")

")

Investment Thesis

AutoNation, Inc. (NYSE: NYSE:AN) is a leading player in the US automotive retail industry, with a broad operational footprint encompassing new and used vehicle sales, parts and service operations, and automotive finance and insurance products. The company’s extensive dealership network, brand recognition, and in my opinion, excellent capital budgeting, position it well to capitalize on market opportunities and drive long-term value creation.

AN operates 347 new vehicle franchises from 251 stores across the US, with a concentrated focus on the Sunbelt region. The company sells 32 different new vehicle brands, with core brands including all the majors (Toyota, Honda, Ford, BMW, and so forth). The company also owns and operates 52 AutoNation-branded collision centres, 23 AutoNation USA used-vehicle stores, and 4 AutoNation-branded automotive auction operations.

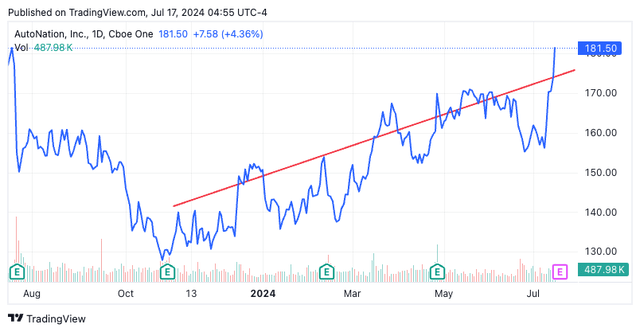

Figure 1.

Tradingview

Shares have just broken out of an ascending channel to the upside and I am buy on AN due to 1) exceptional economics [>20% ROICs + persistence in this advantage, with ~4.5x capital turnover + ~7x inventory turnover, sees it throw off ~$1.5Bn in FCF each quarter], 2) management’s stewardship of capital [it has been aggressively buying back stock as you’ll see], and 3) valuations that support ~$214/share today with CAGR ~8-10% to FY’26E. Net-net, rate buy.

Why AN is a great business

I say great and not exceptional or wonderful here for a couple of reasons – 1) its return drivers, 2) capital efficiency + inventory utilization, and 3) management’s capital budgeting decisions.

Starting with the value drivers:

-

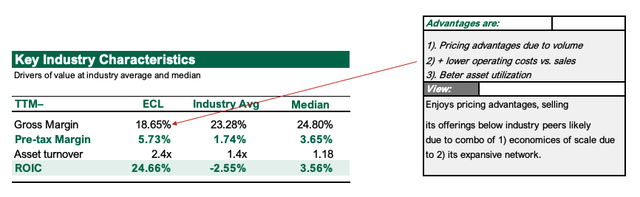

- There are several competitive advantages AN enjoys vs. the industry, including – 1) pricing advantages due to volumes, 2) lower operating costs vs. sales, and 3) better asset utilization leading to 4) ~6x higher ROICs vs. the median peer. It enjoys pricing advantages by selling its offerings below peers. It achieves this through its 1) economies of scale via its expansive network, 2) shrewdest buying that ensures inventories are managed well, 3) is therefore able to sell offerings at all points along the price spectrum, competing with all vendors at these price points given its economics [e.g. in Q1’24 management said “the average selling price of new vehicles decreased 5% resulting in a new vehicle revenue increase of 2%”, + sales of units <$20,000 were +500bps YoY], and 4) because of these three points, enjoys tremendously wide consumer penetration. The breadth of offerings/consumer penetration has immense advantages to profit mix too [parts and service operations, which contributed ~46% of total gross profit in Q1 FY’24 despite comprising only ~18% of total revenue].

Figure 2.

Seeking Alpha. author

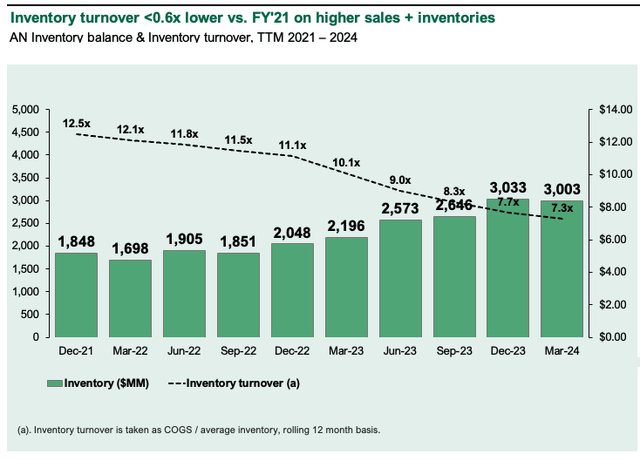

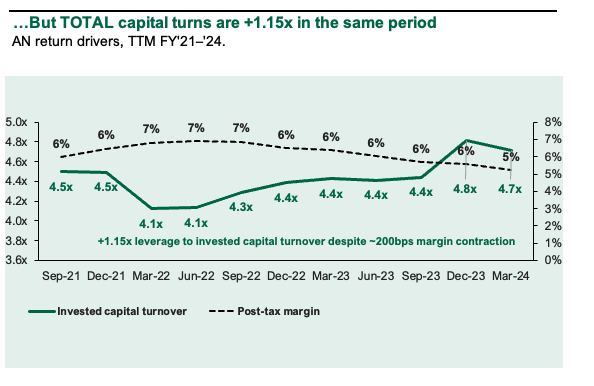

Management deserves high marks for its inventory management and optimization – new vehicle inventory units in Q1 ’24 were 38,185, up from 21,176 YoY with total inventory values >$3Bn (Figure 3). Inventory turnover is ~0.6x that of FY’21 range, with +$1.2Bn surplus. It’s added ~$1Bn of inventories every 12 months from Q2 FY’23-date. In my view it is highly unusual to see ~$3Bn inventory turn over 7x every 12 months producing ~$21Bn in trailing revenues. Secondly, turnover on all capital invested is +1.15x in the same period (Figure 4).We have invested assets returning ~$4.70 in sales per $1 put to work in the business, whilst post-tax margins are ~100bps tighter [unsurprising as FY’22 was due to abnormally high used car prices].

Figure 3.

Company filings

Figure 4.

Company filings

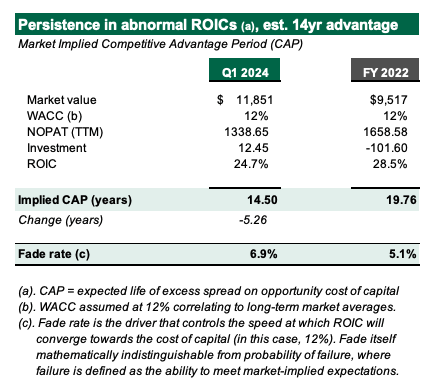

- ROICs are 1) >25% on an ongoing basis, implying 2) AN’s competitive advantage period is ~14.5yrs – the competitive advantage period (“CAP”) is the est. length of time a business can sustain its returns >12%, our minimum accepted return (“MAR”). My view is management as excellent grasp on the balance sheet + industry dynamics are favourable. Thus my forward estimates [see: Appendix 1] provide for ~7% fade rate to the MAR [which would take ~14.5yrs] if correct. Note this is down from FY’22 but unmeaningfully.

Figure 5.

Author, company filings

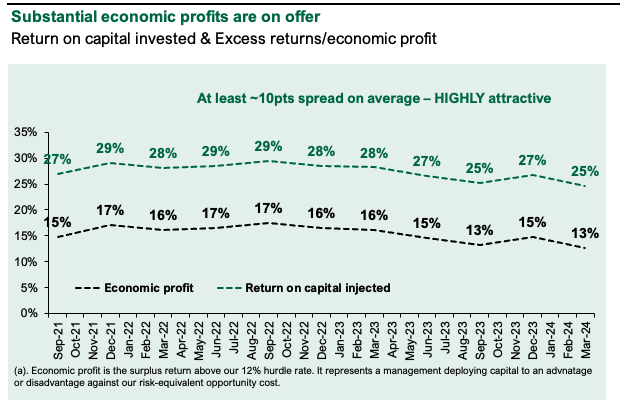

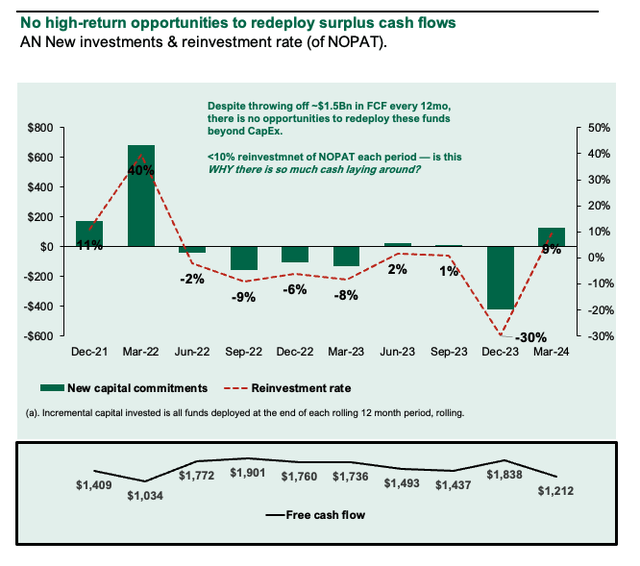

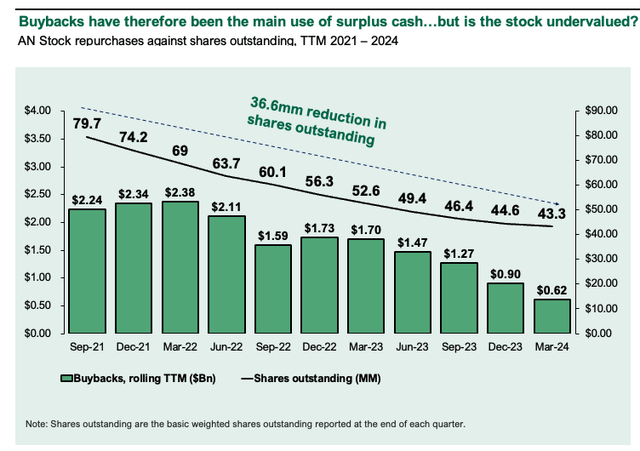

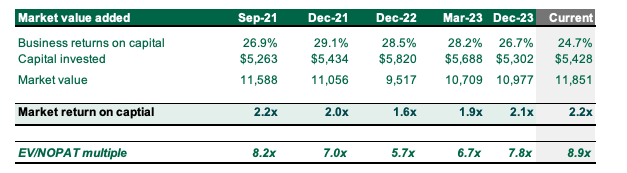

- Such exceptional returns on capital employed into the business produces ~10pts spread above the 12% hurdle rate at least – this is highly favourable and warrants a premium of market value to capital injected into AN’s operations. I said earlier that AN is a great not wonderful business.The question is if AN’s returns are so spectacular why’s it valued at ~9x NOPAT? Answer is simple: It has no high-return opportunities to deploy the funds — since FY’22, despite throwing off ~$1.5Bn every 12mo management has only reinvested ~5% of NOPAT on average (Figure 7). Buybacks have been the primary use of surplus funds (Figure 8) with the sharecount down ~36mm since FY’21. As such, with ~22% incremental ROIC, only ~20% was put back into the business, the remainder kept as cash or buybacks. Investors now enjoy ~$28/share trailing NOPAT on ~$125/share capital invested, 25% ROIC [inc. all buybacks, the owner earnings are $42/share].

Note: If AN were a ‘wonderful’ business under this standard, it would have opportunities to redeploy up to 100% of FCF into new high-return projects. It just doesn’t live in that phase of the cycle. Hence why capital is returned to shareholders instead.

Figure 6.

Company filings, author

Figure 7.

Company filings, author

Figure 8.

Company filings, author

Attractively valued with high margin of safety

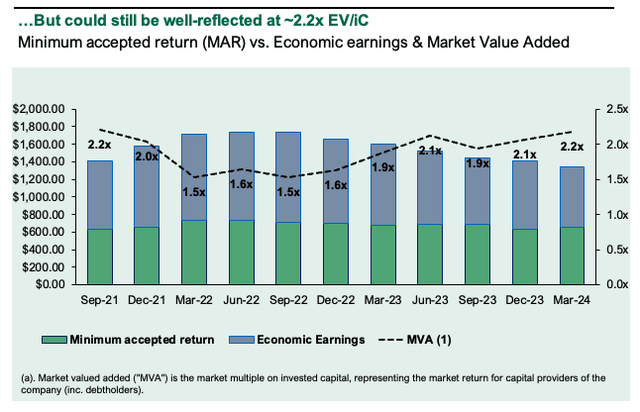

The error for failure is low in buying AN at ~9x NOPAT based on several provable facts. The expectation for 1) persistence in ROICs, 2) future earnings growth and 3) perhaps future buybacks, see AN priced back at ~2.2x EV/IC [in line with FY’21]. The question is what’s the propensity for further expansion from this. My view is the stock is worth ~$215 today with a compounding ability of 8-10%/yr to FY’26E.

Figure 9.

Company filings, author

Valuation insights

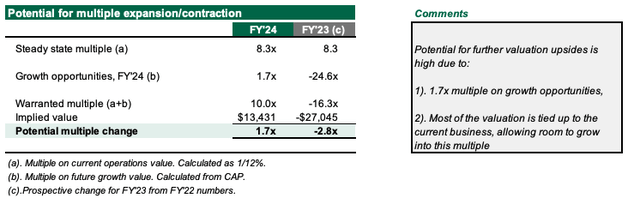

- With the stock at ~2.2x EV/IC and ~9x NOPAT, my view is the scope for these expand is high. Taking a commodity multiple of 8.3x [which is a firm earning ~12% ROIC, thus creating no value i.e. 1/0.12 = 8.3x], my view is AN’s future growth opportunities deserve a ~1.7x multiple, thus meaning a 1.7x propensity for expansion to ~15x NOPAT in the upside case (Figure 11). If this is a ‘cap’, any expansion below this is highly accretive as well. Thus most of the valuation is tied up to the current business, allowing it room to grow into this multiple.

Figure 10.

Author

Figure 11.

Author estimates

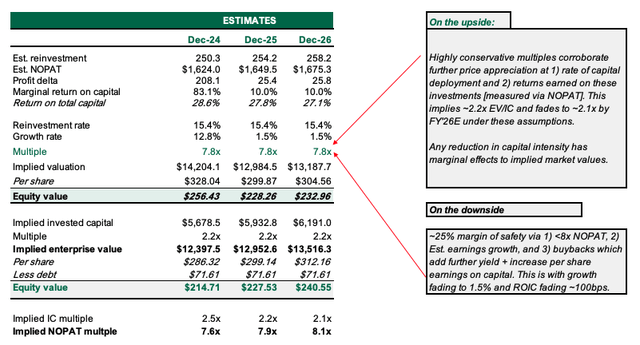

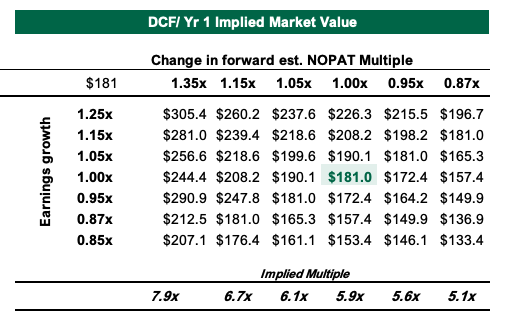

- On the upside, running highly conservative multiples of ~7.8x on my FY’24–’26E estimates [see: Appendix 1] gets us to ~$232/share or ~8-9% CAGR. This = ~2.1x capital, and is thus reasonable. If it were to hold the 2.2x EV/IC range, my view is AN is worth ~$214/share today with $232-$240/share as the objective in 3yrs time. Again, this assumes ~8x NOPAT – more than reasonable. On the downside, there is ~25% margin of safety via 1) the <8x NIPAT< 2) Est. earnings growth fading to ~1.5% and ROICs fading ~100bps. In other words, these are highly conservative assumptions that still get us over the line, leaving widening the margin for error. Even a 5% contraction to ~8.4x EV/NOPAT (equal to ~5.5x P/NOPAT) we have margin of safety with just 5% earnings growth (Figure 13). Say 5% expansion/5% growth, this implies ~$199/share – asymmetrical upside with tremendously low hurdle to overcome.

Figure 12.

Author

Figure 13. Note: implied multiple = P/NOPAT vs. EV/NOPAT

Author

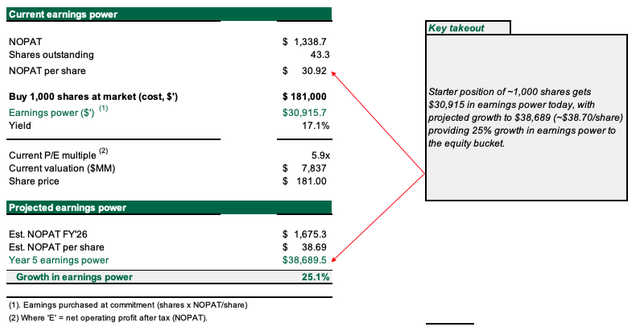

- Subsequently a starter position of ~1,000 shares gets us $30,915 in earnings power [vs. $181,000 cost = 17.1% yield/return on market capital] – and this may very well compound 25% to $38,700 by FY’26E under my assumptions. This supports a buy.

Figure 14.

Author

Risks to investment thesis

Downside risks to the thesis include 1) ROICs, falling <20% [I give this a low-probability weighting], 2) inventory turns <5x [this would be caused by higher inventory days in my view, meaning the business isn’t moving units out the door at as fast a pace], and 3) the broader set of macroeconomic risks that must be factored into all equity evaluations right now, namely the risk for higher inflation data, and another unforeseen rate hike.

Investors must know these risks in full before proceeding any further.

In short

AN presents with mouth-watering economics that see it persistently earn >25% on all the capital that’s been put to work in the business (inc. all inventories). Turnover on this capital is ~4.7x meaning the investment required to produce $1 in sales is only ~$0.21, whilst it is set to turn over ~$3Bn inventory balance 7x this year. My view is the business is worth ~$214/share today at ~8x NOPAT, leaving >25% headroom in margin of safety. Net-net, rate buy.

Appendix 1.

Author estimates

Read the full article here

")

")