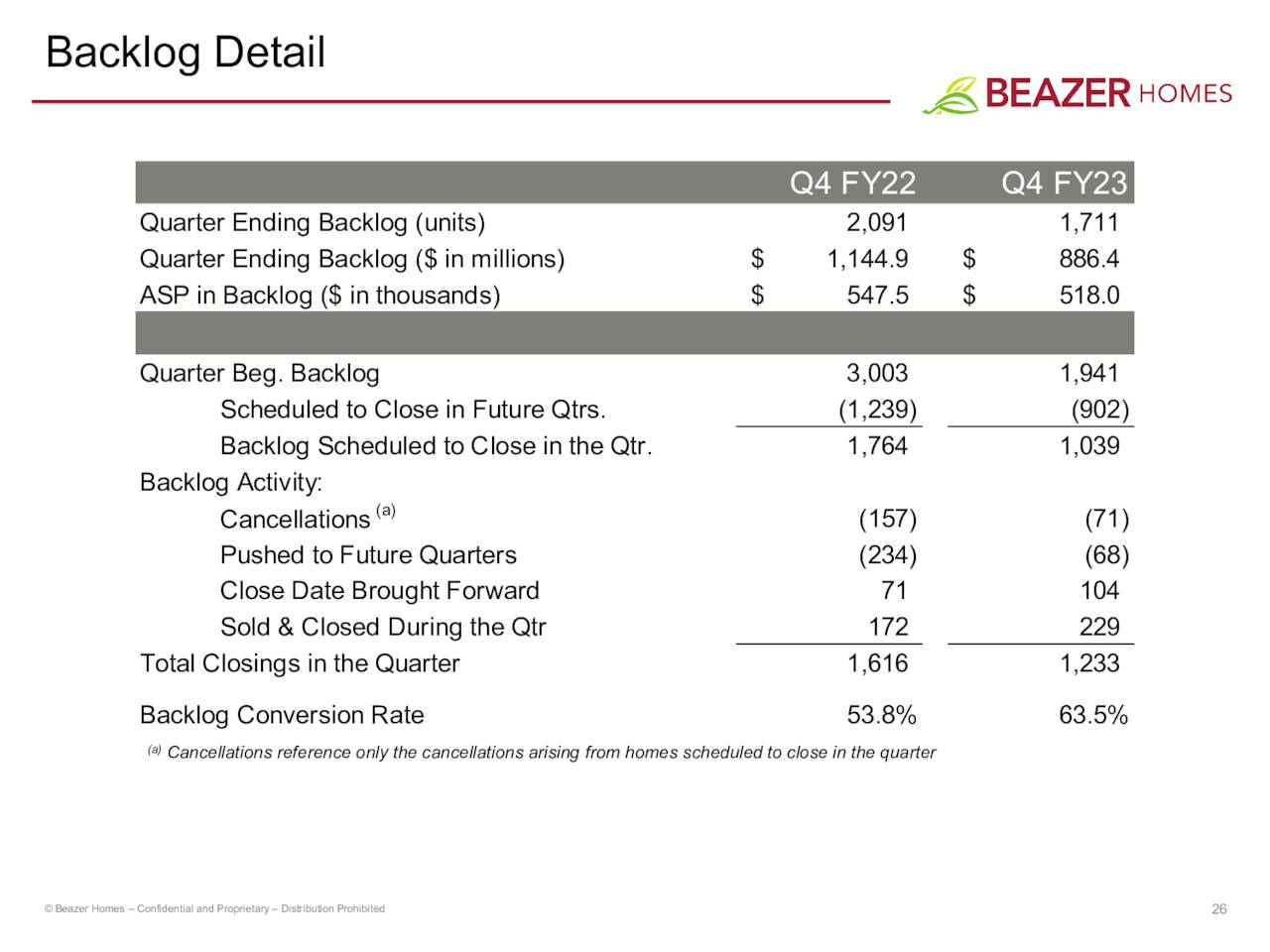

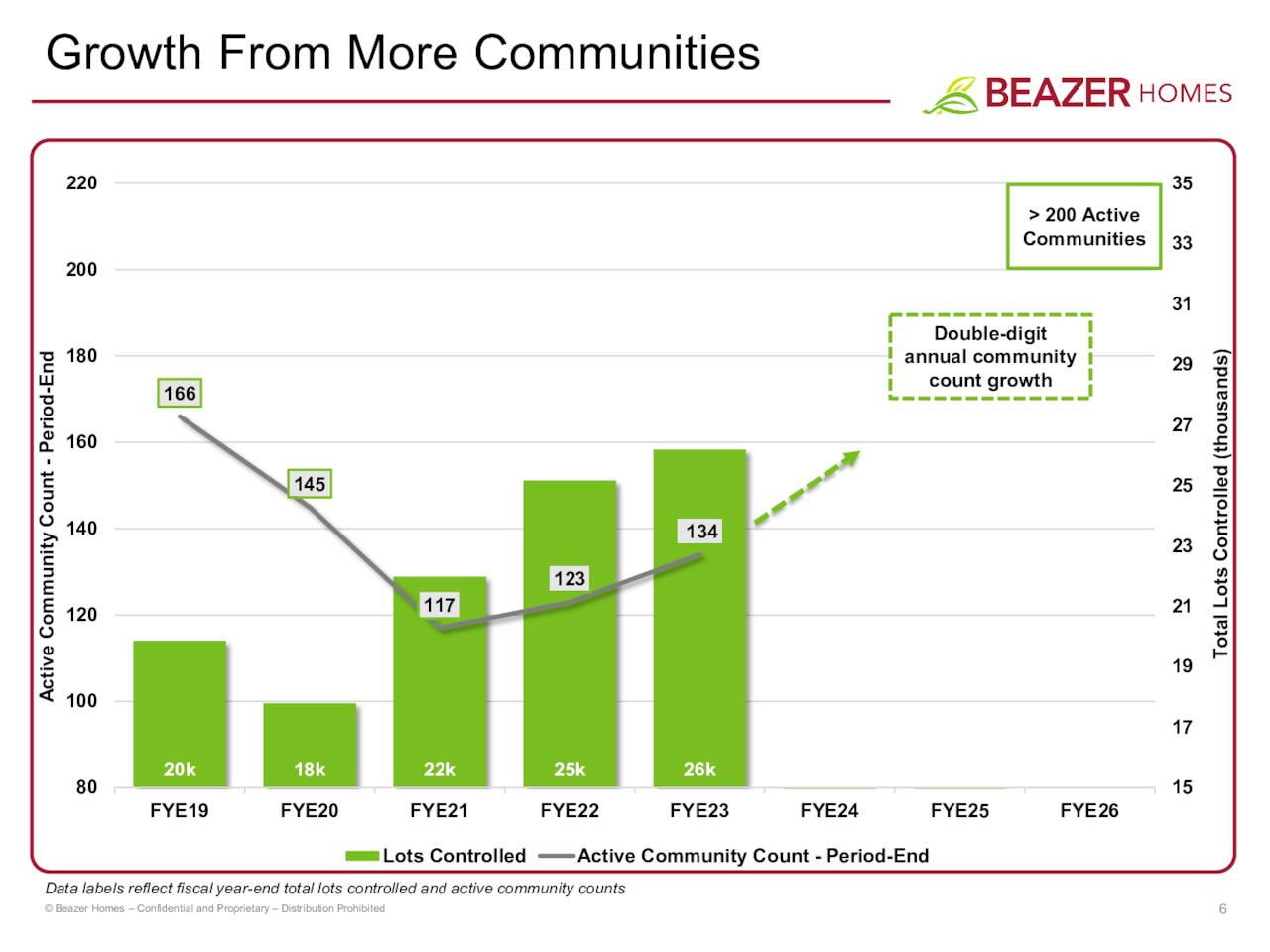

Home closings fell 24% from the same period a year ago to 1,223 while the average home selling priced increased two percent to $520.5 million. Cancellation rates dropped significantly sequentially from the last quarter of Beazer’s FY2023’s year (32.8% to 16.5%). New home orders also rose 43% from 1Q 2023 to 1,003. Community count rose 7 to 130. Finally, the value of the company’s order backlog dropped to $886.4 million from $1.14 billion from the same period a year ago.

November Company Presentation

First Quarter Results:

Beazer posted its first quarter results from its fiscal 2024 year on February 1st. The company delivered a GAAP profit of 70 cents a share, a penny under the consensus. This was down from 80 cent a share GAAP profit in the same period a year ago. Adjusted EBITDA also fell just over 19% to $38 million. Homebuilding gross margin did improve by 70 basis points to 19.9% in the quarter.

Sales fell just over 13% on a year-over-year basis. This was more than $30 million under expectations. Home closings were down nearly 11% to 743 from 1Q2023, while the average sale price dropped nearly four percent. Some of the miss was due to one of Beazer’s key title insurer providers experienced a cybersecurity incident in December. This delayed some closings, which all were completed in January and will be reflected in the next quarterly report.

The brightest part of the quarter was that new home orders surged by just a tad over 70% from the same period a year ago to 823. This consisted of a 50% rise per housing community and a 13.5% increase in the overall community count. Overall backlog order value stood at $932.8 million, down one percent from 1Q2023.

Analyst Commentary & Balance Sheet

B. Riley Financial reissued its Buy rating and $40 price target after third quarter results were posted. After Q3 numbers came out in August, both Sidoti ($36 price target) and Wedbush ($33 price target) upgraded BZH to a Buy. However, Wedbush has since moved to a Hold on the stock.

Approximately four percent of the outstanding float in the shares is currently held short. There has been no insider activity in the stock since May of 2021.

November Company Presentation

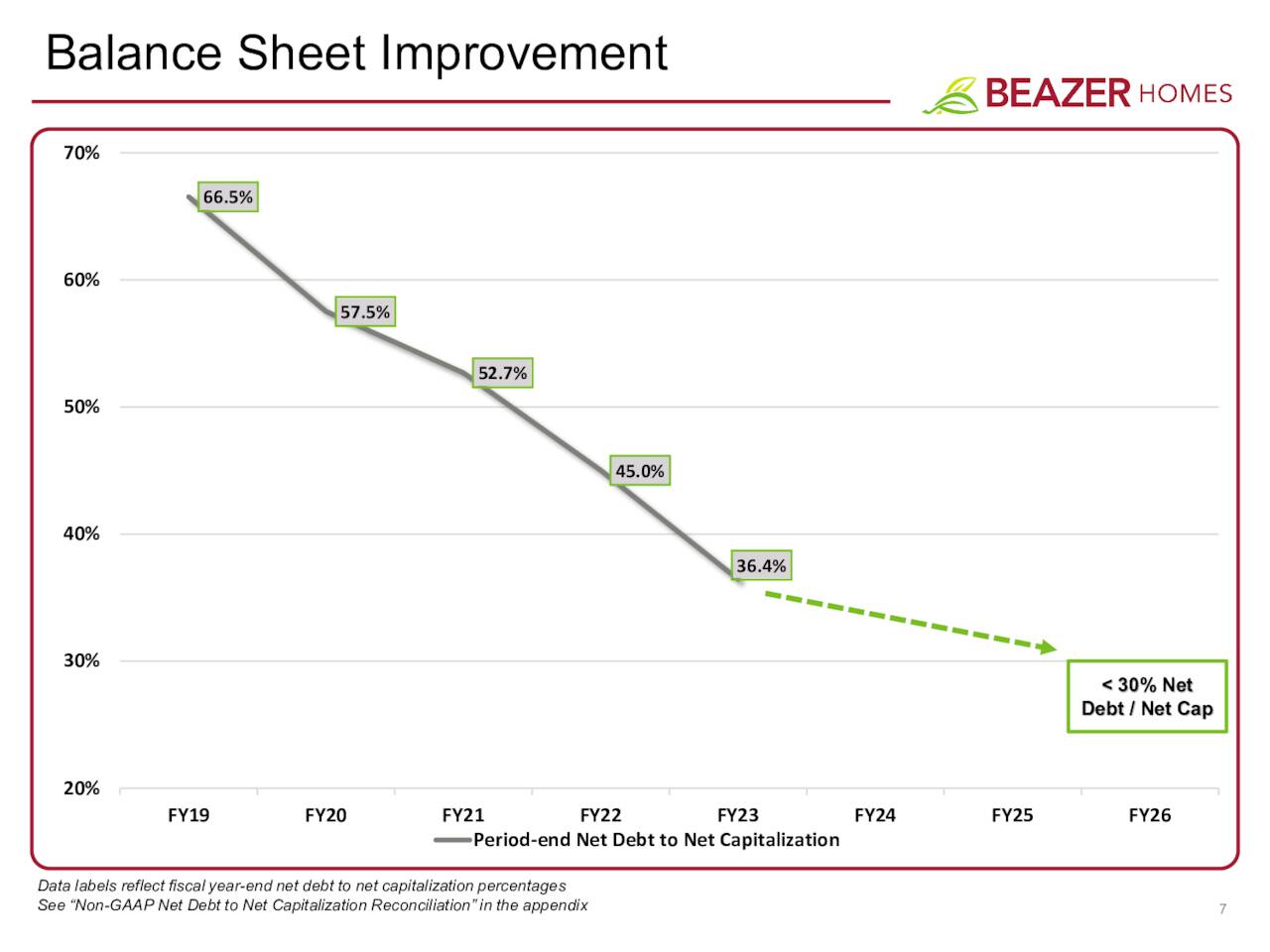

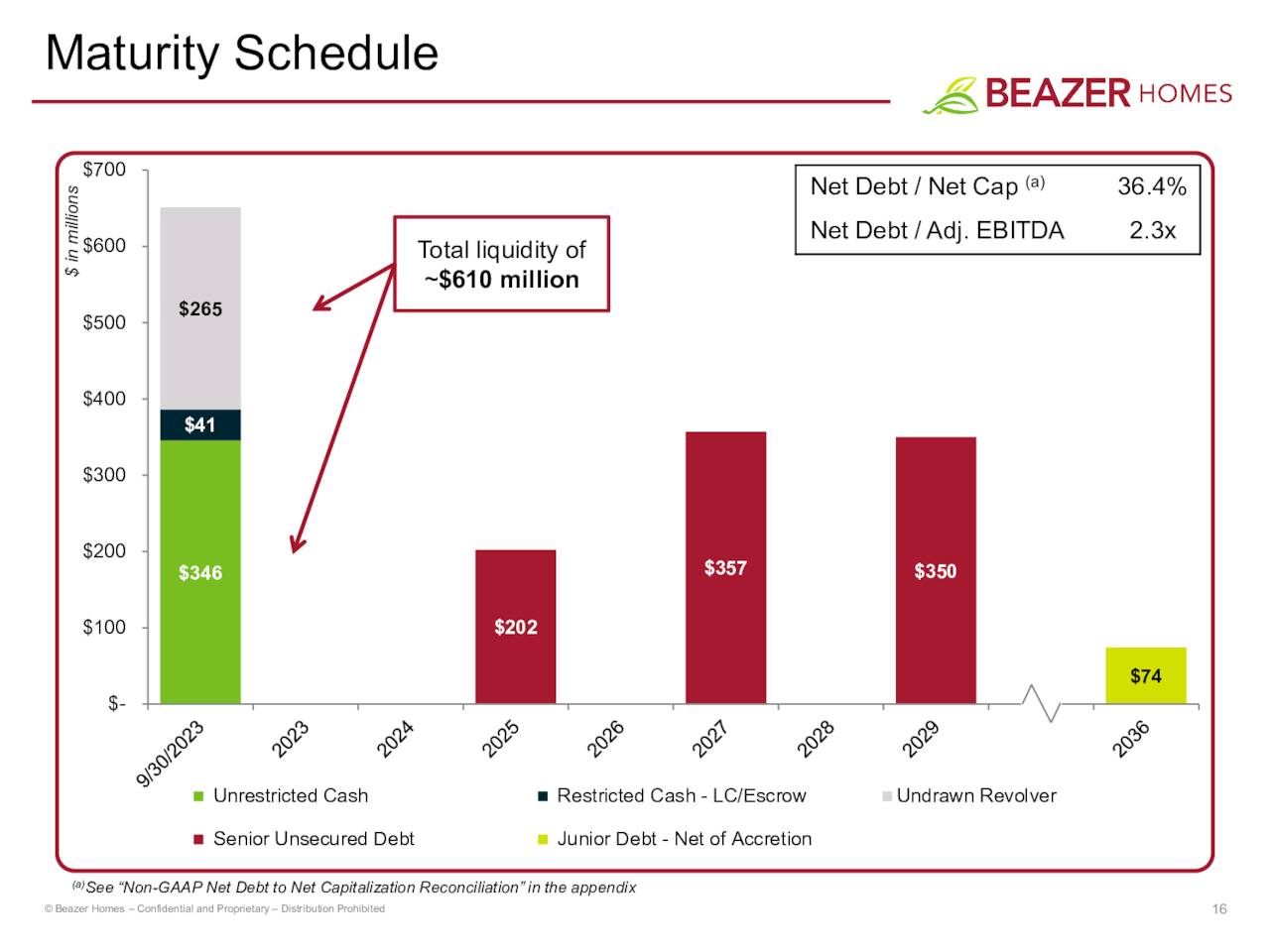

Beazer has done a commendable job of reducing its leverage ratio in recent years, and its balance sheet is in good shape. Total liquidity stood at just over $400 million at the end of the most recent quarter. The total debt to total capitalization ratio fell 410bps to 46.5% from the same period a year ago.

November Company Presentation

Verdict

Beazer Homes made $5.16 a share on $2.21 billion in revenues in FY2023. The current analyst firm consensus has Beazer’s profits falling to $4.71 a share on $2.38 billion in FY2024. The project that profits will rebound in FY2025 to $5.63 a share on 10% sales growth.

Outside recessions, home building stocks typically sell for half or less of the overall market multiple due to their cyclicality. Currently, BZH is selling for less than seven times this year’s projected profits per share. The stock pays no dividend.

November Company Presentation

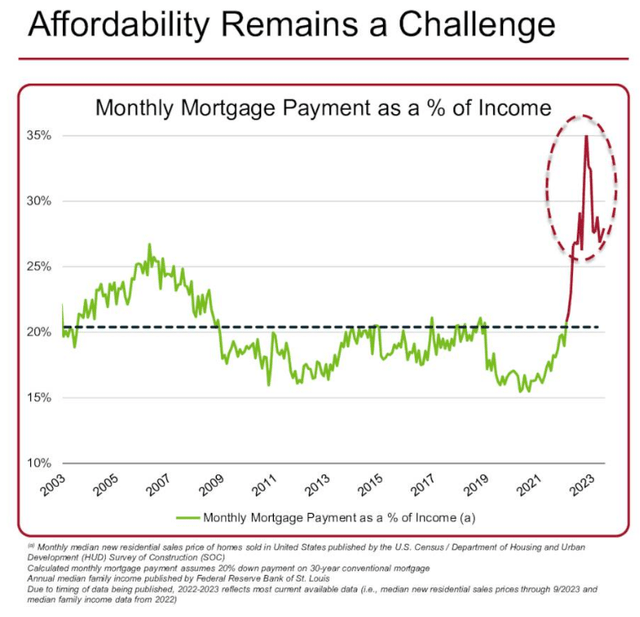

Housing affordability continues to be a significant challenge as the company itself pointed out in its most recent investor presentation. In addition, we are starting to see some deterioration in home builder business models early in 2024. Home building giant D.R. Horton (DHI) was smacked around by the market earlier this month after the company reported 1Q2024 results. The stock fell almost 10% on the day. This was the shares worse daily performance since 2020. New order sales disappointed and gross margins also fell 220bps sequentially from the previous quarter to 22.9%. The huge home builder was forced to offer additional incentives such as mortgage rate buy downs to move inventory.

The yield on the 10-Year Treasury has backed up over 25bps since Friday’s stronger than expected January BLS report. This obviously will trigger a corresponding rise in average mortgage rates, which will be a headwind for the home building sector. While BZH is cheap on many metrics, I continue to remain underweight this sector of the market due to economic uncertainty and the current challenges this industry is facing.

Those who would give up essential liberty to purchase a little temporary safety, deserve neither liberty nor safety.“― Benjamin Franklin

Read the full article here

")

")