")

")

")

")

Introduction

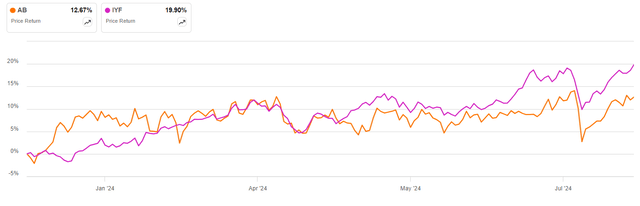

AllianceBernstein (NYSE:AB) has underperformed the iShares U.S. Financials ETF (IYF) so far in 2024, delivering a circa 13% total return against the almost 20% gain for the benchmark ETF:

AB vs IYF in 2024 (Seeking Alpha)

This has resulted in the company trading at an adjusted P/E multiple discount relative to the broader US financials sector, as well as recent M&A transactions. Also taking into account the firm’s robust operating results in terms of AUM growth and benchmark outperformance, I think the shares are worth a buy rating.

Company Overview

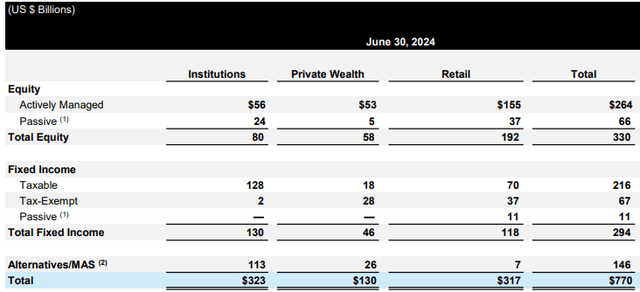

You can access all company results here. AllianceBernstein is an asset management company managing $770 billion in assets under management, or AUM, at the end of H1 2024, split between Equity (43% of AUM), Fixed Income (38%), and Alternatives (19%):

Assets under management breakdown (AllianceBernstein Q2 2024 Results Presentation)

From the snippet above, we also observe Institutional investors account for 42% of AUM, followed by Retail investors at 41% and Private Wealth customers at 17%.

73% of AUM is managed for clients in the United States, while overseas clients account for 27% of AUM.

Operational Overview

AllianceBernstein reported an adjusted EPS of $0.71/share in Q2 2024, up 16% Y/Y, driven by an improved adjusted operating margin of 30.8% (2023: 27%), helped by lower expenses even as revenues were flat Y/Y.

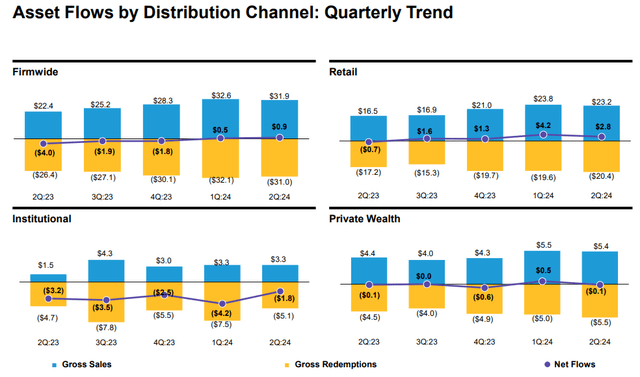

Net flows into AUM were $0.9 billion in Q2 2024, continuing an improvement since Q2 2023 when net flows were negative $4 billion:

Net Flows Evolution (AllianceBernstein Q2 2024 Results Presentation)

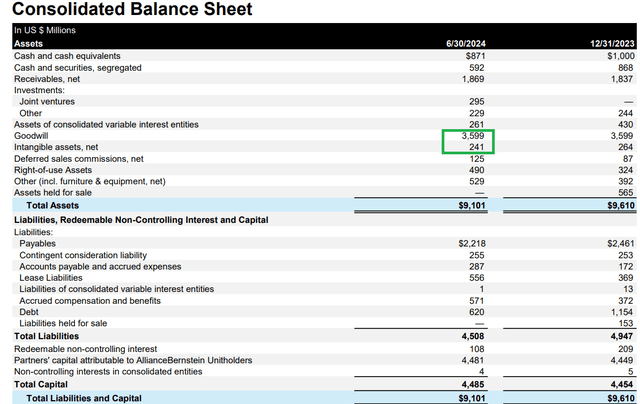

Balance Sheet

AllianceBernstein runs a conservative balance sheet with a net cash position of $251 million. As such, the company will actually be negatively affected as the Fed cuts interest rates unless it opts to repay debt and repurchase shares. Its debt currently carries an interest of 5.3%.

As you would expect from an asset management company, the balance sheet is dominated by intangibles of about $3.8 billion:

Consolidated Balance Sheet (AllianceBernstein Q2 2024 Results Presentation)

Valuation and prospects

AllianceBernstein is quite attractively valued on an adjusted P/E multiple basis, at about 12.3x. I should again underscore that the earnings are achieved with a net cash position, a rare capital structure among financial companies that generally use leverage to boost returns.

The company also trades at a discount to the iShares U.S. Financials ETF Price/Earnings multiple of 15.6x, which admittedly is a GAAP basis, hence not directly comparable with AllianceBernstein’s adjusted P/E.

I would also point you to my recent article highlighting the acquisition of French insurance company AXA (OTCQX:AXAHY)’s asset management unit, AXA IM, by BNP Paribas (OTCQX:BNPQF). The transaction was priced at an adjusted P/E multiple of 15x, indicating some upside potential should a larger company acquire AllianceBernstein.

While there is no concrete indication of such a transaction happening in the near term, I would not rule it out in the future. I think banks suffering from declines in net interest income as central banks cut rates will want to deploy excess capital into growth areas such as asset management, which are asset-light and offer upside for commission income.

We are already seeing movement in this regard, with AllianceBernstein forming a joint venture for equity research with Societe Generale (OTCPK:SCGLF).

Risks

I think the main risk facing AllianceBernstein is its high exposure to active equity, at 80% of total equity AUM. With the proliferation of passive investing, active managers such as AllianceBernstein have struggled to attract assets, as evidenced by its weak although positive AUM inflows.

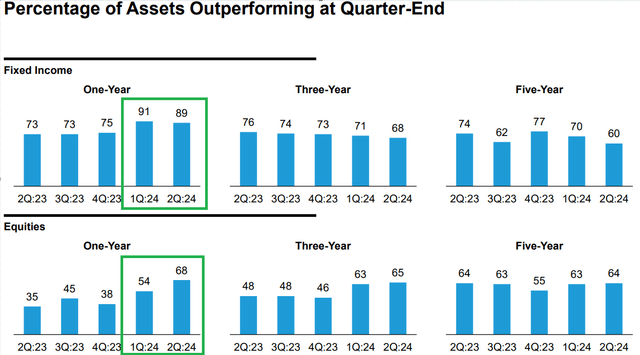

The good news here is that the company has seen a rise in Equity and Fixed Income assets outperforming their benchmarks in H1 2024, which should help attract AUM in the future:

Performance versus benchmarks (AllianceBernstein Q2 2024 Results Presentation)

Another risk to highlight is that net flows are driven entirely by Retail clients, while Institutional and Private Wealth clients withdrew AUM in Q2 2024. This exposes AllianceBernstein to heightened economic risk as I think retail investors are more likely to withdraw AUM during a recession as opposed to institutional investors.

Finally, I would note the firm may underperform due to its low financial gearing, which will hurt growth relative to peers that have funded part of their balance sheet with debt and may see their costs decline as the Fed lowers interest rates. Of course, the capital structure is always dynamic and AllianceBernstein may adjust in the future, for example via share repurchases funded with new debt.

Conclusion

AllianceBernstein delivered positive AUM net flows in Q2 2024 and is attractively valued on an adjusted P/E multiple basis. The asset manager trades at a discount relative to the U.S. financials sector and the recently announced AXA IM transaction.

The company runs a net cash balance sheet which provides safety on the one hand but will also hurt returns as peers benefit from Fed rate cuts on the other hand.

I think that the shares are worth a buy rating as long as AllianceBernstein keeps up the robust performance in terms of net flows and outperformance versus benchmarks. The firm may provide further upside if a bank looking to boost its commission income expresses interest in purchasing the asset manager – something I have no indication of at the moment.

Thank you for reading.

Read the full article here

")

")

")

")