")

")

Investment Rundown

The action with the stock price of ALLETE Inc (NYSE:ALE) hasn’t been that great for the past 12 months. I covered the stock before in late August. Since the writing of that article, the stock has appreciated about 6% in total, which has been an underperformance of the broader markets, like the S&P 500, which has grown over 10% during the same period. ALE continues to trade at quite low multiples making it still an appealing buy for the long-term investor. The company is not that far out from its Q4 and full-year 2023 report, but the company has already raised its quarterly dividend to $0.705, a 4.1% raise YoY. The yield is now very appealing for the long-term with 4.77%. I am making an additional article on the stock to give an updated view for 2024, but to keep it short, I continue to be bullish on the business and the valuation leaves a good upside potential for investors.

Company Segments

ALE operates as an energy company, working with electricity generation through sources like coal, natural gas, hydroelectric, wind, and solar. The company has started focusing on clean and renewable energy projects in the last several years, managing a significant wind energy generation capacity. ALE has now become a leading investor in renewable energy in comparison to its market cap.

Company Overview (Investor Presentation)

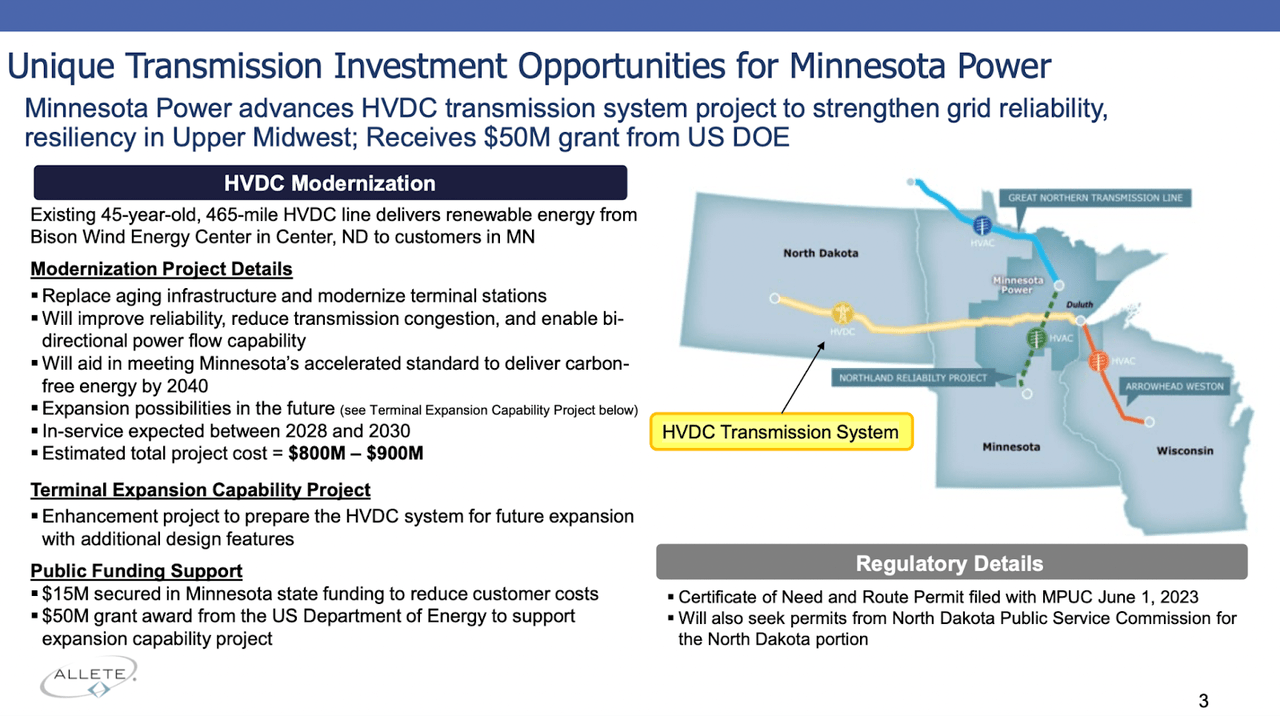

ALE has identified several investment opportunities to find new revenue sources, and at the same time create a qualitative asset base for the long-term. One of the areas that I watching right now is Minnesota Power as ALE aims to expand more into North Dakota and create a bigger transmission line. In late 2023 ALE and North Plains Connector LLC signed the agreement for a new HVDC line in North Dakota. The 400-mile high voltage line is set to be established from North Dakota to Colstrip Montana. The agreement represents a nearly $3.2 billion investment into infrastructure and energy for Montana and North Dakota. This should in my opinion position ALE very well over the next decade to continue steadily increasing its revenues as base retail electric rates increase.

Company Growth (Investor Presentation)

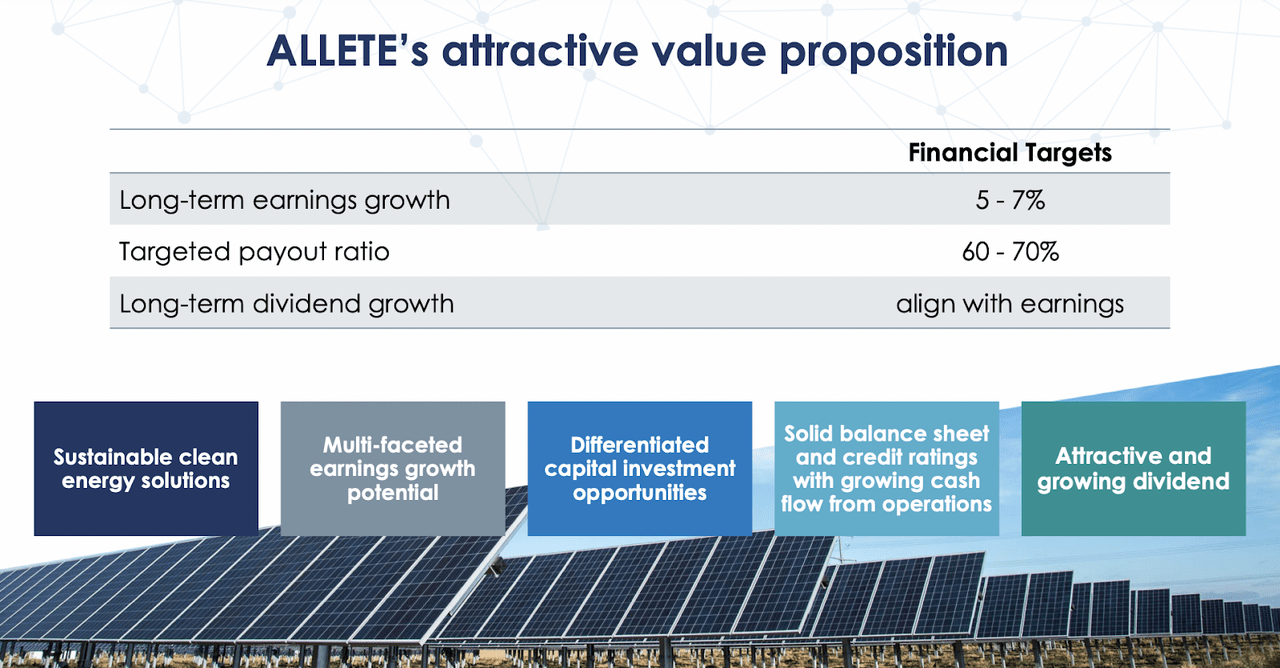

ALE has a few different segments, those being Regulated Operations, ALLETE Clean Energy and Corporate, and lastly Other segment. ALE’s Regulated Operations segment has built up a strong position in northwestern Wisconsin, where it provides essential utility services. The company has around 15,000 electric, 13,000 natural gas, and 10,000 water customers in the region, securing a strong position in the regional market. ALE has made it clear for the long term that they intend to deliver a very solid shareholder return. A target payout ratio of 60 – 70% is quite high but lends itself well to continued dividend raises. The long-term dividend raises are expected to go in line with long-term EPS growth of 5 – 7%.

Dividend Summary (Seeking Alpha)

ALE raised the dividend in late January and set it at a quarterly $0.705, a 4.1% raise from the previous one. This is of course lower than the long-term one, so I do expect it to accelerate from here, and the North Dakota investments is certainly going to be one of these carriers. The payout ratio can also be increased further as it is at the lower end of the guided range, at 62%. The yield is 4.77% is close to the ATH high yield of 5.3% for the company. As we approach the next earnings report I think that some more comments on strategic expansion will be good to get, to better gauge on how ALE could ensure they deliver on the long-term targets. A more aggressive dividend raise in 2024 is on my checklist along with a bigger cash buildup to hedge against potentially high interest rates to continue.

Earnings Highlights

We are approaching the next earnings report by ALE, which seems to be on February 16. I have been bullish on the stock before as I see it as undervalued, and below we will dive a little into the target price and fair value I see for it. But first I want to recap the third quarter a little and see if we can spot some trends that might continue in Q4 that could either be bullish or bearish.

Income Statement (Earnings Report)

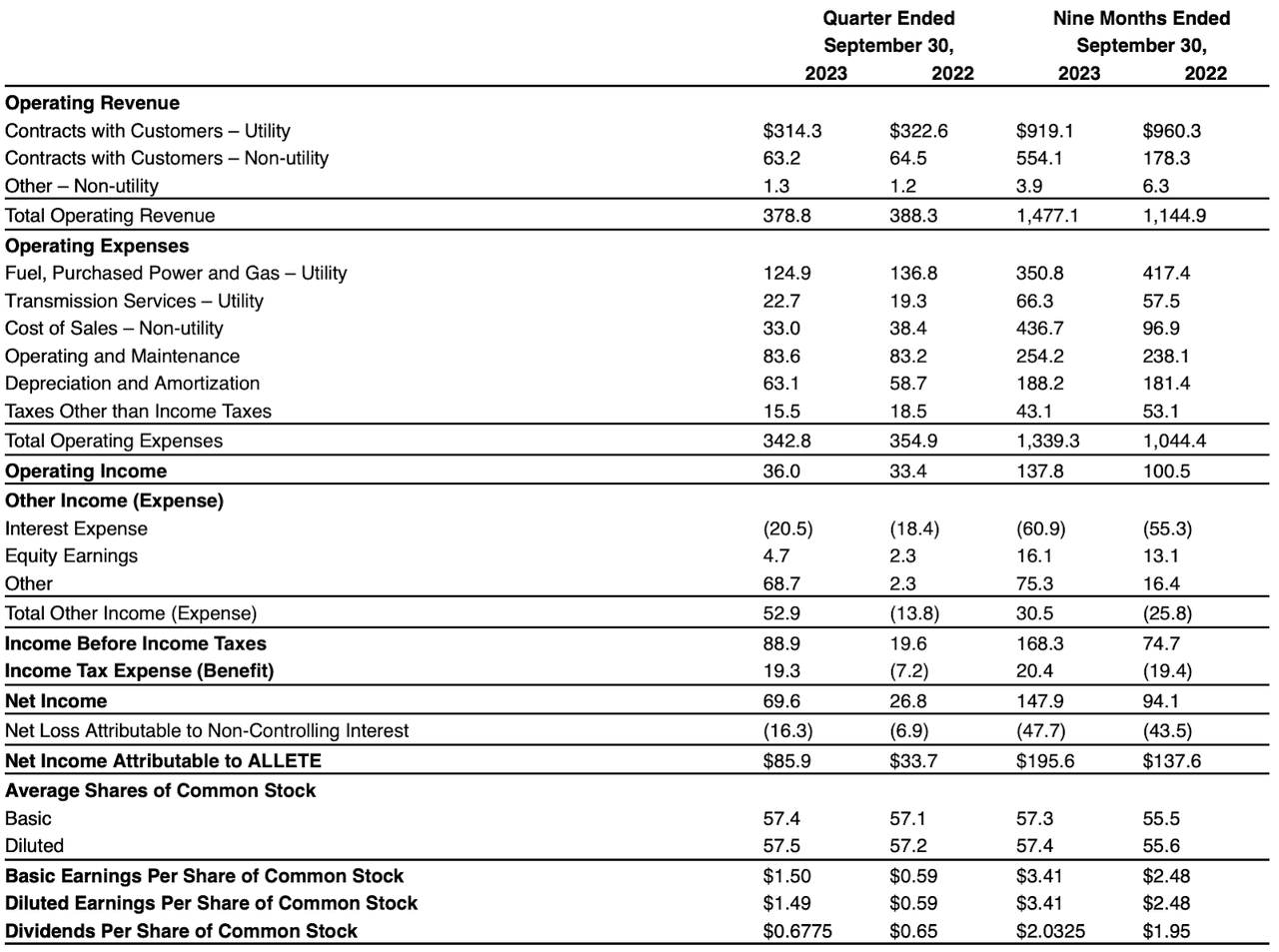

The third quarter report was released on November 2 and included a raise for the full-year guidance, EPS is now expected to be $4.3 – $4.4. I like this outlook and guidance as it’s very tight and showcases how ALE can reliably predict their future earnings and act according to it as we do. Makes it a lot easier for an analyst as well to better gauge the value of the business. One of the trends that appeared in the report was a slight revenue loss of $10 million YoY, mostly because of a loss in contracts with customers’ revenues. However, the bottom line was still up a lot YoY, $1.50 compared to $0.59 in Q3 FY2022. On the operating expense, the fuel, purchase of power, and gas fell by $12 million and tax expenses also fell, resulting in a net income of $69.6 million. A larger part was also other income, amounting to $68.7 million. The other income was related to an arbitration reward.

Valuation (Seeking Alpha)

The FY2023 EPS estimate of $4.3 – $4.4 now puts ALE at an FWD p/e of 13.4 on the higher end of the guidance. ALE has for the better part been able to beat out on earnings estimates, but not by a lot, so I don’t expect there to be one here either. With an FWD p/e of 13.3 ALE trades nearly 20% below the rest of the utilities sector. I think in the past 12 months there has been a shift out of utility companies and energy companies too as investors are eying future rate cuts and want to be in more high-growth stocks instead. This has left an opening for a company like ALE. I think a fair value is a p/e of 16, and I say this because of the reliable outlook and performance it has had so far. It can efficiently row the EPS and at the same time distribute a satisfactory dividend yield too. With a 16x earnings multiple I arrive at a target price of $70 for FY2024 with ALE, representing a solid upside potential which is why I am reiterating my buy for the stock once again.

Risks

Earnings volatility is one of the concerns that I see with ALE right now. In 2020 the company got a credit downgrade following somewhat lacking earnings growth. The reason cited was weaker economic conditions which caused ALE to look more leveraged. The downgrade wasn’t necessarily that drastic but the downgrade was issued amid the Covid-19 outbreak, which further dragged down the stock price. The stock has not received to pre-pandemic levels of $86 per share, and perhaps the higher debt position ALE has acquired has something to do with this. However, the past few years have meant strong earnings growth, averaging over 11% annually over the past 3 years. EBITDA at $430 million and long-term debt at $1.6 billion leaves a ratio of 4, which isn’t necessarily worrisome high, not for a utility company like ALE at least. The company works in an incredibly stable market where rates are set for a long period and earnings are easier to anticipate. The risk that was previously placed over ALE I don’t think no longer holds enough weight to trump a buy case.

Final Words

It’s my second time covering ALE here on Seeking Alpha and I will be sticking with my initial rating, which is a buy. The company has continued to expand its asset base and the large investments going into North Dakota to establish an HCDC transmission system are positioning it well for the long-term. Shareholder returns are continuing to be a high priority, with the payout ratio remaining between 60 – 70%. I expect further divined raises in 2024 and with earnings around the corner, it continues to radiate value for the long-term investors.

Read the full article here

")

")

")

")

")