")

")

Introduction

I recently pulled the trigger and opened a small position in Axcelis Technologies (NASDAQ:ACLS), so I wanted to outline the three reasons why I decided to finally start a position. It is a great company in a niche area of semiconductors, specifically ion implantation, in which it holds the biggest share globally. The company’s products are top-of-the-class in the ion implant business, and the continuation of improvements and laser focus of the company on these products will make sure to keep them at the top of the demand.

In the League of Their Own

When it comes to ion implantation, ACLS is an undisputed leader in the category. I always like to own companies that possess the moat and have an advantage in their specific field. ACLS is in a league on its own. There have been reports in the past that the company held anywhere between 70% to 80% of the ion implantation sales worldwide, however, I couldn’t find any concrete evidence to support that currently, however, if we look at what the company made in 2023, and what total sales have been reported in the ion implantation business for the same year, we can see that ACLS is not far off that number. According to this report, the global ion implantation market was valued at $1.85B in 2023 and is forecasted to grow at a respectable 6.6% CAGR from 2023 through 2030. In 2023, ACLS saw $1.13B in total sales, which is around 61% of the total value of the business segment. So, not quite 70% or 80% but given the downturn in the semiconductor industry, it is still a good result, which still leaves the company as THE company for ion implantation needs.

Other companies do ion implantation, for instance, Applied Materials (AMAT), which is a much bigger company overall, however, AMAT’s focus is not ion implantation, and given the market share that ACLS took in 2023, AMAT’s piece of the pie is much smaller.

The advantage of owning ACLS is that they are more focused on ion implantation, which made up over 90% of its total sales year after year. They are the leader in such a specific area, known for its innovative implanter technology, and catering to specific market segments like silicon carbide or SiC. Being laser-focused on a specific segment in semiconductors allows for higher knowledge in the design and manufacturing process and staying on top by committing most if not all available resources to further develop new tools that help the process to be more efficient and profitable. So, why AMAT may be a dominant player in the overall semiconductor market, a leader in a niche market like ion implantation goes to ACLS.

I mentioned that the market is going to grow at around 6.6% CAGR over the next 7 years. However, I believe ACLS will see a much higher growth number than the average given its position as the leader and expect to see low-double-digit growth for the next few years, except for FY24, however, these are my assumptions, and we won’t know for sure of the extent of the recovery going forward.

Position in Silicon Carbide

A significant amount of the company’s revenues come from silicon carbide or SiC. SiC continues to be in high demand and given the position of ACLS as a leader in SiC implantation with the company’s Purion Power Series, the company will capture that growth going forward. That still holds for the long term. However, there are inklings of some sort of slowdown in demand for SiC due to oversaturation. One of the company’s main end markets, the EV segment, has seen a substantial slowdown in demand recently, which was quite surprising, especially when many researchers forecasted robust growth numbers for the next decade. EVs require SiC components, therefore the lower expectations of sales of EVs may put a damper on ACLS’s total revenues in the short run, however, SiC will remain in high demand over the long run given its many advantages over traditional silicon for power device applications, such as increased efficiency, higher operating temperatures, and a higher breakdown voltage.

With the slowdown in EV adoption, the slack is being picked up by hybrid EVs, or HEVs, so even if the adoption of EVs has seen some obstacles due to them being still too expensive to own, I like that there is a bridge that will get us eventually to full adoption to EVs when we are ready, or should I say when those cars are at least on par with costs of traditional ICEs.

In the long run, the demand for SiC is outstanding. The SiC market is expected to grow at a whopping 32.6% from 2024 through 2029. ACLS’s Purion Power series is top-of-the-line and will be in high demand going forward. We can see these products already being in demand. Back in April, ACLS announced multiple shipments of the series, specifically, the Purion H200 SiC high current, Purion XE SiC high energy, and Purion M SiC medium current implanters. This gives me confidence that the slowdown in SiC is only temporary, and the company will continue to see decent sales going forward.

Outstanding Financial Position

Another reason I think the company is going to be a winner in the long run is its financial position. As of Q1 ’24, which was filed on May 2nd ’24, the company had around $530m in cash and short-term investments while still having no debt outstanding. This position is ideal for any kind of downturn.

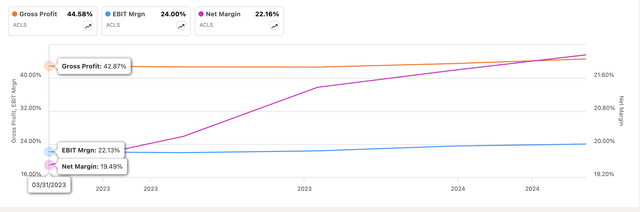

Even during the tougher year of 2023, the company managed to increase its margins across the board, which tells me that the management is more than capable of directing the company’s resources according to what is going to hurt its operations or not and cut off some part of production early on, so as not to waste resources and adjusting the product mix accordingly to maintain or in this case improve efficiency and profitability.

Seeking Alpha

The management mentioned that they are retiring the company’s incentive program, which should affect gross margins in the second half of the year, so I expect further operational efficiency to kick in.

The company’s cash from operations seems to have bottomed out. However, I expect more volatility in the short run to occur due to the mentioned slowdowns in many end markets in which the company operates.

In short, I believe being a niche player is going to continue to be an advantage to ACLS. SiC in the long run has a strong growth trajectory, which no doubt will help the company grow its top line also. The company’s financial position is immaculate in my opinion, which should help it weather any sort of downturn in the short run successfully.

Risks

Of course, no investment comes without risks, and ACLS is no different. The same risks remain as in my previous article, so I will cover them briefly.

Many investors who due deep research on which stock to buy may find that ACLS is heavily dependent on China. A lot of investors tend to avoid such companies due to the uncertainty factor when it comes to relations between China and the US. Many Chinese companies have been put on the Entity List, including ACLS’s major client SMIC. So far, the company managed to ship to most if not all of its clients in China, but that may change in the future if relations worsen. I think the risk is valid and would like to see the company putting a lot more effort into diversifying away from the Asia Pacific region.

The continual softness in the EV market will potentially weigh on the company’s top line. But as I said earlier, this will be short-lived because many governments are pushing for further electrification. Furthermore, to bridge the gap between ICEs and EVs, a nice alternative the HEVs will soften the blow to the global sales of vehicles and ACLS’s top line.

As with the slowdown in EV adoption, the slowdown in SiC demand will certainly play a decent role in the company’s lackluster performance over the next year or so, however, as we saw above, the demand for SiC is robust in the long run. Therefore, the softness will also be short-lived.

Closing Comments

The long term remains very positive in my opinion. Do I expect the share price to just skyrocket going forward? No, I don’t. I don’t even want it to do that because I recently started a small position and would like to get in on an even lower price because a lot of analysts are expecting softer demand overall, which should bring the company’s share price further. And when that happens, I will be ready to add on the weakness, which in the long run, should be no big deal.

Therefore, I am reiterating a buy and believe that the reasons outlined above are reasons enough to warrant a position in a portfolio that is looking to add a leader in its field, with a great balance sheet, and a great outlook in the long haul.

Every investment has risks, and my thesis may change with time if something serious comes out of the upcoming couple of earnings reports, so I will be analyzing the numbers and the outlook like a hawk over the next year or so to make sure everything is going in the right direction.

Read the full article here

")

")