")

Q4 2024 Earnings Call Transcript")

")

")

")

Trading at a big discount to its portfolio’s value with a juicy yield, Barings BDC (NYSE:BBDC) looks like an option for risk-tolerant investors looking for yield.

Company Profile

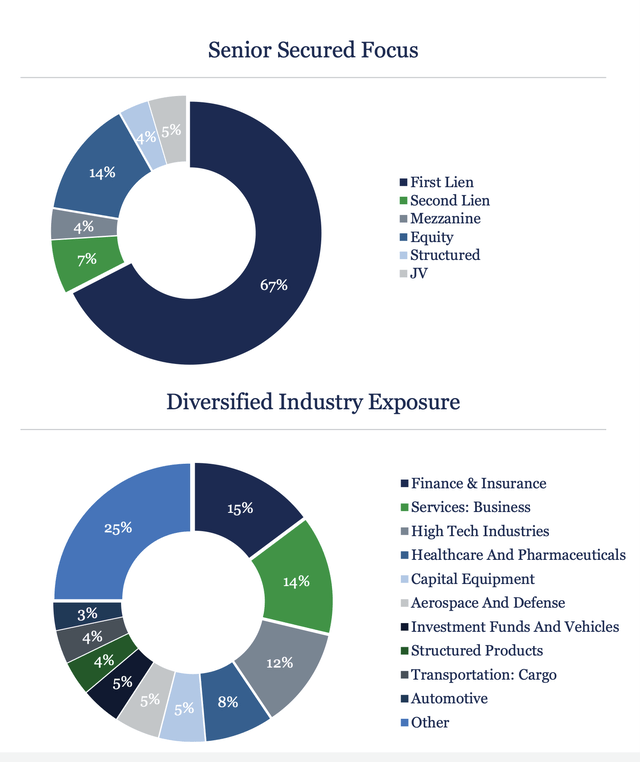

BBDC is a business development company (“BDC”). It looks to invest in the debt and equity of middle-market companies that typically have EBITDA of between $15-150 million. The firm primarily invests in first lien debt with 67% of its portfolio in these types of loans at the end of Q3. Approximately 14% of its portfolio was in equities at the end of Q3, followed by 7% in second lien loans, 5% in mezzanine debt, and 4% each in structured debt and joint ventures.

BBDC has a diversified portfolio, with investments from 335 different issuers. Its largest industry exposure at the end of Q3 was Finance & Insurance at 15%, followed by Business Services at 14% and High Tech Industries at 12%. Approximately 89% of its loans had floating rates at the end of Q3.

Company Presentation

BBDC’s investment advisor is Barings, which is a subsidiary of insurance firm MassMutual.

Opportunities & Risks

BDCs are largely about risk management, and on that front, BBDC appears to have a bit of a larger risk appetite than some rivals. This can be seen in the firm’s portfolio make-up, where 33% of its investments are lower down the capital structure from first lien secured notes.

BBDC has also gone out and bought entire portfolios since the pandemic, purchasing MVC Capital in December 2020 and Sierra Income in February 2022. In both cases, Barings decided to offer credit support against losses of $23 million and $100 million in realized and unrealized losses from their respective investment portfolios over a 10-year period.

Now, it is notable that if aggregate realized and unrealized gains exceed aggregate realized and unrealized losses, no credit support is required with these agreements. In addition, settlement isn’t until the earlier of when the entire portfolio has been realized or written off, or at the end of the agreements, which is January 2031 for MVC and April 2032 for Sierra. Any losses, meanwhile, will initially be covered by waiving incentive fees for the next four quarter afterwards, and then a payment for the rest, if any.

The two CSAs are valued at $54.2 million on its balance sheet, or about 51 cents per share. This value will move up or down based on the realized and unrealized gains and losses as well as the discount rate being used. But the changes in the CSAs and investments at fair value should even themselves out, not impacting its NAV.

The value of the CSA at the end of Q3 is up from $49.5 million a year ago, but down from $60.7 million at the end of June. BBDC’s net asset value, meanwhile, has remained pretty steady, coming in at $11.25 at the end of Q3 versus $11.28 a year ago.

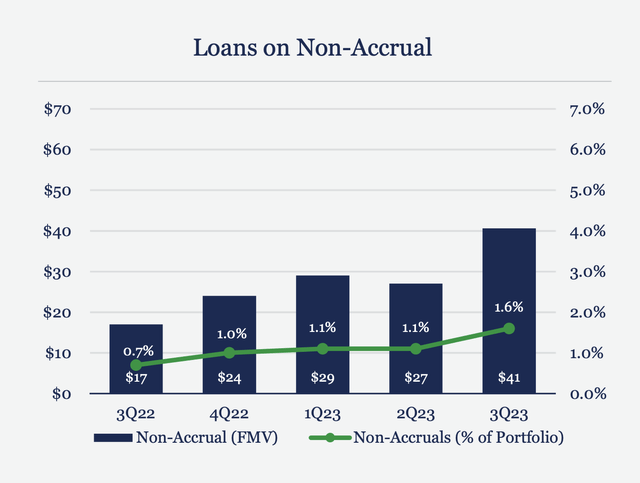

The company has experienced non-accrual investments, with much of them coming from its two acquired portfolios. However, the portfolios have performed fairly well, overall, with less than $35 million in net losses having been realized as of the end of Q3.

Total non-accruals in Q3 were 2.5% of its portfolio on a cost basis and 1.6% at fair value. Only two non-acquired investments were on non-accrual in Q3, while 5 investments from acquired portfolio investments were on non-accrual status. The company also restructured three investments, which is also a sign of potential credit issues down the road.

The credit quality of its portfolio overall has held up well, now it is also notable that non-accruals have been ticking up, which is something to continue to monitor. If the economy worsens, this could become more of an issue.

Company Presentation

With most of its loans floating rates, interest rates play a role in BBDC’s performance as well. The rise in interest rates has increased BBDC’s weighted average yield on its debt securities to 10.6% at the end of September. That’s up from 8.6% a year ago. This has led its investment income per share to rise 19% to 31 cents from 26 cents a year earlier.

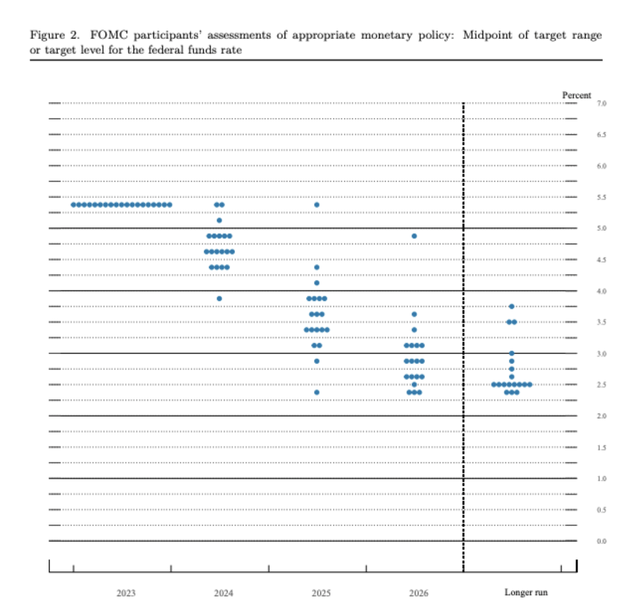

A shift in interest rates, which the Fed suggested it could do in December, is a risk. The Fed is still projected to lower rates three times in 2024 even after they held rates steady in late January, but the first cut isn’t expected until May or June now. Secured Overnight Financing Rats (SOFR) were basically unchanged on the news and remain elevated at over 5.3%.

FOMC

For its part, BBDC provided some preliminary results in late January. It projected NII of between 30-32 cents. Meanwhile, it’s looking for its NAV to end up between $11.25-11.29. The company had 1.15x net leverage at the end of the year.

At the end of December, it had four portfolio companies on non-accrual status, representing 2.5% of its cost and 1.6% at fair value. After the quarter, its investment in bitcoin mining company Core Scientific (CORZQ) was removed from non-accrual status, and it exchanged its debt for equity as the company exited bankruptcy.

Overall, BBDC has been a steady performer in 2023. Its NAV has moved from $11.05 at the end of 2022 to about $11.27, a 2% increase. At the same time, its net investment income has been at a steady 31 cent per share the past three quarters of 2023 if it hits the midpoint of its recent update. The only negative is that the percentage of its portfolio on non-accrual status has ticked up slightly, which is something to continue to monitor.

It’s also worth noting that BBDC has a large equity investment in Eclipse Business Capital, which provides revolving lines of credit and term loans secured by collateral such as accounts receivable, real estate, machinery or inventory. It also has a large preferred share investment in Rocade Holdings, which provides financing to plaintiff law firms engaged in mass tort. These two investments add both risk and opportunity given their size and structure.

Like other investment portfolio companies, BDCs typically are valued at a price to book or NAV. Based on the mid-point of its estimated year-end NAV, it trades at a 0.79x NAV. According to BDCInvestor.com, BDCC has the 10th lowest P/NAV of the 48 BDCs it tracks.

Conclusion

Given its portfolio make-up, BBDC does carry more risks than some other BDCs, as it has exposure to two large equity investments and only two-thirds of its portfolio is in first lien loans. However, it’s done a fair job with regard to credit quality, and its two CSAs do help protect its NAV to the downside with regard to the portfolios it bought. I’d just continue to monitor its credit quality and loans on non-accrual status.

Yes, given that only 67% of its portfolio is in first lien loan does add some risk, but with the stock trading at 20% discount to NAV, this risk seems to be more than reflected in its share price. At the same time, the strength of the economy has been holding up well, despite earlier fears that it would spin into a recession. Its equity positions in Eclipse and Rocade, meanwhile, are generally considered uncorrelated to the economy.

Overall, I think the discount to NAV for BBDC is too much, and I could see the stock trade up to 0.9x, which is still a discount reflecting its somewhat riskier portfolio. As such, I’m going to start the stock with a “Buy” rating and $10 target. The stock currently has a 11.8% yield.

Read the full article here

")

Q4 2024 Earnings Call Transcript")

")

")

")