")

")

")

")

")

Investment summary

My previous investment thoughts on Arrow Electronics (NYSE:ARW) (published on 23 May) was a buy rating, as various indicators have pointed to ARW reaching the end of this cycle. I remain buy-rated as the timing of a recovery cycle is getting increasingly visible and, by my estimate, should happen in 4Q24.

2Q24 results update

Released a few days ago, ARW once again reported positive results that support my bullish views on the stock. Total revenue was flattish sequentially, coming in at $6.9 billion, with Global Components [GC] sales down 3% sequentially to $5.03 billion and Enterprise Computing Solutions [ECS] up 7% sequentially to $1.86 billion. Gross margin was barely down by 20 bps sequentially to 12.3%. Better than expected performance led to an operating EPS of $2.78 vs. consensus estimates of $2.22. 3Q24 revenue guidance now calls for $6.67 billion at the midpoint, with GC sales of $4.7 billion to $5.1 billion and ECS sales of $1.67 billion to $1.87 billion. Operating EPS is guided for $2.20 at the midpoint.

More signs of a cycle turnaround

Redfox Capital Ideas

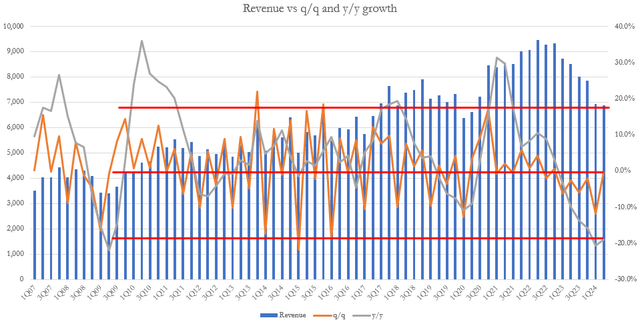

The biggest takeaway from the 2Q24 results is that ARW is one step closer to seeing a strong growth inflection as the cycle turns upwards. As I noted previously, each time sequential growth rates dip below -10%, subsequent periods of y/y growth have been strong, and 2Q24 showed the first sign of this happening. Sequential growth reversed back from -11.8% to -0.5%, which drove the first positive inflection in y/y growth. If you look at the bottom red line that I highlighted above, the current y/y trend has a splitting image compared to the 2007–2009 period.

Various other underlying metrics all point to the cycle moving from the downtrend phase to a stabilization phase, setting up well for the uptrend phase in the next few quarters. For instance:

- ARW saw a sequential improvement in bookings across all regions; notably, overall sentiments have improved at both suppliers and customers’ levels; and

- The book-to-bill trend continues as per last quarter, reaching parity soon, and

- Importantly, the backlog has stabilized (this is a leading indicator of underlying demand) and cancellations have fully normalized (which means the backlog is a reliable indicator of demand).

Comments from some of ARW peers all align with my view that underlying demand is healthy.

As a result, we believe that device demand will improve modestly for the balance of the year. PC Connection Inc 2Q24 earnings transcript

Yeah, I just would like to add that, we see the demand being driven by enterprise and SMB. So these are the two customer segments plus public sector, and which are driving the demand as we speak.

Gen AI requires a lot of compute and a lot of optimization of your infrastructure. So I mean, not only in software, of course, we’re going to see the benefits, but basically companies will have to upgrade their servers, their switches, their storage. So we see the impact of Gen AI being very pervasive across most of our technologies, which obviously is going to be a very nice prospect for the future. So yeah, very positive — again, Gen AI, I think is a very nice opportunity for the IT industry in general and of course, for us in particular. TD Synnex Corp 2Q24 earnings transcript

Inventory continues to trend down

Redfox Capital Ideas

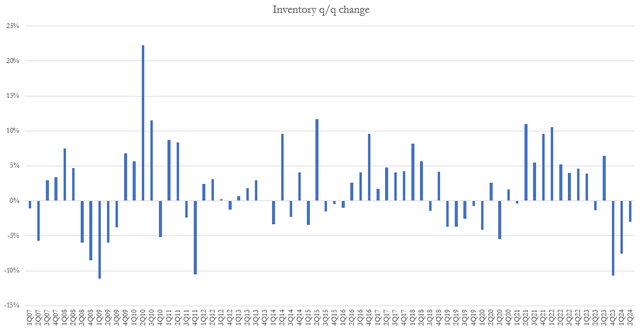

Apart from the signs in the P&L, ARW’s balance sheet also provides signs that a turnaround is imminent. Comparing the current downcycle to the previous major downcycle in the 2007–2009 period (excluding COVID because there was a major supply shock), the current inventory sequential trend is also following the same pattern. A sharp sequential decline is followed by subsequent quarters of decelerating declines.

In the case of the 2007-2009 period, 3Q23 was the end of the sequential decline, which is also the first period that saw sequential revenue growth. Assuming the current cycle follows the same pattern, the next positive sequential growth could very well happen by FY24 (in 2H24). Since management implicitly guided for another sequential decline, it seems more likely for a sequential growth turnaround to happen in 4Q24.

As mentioned, bookings accelerated across all regions, which we believe indicates a further step down in ecosystem inventory levels as well as improved visibility to forward-looking production requirements.

Sure. Well, as I said before, we are managing inventory carefully. We are taking a 90-day view one quarter at a time if you will. We do anticipate that things are getting better here in the near term. I’d say we’re now bouncing along the bottom. 2Q24 earnings transcript

Just for readers that missed my previous post, I reiterate the other positive impacts of a reduced inventory portfolio for ARW:

(1) This frees up cash for ARW to continue returning capital to shareholders. ARW bought back shares every single quarter over the past decade, even during downcycles.

(2) This lifts the pressure on gross margin, as ARW need not continue to provide discounts to clear inventory. I also note here that ARW has done a much better job in this cycle relative to the past, as the trough gross margin is higher than the past 2, implying a higher base for gross margin to expand from in the upcoming cycle

Valuation

Redfox Capital Ideas

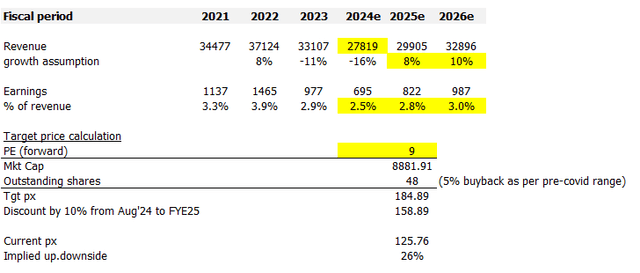

I model ARW using a forward PE approach, and using my assumptions, the upside remains very attractive. My growth and margin estimates have remained the same as I modeled previously. The only change is that my estimate for FY24 revenue has declined from $29 billion to $27.8 billion. This reflects the 3Q24 revenue guidance and my assumption that 4Q24 will see a positive sequential growth uptrend like it did in 3Q09. While this is a decline in my estimates, I believe it has an overall positive impact on stock sentiment, as 2Q24 results instilled more confidence in the market that the turnaround is even nearer (very likely in 4Q24). I hold my valuation multiple assumption steady at 9x, as this is the mid-cycle multiple that ARW tends to trade at.

Risk

I have not made many changes to my views on risk here. I still think the risk lies in the timing of the recovery cycle.

Arrow’s forward visibility remains limited… for all we know, we are still in a downward trend. The global recession is a major macro-risk that should be considered as well. A further slowdown in global economic growth will put further pressure on demand.

Conclusion

My view for ARW is a buy rating as 2Q24 results provided more evidence of an upcycle happening soon. The sequential revenue stabilization, coupled with improving booking trends and inventory management, suggests that a growth inflection point is imminent. While the exact timing of the recovery remains uncertain, I am increasingly confident that sequential growth will happen in FY24.

Read the full article here

")

")

")

")