")

")

")

On August 8th, Aldeyra Therapeutics, Inc. (NASDAQ:ALDX) seemingly achieved its final clinical step in its long and winding road to achieve FDA approval for its Dry Eye Disease (DED) eye drop, called Reproxalap. Approval, if granted, should trigger the exercise of an exclusive option owned by AbbVie Inc. (ABBV) that would result in significant milestone payments and the creation of a 60%/40% partnership (with Aldeyra being the minority owner) to manufacture, market and distribute this innovative DED therapy that has a significant advantage over existing DED therapies.

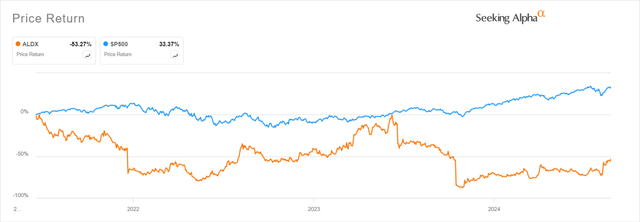

Consider this article an update to my original 2021 article on Aldeyra that provided a detailed description of Aldeyra’s intriguing RASP (Reactive Aldehyde Species) platform. I highly recommend readers review that article for a better understanding on RASP. For the sake of full disclosure, ALDX shares have substantially underperformed the overall market since that initial article was published as shown in the chart below.

Seeking Alpha

However, going forward and within the next 7 months, Aldeyra may finally deliver on the potential of its unique RASP platform that has shown promise in regulating inflammation in a safe and effective manner in several clinical studies.

Looking Back: From Unbridled Optimism to the Depths of Despair

On October 16th, 2023, with the Aldeyra investing community in a very positive frame of mind, given the great optimism emanating from management over the prior year, the company dropped this bombshell in an 8-K filing:

Item 8.01 Other Events

On October 16, 2023, Aldeyra Therapeutics, Inc. (“Aldeyra” or the “Company”) announced that it received minutes from a late-cycle review meeting (the “Minutes”) with the U.S. Food and Drug Administration (the “FDA”) relating to the new drug application (“NDA”) for reproxalap for the treatment of the signs and symptoms of dry eye disease. The Minutes identified substantive review issues in connection with the NDA for reproxalap. The FDA stated that “[i]t does not appear that you have data to support the clinical relevance of the ocular signs to support your dry eye indication.” In subsequent communications between Aldeyra and the FDA, Aldeyra has submitted responses to the FDA that Aldeyra believes to be sufficient to mitigate the identified issues, but the FDA has not directly opined on the sufficiency of the information submitted, has no legal obligation to review the information submitted by Aldeyra, and has indicated that Aldeyra needs to conduct an additional clinical trial to satisfy efficacy requirements. As such, based on the time remaining in the NDA review cycle, the FDA may not be in the position to approve the NDA for reproxalap on or about the Prescription Drug User Fee Act (“PDUFA”) target action date of November 23, 2023 or afterwards, and it may issue a Complete Response Letter and require that Aldeyra conduct additional clinical trials and submit the results of those clinical trials before the application will be reconsidered.

ALDX shares that had traded above $11 per share in June 2023, plummeted to a low of $1.42 on the devastating disappointment. A month and a half later, on November 27th, the company made the bad news official when it revealed it had, in fact, received the dreaded, “Complete Response Letter” from the FDA and an additional clinical trial would be required to gain approval.

Bad News Reversal: AbbVie Shows Its Interest in Reproxalap

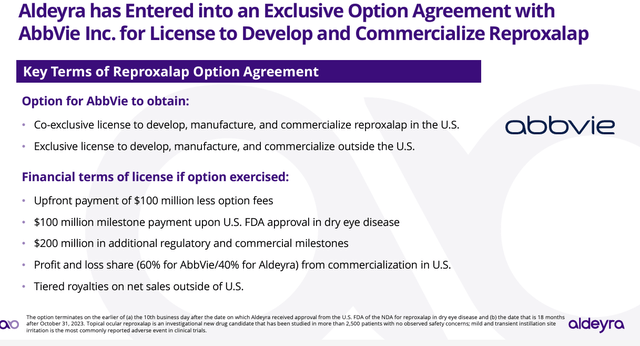

On November 1st, 2023, after the 8-K warning and with the official failure announcement from FDA still imminent, Aldeyra mitigated the bad news somewhat when it announced an option agreement on a potential joint venture with AbbVie:

LEXINGTON, Mass.–(BUSINESS WIRE)–Nov. 1, 2023– Aldeyra Therapeutics, Inc. (ALDX) (Aldeyra), a biotechnology company devoted to discovering and developing innovative therapies designed to treat immune-mediated diseases, today announced that it has entered into an exclusive option agreement with AbbVie Inc. (AbbVie).

Under the terms of the option agreement, AbbVie has the option to acquire a co-exclusive license to develop, manufacture, and commercialize reproxalap in the U.S. and an exclusive license to develop, manufacture, and commercialize reproxalap outside the U.S. Aldeyra will receive a non-refundable option fee of $1 million and an upfront payment of $100 million less option fees if AbbVie chooses to exercise the option. Under the terms of the license agreement, Aldeyra would be eligible to receive up to $300 million in regulatory and commercial milestone payments, inclusive of a $100 million milestone payment upon U.S. Food and Drug Administration approval of reproxalap in dry eye disease; in the United States, Aldeyra and AbbVie would share profits and losses from the commercialization of reproxalap according to a split of 60% for AbbVie and 40% for Aldeyra; and for markets outside the U.S., Aldeyra would be eligible to receive tiered royalties on net sales of reproxalap.

Exercise of the option will also grant AbbVie the right of first negotiation for compounds that are owned or otherwise controlled by Aldeyra in the field of ophthalmology relating to treating conditions of the ocular surface. The right of first negotiation is in addition to a right to review data for any other compounds that are owned or otherwise controlled by Aldeyra in the fields of ophthalmology and immunology before such data is shared with any other third party..

By itself, a $1,000,000 up front payment, with no firm obligation, is not very impressive. However, AbbVie is one of the largest pharmaceutical companies in the world and a very impressive partner for a tiny company like Aldeyra to corral given the pending NDA failure. Importantly, through its acquisition of Allergen in 2020, AbbVie became the owner of Restasis, the most successful DED prescription eye drop ever. From AbbVie’s perspective, with Restasis now off patent and the first competing generic approved in February 2022, Restasis revenues have plummeted and Reproxalap gives AbbVie a potential new differentiated DED therapy to get back in the game.

From Aldeyra’s perspective, this seems like the ideal partner. Much of the team that developed Restasis into a blockbuster drug should still in place to take on the Reproxalap mission. AbbVie is well suited to help guide Aldeyra through the approval process and, more importantly, if and when the option is exercised, AbbVie has extensive experience to build out a DED business.

The Latest Data and Why This Time Reproxalap Should Gain Approval

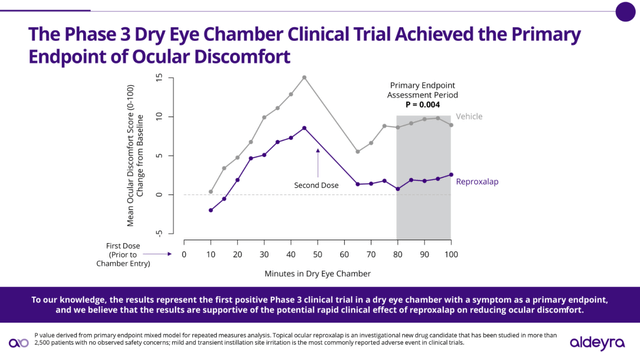

So why should investors be optimistic this time? First of all, Aldeyra has been in direct discussions with the FDA with regard to the protocol and additional clinical endpoint needed to gain approval. Aldeyra designed the latest symptom trial using the endpoint of ocular discomfort, specifically based on those discussions, which included a Type A meeting. The study, undertaken in a dry eye chamber, delivered a highly statistically significant effect over vehicle based on a p value of .004:

Aldeyra Therapeutics

So, to recap, according to the FDA, Aldeyra failed in its first NDA attempt for Reproxalap by not providing the breadth of data required for approval. Aldeyra then worked closely with the FDA to design the protocol of a final study that, if successful, would satisfy the FDA’s requirements for approval. The study results were compelling, with an excellent demonstration of efficacy and without any material adverse effects. Shares have rallied from the low $3 range to over $5.00 based on these results. However, the company still seems to be facing a lingering credibility problem and, as a result, shares are still well below all-time highs even as they approach an important inflection point. It appears that Aldeyra shares are still in the, “Fool me once, shame on you. Fool me twice, shame on me!” penalty box. They can exit the box with FDA approval or an option exercise by AbbVie, whichever comes first.

Reproxalap’s Ace in the Hole – Immediate Relief

The DED space is a very competitive space. From over the counter eye drops to prescription drugs, a patient has many options. However, when a patient takes the step to see an ophthalmologist for relief, Reproxalap (based on data) should have one significant marketing advantage over other leading prescription drugs like Xiidra, Restasis and generic forms of Restasis. Reproxalap provides BOTH acute and chronic relief to dry eye patients. Existing competing DED therapies take weeks or longer to show any effect. Reproxalap works within minutes. This advantage cannot be overstated. It would be a logical assumption that, with all other considerations being equal, an ophthalmologist treating a patient with dry eye disease would be inclined to prescribe a therapy that provides the patient with BOTH immediate and long-term relief.

Financial Position and Valuation

Within about a month, Aldeyra is expected to file a new NDA for Reproxalap with the FDA. The main risk here is obvious; another rejection by the FDA would be devastating. Based upon everything previously stated in this article, that outcome seems highly unlikely, but it can never be completely discounted.

At a price of $5.30, Aldeyra has a market cap of about $319,000,000. At the end of June 2024, Aldeyra had $120,000,000 in cash, cash equivalents and marketable securities and $15,000,000 in debt, giving it an enterprise value of about $214,000,000 ($319M – $120M + $15M). Within the next 7 months or so, investors will have the answers with regard to Reproxalap and AbbVie. $400 million in total milestone and upfront payments are at stake, in addition to royalties and a 40% ownership of the joint venture, as shown in the summary below.

Aldeyra Therapeutics

A quick and dirty calculation based on the terms of the AbbVie transaction indicates that shares are undervalued under my assumption that there is a high likelihood of FDA approval and the consummation of the AbbVie transaction.

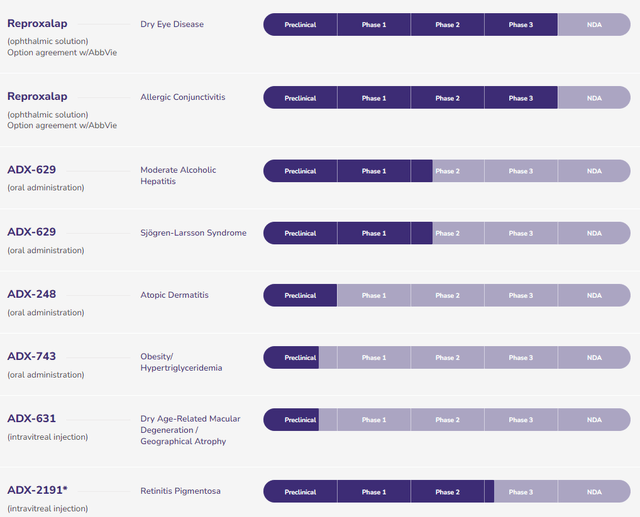

Focusing only on the milestone payments and the value of the joint venture provides a ballpark valuation of this transaction. Assuming milestones are met, AbbVie will pay Aldeyra a total of $394,000,000 ($6,000,000 has already been paid with option exercise and extension). One simple step to analyze the implications of the value being created is to assume that $400,000,000 is representative of AbbVie’s 60% investment in the AbbVie/Aldeyra joint venture for Reproxalap. This implies that AbbVie, at a minimum, is valuing the joint venture at $666,666,666 ($400,000,000/60%). This would also imply that Adeyra’s 40% interest of the $666,666,666 is worth $266,666,666. Adding the $266,666,666 to the $394,000,000 in potential remaining cash payments from this deal, at a minimum, Aldeyra will generate $660,666,666 in value from the future execution of this transaction over time. For simplicity, the discounted time value of money and future value of royalties and future profits from the venture are ignored. The $660,666,666 in value created is over 3 times the current enterprise value of Aldeyra and that does place a value on the rest of the RASP and non-RASP pipeline as shown below:

Aldeyra Therapeutics Pipeline (Aldeyra Therapeutics)

With a win on Reproxalap, the rest of the RASP pipeline should come into focus and there is the possibility that AbbVie would be interested in purchasing the remaining 40% interest held by Aldeyra in the Reproxalap venture or buy the company outright in my view.

Risks and Cash Runway

By now, readers probably have surely identified the most significant risk to this story. That, of course, is that the FDA finds a reason to turn down the NDA for Reproxalap, once again. For sure, that is the number one risk here and the risk one must accept, based on the analysis shared above, in order to buy into this investment thesis. The other related risk is the basic risk of investing in small biotechs, in general. Many more fail than succeed. As stated above, Aldeyra has a healthy cash position of $120,000,000. At the end of a recent investor call, CEO Todd Brady stated that the current trials in the pipeline above are fully funded. In Aldeyra’s most recent 10-Q, operating cash burn through the first half of 2024 was $23,196,000 or $3,866,666, monthly. At that burn rate, the company has about 31 months of cash assuming a $15,200,000 debt obligation due on October 31, 2024, to Hercules Capital Inc. gets extended. In the event that the loan is paid off in October, the cash runway drops to about 27 months.

Read the full article here

")

")

")