")

(NASDAQ:ARM)")

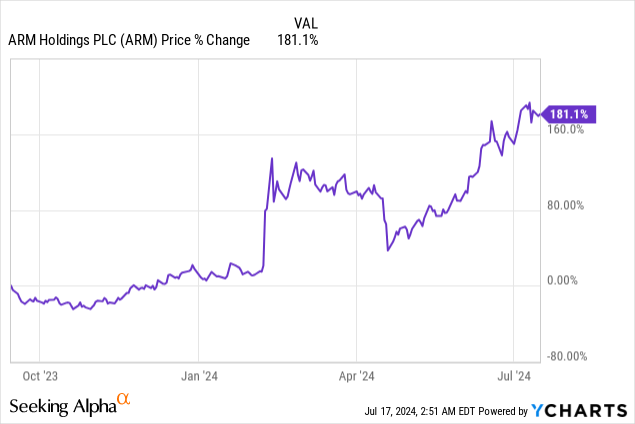

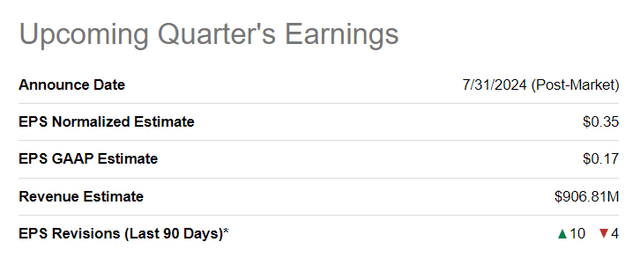

Arm Holdings (NASDAQ:ARM) was one of those investment opportunities that I blew big time, just shortly after the company conducted its IPO in the third-quarter of last year. In my initial work on the chip design company in September 2023 I stated that the lack of meaningful top line growth was a reason for me, paired with considerations about valuation, to give Arm a strong sell rating. This obviously did not age well since Arm started to benefit from considerable top line momentum, especially in the last quarter, related to the AI boom in the semiconductor industry. The Armv9 architecture has also proven to be successful (resulting in a higher share of product-specific royalty revenues). With Arm set to report earnings for its first fiscal quarter at the end of the month (July 31, 2024), I believe the chip design company has considerable surprise potential and I am up-grading my rating to hold!

Strong business momentum amid accelerating AI boom

Given the renewed momentum in Arm’s core business, driven by growing spending in the Data Center industry, the company is facing an improving top line and earnings picture.

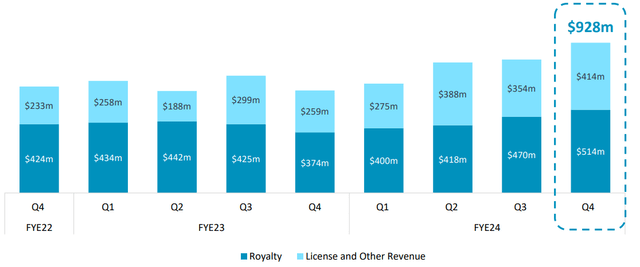

In the most recent quarter, FQ4’24, Arm reported $928M in revenue, showing a year over year growth rate of 47%. Arm achieved both its highest level of revenues ever recorded in the last quarter and saw a significant acceleration in its top line growth rate as well: in the previous quarter, Arm generated “only” 14% year over year growth.

Arm

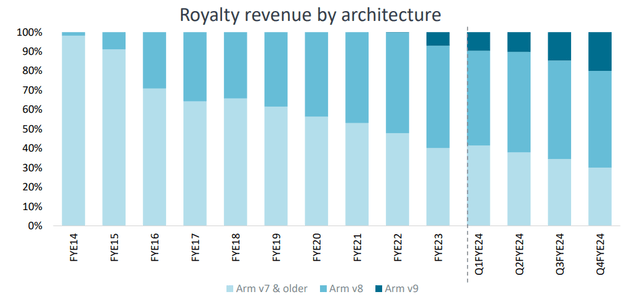

The acceleration of top line growth likely persisted in Arm’s first fiscal quarter given the strong chip demand from Data Centers especially. Arm licenses its processors and semiconductor designs to chip manufacturers and therefore participates in the overall growth of the AI, Data Center and Edge Computing industries. Arm’s revenue momentum is driven mainly by CPUs build on the relatively new Armv9 architecture that has been specifically designed to power compute-intensive AI workloads. Armv9 has started to place older-gen CPUs, like those build on the Armv8 architecture, resulting in a growing share of Armv9-related royalty revenues. With demand for AI applications growing exponentially, I would expect the chip design company to report growing Armv9-related revenues in FY 2025.

Arm

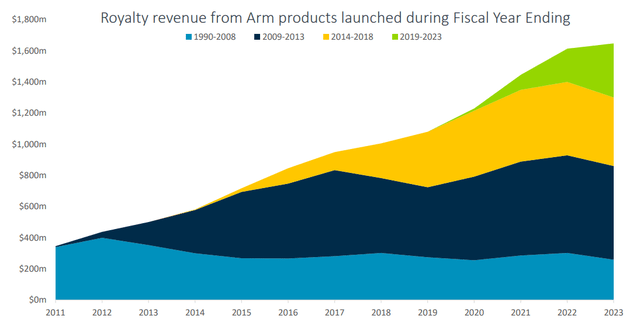

Arm’s products are vitally important for the semiconductor industry and can be found anywhere chips are used: in consumer electronics devices like smartphones, in automobiles, the Internet of Things (connected devices) and in Data Centers. Arm’s royalty revenues have grown consistently in the last decade, but the acceleration in FQ4 was a seismic shift that I unfortunately did not foresee.

Arm

A beat-and-raise is likely at the end of the month

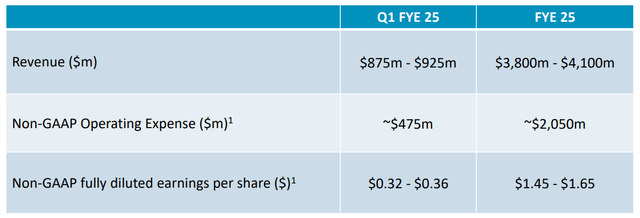

Arm guided for $3.8-4.1B in revenues for the current fiscal year. Given that Arm had revenues of $3.23B in FY 2024, the chip design company is looking to grow its top line 22% year over year.

Arm

Besides a strong guidance for revenues, Arm’s EPS revision momentum is positive as well. In the last 90 days, analysts have revised their EPS estimates upward 10 times compared to just 4 downward EPS revisions. Analysts currently expect the company to report $0.35 per-share on an adjusted basis for Q1’25 (implying a $0.01 per-share Q/Q drop-off) and I believe the current momentum in Arm’s core business, especially with regard to Armv9 product adoption raises the odds of a beat-and-raise at the end of the month.

Arm

Arm’s valuation

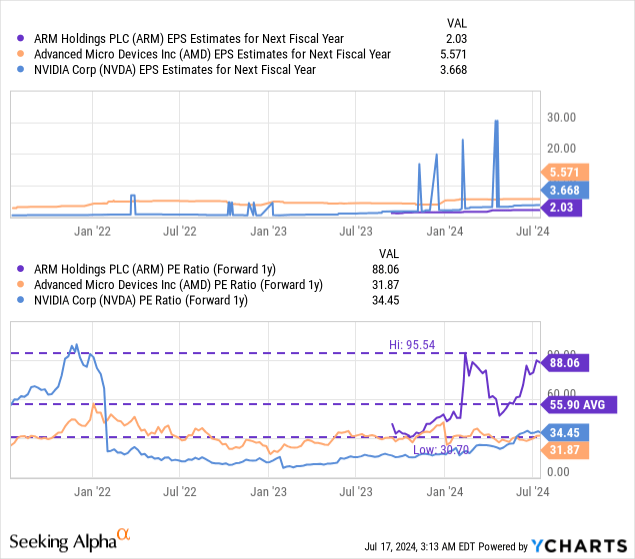

Although I clearly misjudged Arm’s possibilities for stronger top line growth, driven by new designs (such as the Armv9 architecture), the valuation is what is still holding me back from a buy rating. Shares of Arm are currently valued at a P/E ratio of 88.1X (based off of FY 2025 earnings), which is way above the company’s historical average price-to-earnings ratio of 55.9X. Even companies like Nvidia (NVDA) and AMD (AMD) are trading at much lower P/E ratios of 34.5X and 31.9X and their fortunes are obviously also closely linked to the prospects of the semiconductor industries as well.

Arm is expected to see 30% EPS growth next year compared to earnings growth rates of 34% for Nvidia and 59% for AMD. In other words, Nvidia and AMD are still going to grow more quickly than Arm, but trade at significantly lower earnings multipliers. In my opinion, AMD is an exceptionally good deal for investors right now given its accelerating GPU ramp which is set to go into full effect in FY 2025: AI GPU Underdog With Serious Catalysts.

Nvidia, obviously, is the ultimate Data Center play given its explosion of profits in the last quarter.

The industry group price-to-earnings ratio is about 51.0X which would make Arm significantly overvalued. However, as I said above, Arm does have considerable surprise potential heading into its Q1’25 earnings report given its strong royalty revenue growth related to the Armv9 architecture that has been specifically designed for the AI market. Based off of the company’s historical valuation ratio of 56X forward earnings, Arm could have a fair value closer to $118. However, the top line momentum and strong demand for AI chips could result in a significant raise in the company’s outlook for FY 2025 revenues and earnings. Given this surprise potential, I am upgrading shares of Arm to hold.

Risks with Arm

The biggest risk for Arm, as I see it, relates to a potential slowdown in the core business, driven by companies scaling back their spending on Data Center infrastructure. Companies are investing heavily into their AI capabilities, but they are currently not yet reaping the rewards from this spending. A scale-back of AI-related infrastructure spending would hit Arm hard and likely cause the multiplier factor to contract.

Final thoughts

Arm is likely set for a strong earnings scorecard for its first fiscal quarter, to be revealed on July 31, 2024, driven by strong demand for AI-optimized processors deployed in Data Centers around the world. In my opinion, Arm is set to see continual upside momentum in its top line and the company is has significant surprise potential at the end of the month. The earnings estimate revision momentum favors Arm as does the company’s growing share of Armv9-related royalty revenues. I still don’t like Arm’s valuation, however, but like to correct my misguided rating from September ahead of a likely strong Q1’25 earnings card. Since Arm’s revenue growth accelerated considerably in the last quarter, Arm has also favorable odds of raising its full-year revenue and earnings forecast!

Read the full article here

")

")