")

Q4 2024 Earnings Call Transcript")

")

")

")

As the S&P500 is at its all-time high, I’ve started to look at commodity stocks that are at depressed price levels. Enter: Albemarle Corporation (NYSE:ALB). This leading American lithium mining company has been pummeled in the past year as lithium prices have fallen mostly due to subdued EV battery demand in a harsh macro environment. The slowdown in demand has sparked fears about a wider gap between supply and demand as the mining companies continue to increase production to meet the increasing secular demand.

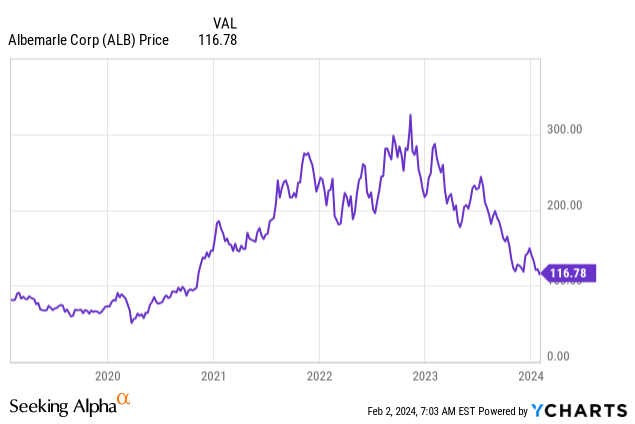

In August of 2022, Albemarle’s stock reached an all-time high at $325 but has now dropped to only $116. A word of caution: Commodity markets are highly volatile and investing in them requires a stomach for fluctuations. However, the volatility can also offer great returns if executed properly. The majority of Albemarle’s business is from lithium, and the stock price is highly correlated with lithium prices, so that will be the main point of this article. I issue a Hold rating for this company. If the stock were to drop another 30% or more, or the supply & demand picture turns into a more favorable one, prospective investors should be facing a compelling risk/reward situation.

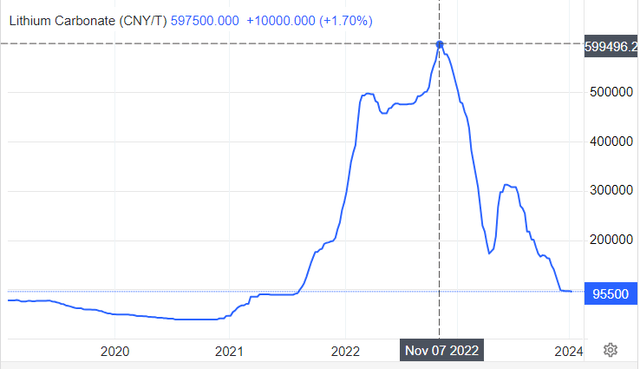

CNY/T Price History (TradingEconomics)

Company Overview

Albemarle Corporation is a global specialty chemicals company that produces and sells a wide range of essential ingredients for a variety of industries. The company operates in three business segments: Energy Storage(Lithium), Specialties(Lithium, Bromine), and Catalysts(Ketjen).

Revenue Streams

Albemarle generates its primary revenue stream from the sale of its products to customers. The company’s products are used in a variety of applications, including:

- Lithium-ion batteries for electric vehicles and grid energy storage

- Bromine-based products for fire safety, water treatment, and refrigerants

- Catalysts for oil refining, petrochemical processing, and industrial emissions control

In addition to selling its products directly to customers, Albemarle also offers contract manufacturing services to companies that require specialized chemistry or manufacturing processes for their products.

Cost Structure

Albemarle’s cost structure is primarily driven by research and development, manufacturing, and sales and marketing expenses. The company incurs significant costs in developing new technologies and processes, as well as in constructing and maintaining its manufacturing facilities. Sales and marketing expenses are also important, as Albemarle needs to reach a wide range of customers in a variety of industries.

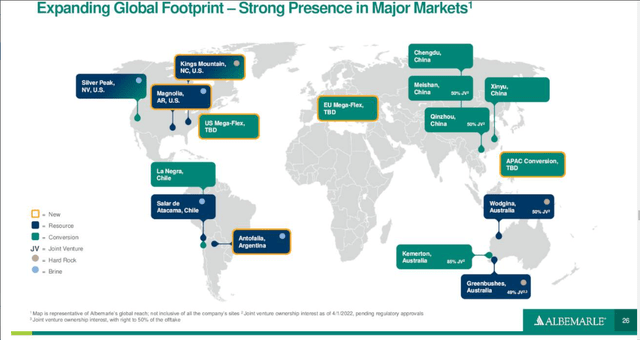

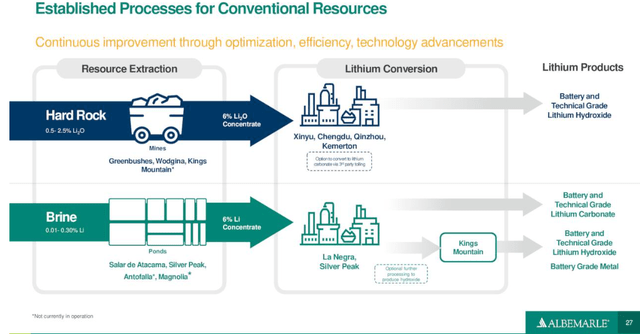

The material below illustrates Albemarle’s operations globally and gives a rudimentary grasp of its lithium operations.

Albemarle Albemarle

Financials

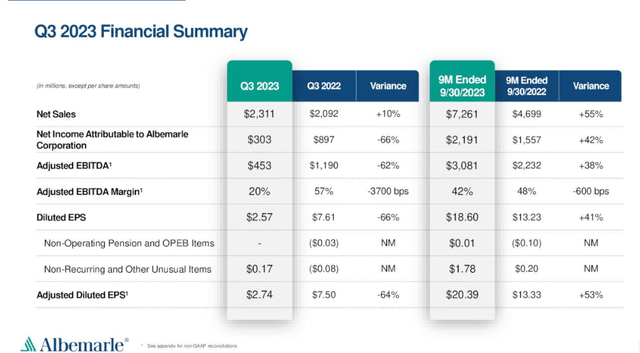

If you look at Q3 of 2023 compared to the same quarter of 2022, you’d think the company is in serious pain; this isn’t the case.

Albemarle

In Q3 of 2023, Albemarle’s Net Income and Diluted EPS collapsed -66%. Adjusted EBITDA also fell -62%, and margins along with it from 57% to 20%. Bearish points include Albemarle’s profitability in a low lithium price environment. These aspects paint a bleak picture, and these numbers are mainly due to the falling lithium prices. But as I said, this isn’t the full story. For one, the lithium prices in the past few years have been extraordinary and do not reflect the average prices in the market. A fall might seem drastic, but it isn’t apocalyptic. In contrast, 9M ended 9/30/22 Diluted EPS and Adjusted EBITDA were up 41% and 38%, respectively. The danger here is that management becomes overly optimistic, assuming that high lithium prices will return in no time, making excessive projections about their business.

Going back to the Q3 comparison, Net Sales were 10% higher, indicating a persistent demand for Albemarle’s business even in a tough macro environment. Albemarle’s cost structure for lithium production is of the industry’s highest standard, allowing them to produce lithium despite the low prices. This leads to gaining market share from competitors that are required to reduce or halt production due to their higher cost structure, giving Albemarle an enviable position in the lithium industry to keep chugging to gain more business. As the prices rise sooner or later, they will have more customers and sales. This doesn’t mean it’s a go for investors. As the low-cost producers keep chugging, supply increases and lowers the price of lithium until demand picks up or supply decreases relative to demand. Only when even the most cost-efficient producers start to halt projects do we see a bottom in prices. In this scenario, it would be the go for investors.

In Q3 Earnings Call, CFO Scott Tozier gave an outlook guidance for the full-year:

Our adjusted EBITDA outlook is expected to be in the range of $3.2 billion to $3.4 billion. This implies full-year EBITDA margins of 34% to 35%. Our full year 2023 adjusted EPS outlook has also been adjusted to a range of $21.50 to $23.50.

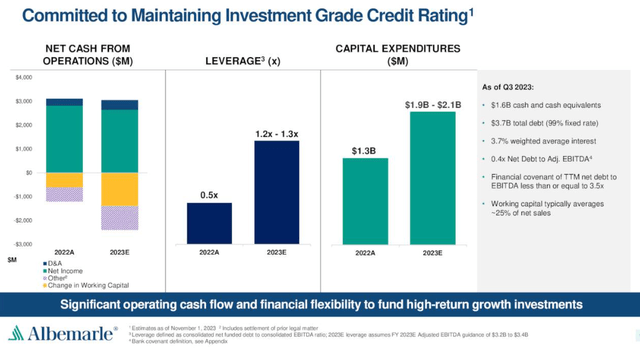

Looking at Albemarle’s balance sheet, the company seems to be operating in a fairly conservative manner. The company operates with a leverage of 1.2x to 1.3x, within acceptable levels. With mostly all of its debt being fixed rate, current leverage isn’t an issue. However, $3.7B in debt against negative levered free cash flow at -1.25B (‘TTM’) is a considerable amount, and this issue should be a point of interest while evaluating the company and its following quarterly reports. Less investment and higher lithium prices would help with the debt burden, but one should expect low prices for multiple years.

Management indicated in their Q3 Earnings Call that they intend to be conservative in their capital allocation to sustain their BBB credit rating and be financially nimble while investing in organic and inorganic growth. However, raising capital expenditures while profits are taking a beating isn’t a particularly welcome sight. After ensuring conservative capital allocation and growth, next up is maintaining dividend payments and growing them, as ALB has hiked them annually for 28 years. However, the yield isn’t that appealing with 1.40%.

Albemarle Albemarle

Growth

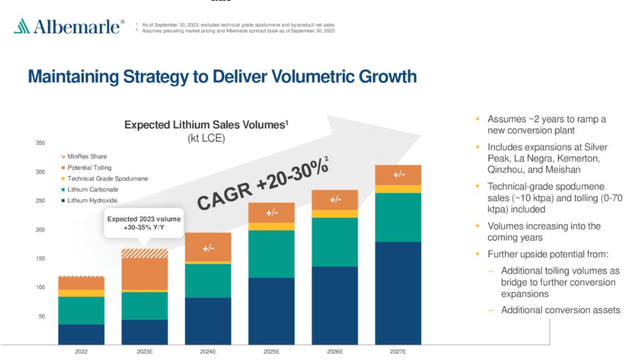

Albemarle expects to deliver volumetric growth of 20-30% CAGR until 2027. They expect the full-year of 2023 to be 30-35% growth, and after the fiscal year of 2024, the LCE(lithium carbonate equivalent) kiloton volume should be close to 200. This rapid growth is attributable to a ramp-up in different projects to meet future demand and capture market share.

Albemarle

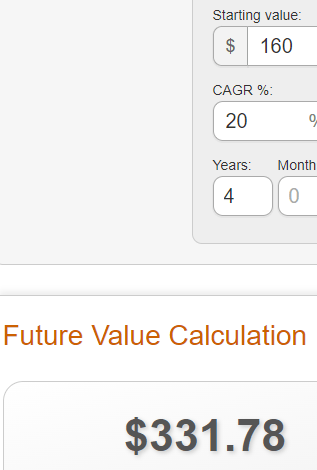

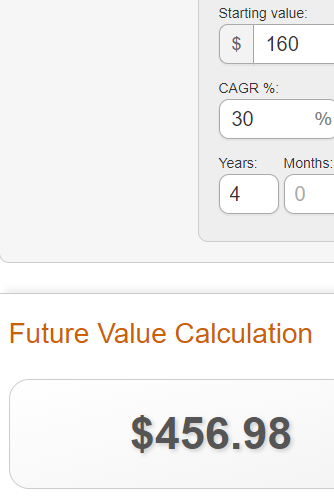

Despite the growth, the CAGR estimation raises eyebrows for me, as the difference between CAGR of 30% is considerably more than 20%. Would their estimations be revised if the growth for 2024 is 20% or a couple of basis points lower? I think so, as the 2023 growth is expected to be 30-35%. This illustrates the company’s inability to forecast with precision, leading to revised expectations and missed estimates. As a prospective shareholder, this wouldn’t be ideal. The 2023 lithium sale volume expectations are at around 160 kilotons. I will illustrate the difference between CAGR of 20% and 30%.

20% CAGR (The Calculator Site) 30% CAGR (The Calculator Site)

As can be seen, the sales volume projections with their CAGR estimations are on an entirely different page. A CAGR of 30% estimation in four years is approximately 38% higher than the 20% CAGR estimation. While the growth numbers are significant either way, my trust in the company’s estimates wavers.

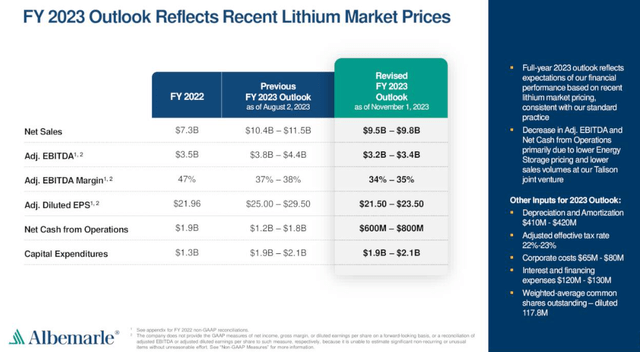

In addition to sales volume estimates, Albemarle had to revise their net sales estimates for 2023 in their Q3 report. In Q2, the company had estimated that their net sales for the year would be $10.4B – $11.5B. However, three months later in Q3, the estimates were at $9.5B – $9.8B. The high-end estimates fell by $1.7B in just three months, reinforcing my belief that the company’s estimates could be way off and untrustworthy. As seen from the illustration below, the net sales will still increase lavishly, fueled by increasing demand, but the estimations were off. It begs the question whether we should trust any of the estimations by the company.

Albemarle

Competition

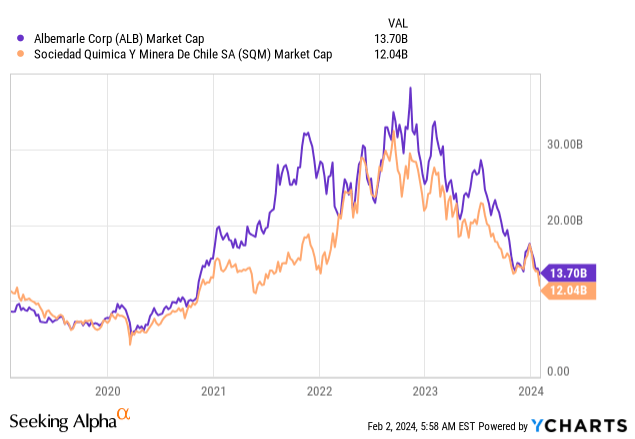

There are multiple miners in the industry, but I will compare the two of the largest: Albemarle and Sociedad Química y Minera (SQM). Other notable companies are recently merged Allkem and Livent named Arcadium Lithium PLC (ALTM), Ganfeng Lithium Group (OTCPK:GNENF), Pilbara Minerals Limited (OTCPK:PILBF), and Mineral Resources Limited (OTCPK:MALRY), among others.

As stated previously, producer stock prices primarily follow lithium prices and supply/demand equilibrium, which is evident in the YChart above. Now, the economics of these companies do differ, and we are going to compare these two.

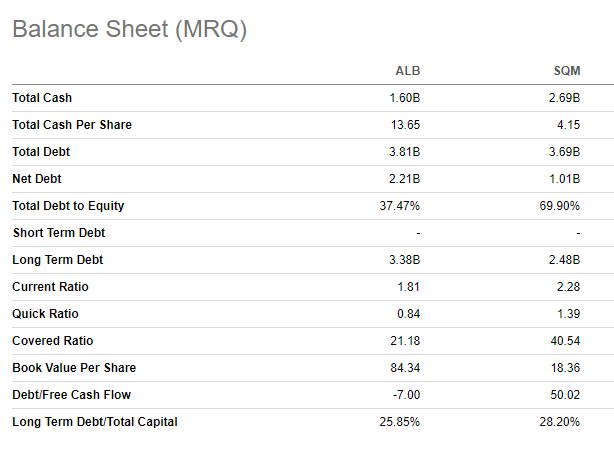

The balance sheets below illustrate that SQM has a better situation than ALB. For example, SQM has a better Current Ratio, which indicates the company’s ability to pay short-term obligations or those due within one year. A good ratio is considered to be between 1.2 and 2. Both companies have good current ratios, but SQM triumphs with a 2.28 against Albemarle’s 1.81. However, Quick Ratio excludes inventory and accounts receivable, and by using this metric, ALB seems less appealing with 0.84, as anything above 1 is considered good.

Seeking Alpha

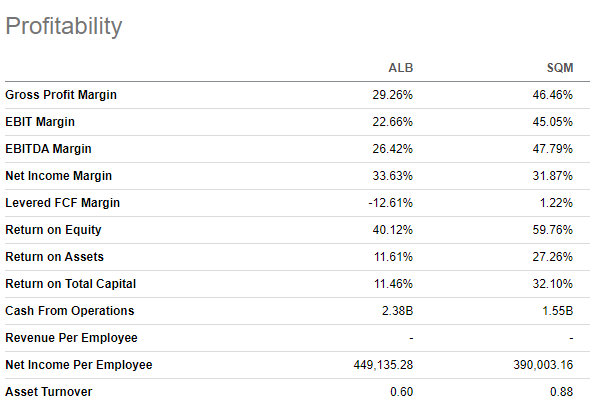

Next up is profitability. SQM beats ALB in this aspect as well in most metrics, including EBITDA Margins and RoE by 20%. But like the most metrics in this business, these are tied to highly volatile lithium prices. Furthermore, an aspect like a potential tax hike should also be considered with these two, as both have operations in Chile. More on Chile-related taxes later. As EBITDA doesn’t cover taxes, Net Income Margin is also worth looking at. Here the difference is almost non-existent, but ALB beats SQM with 33.63% against 31.87%. This is the only margin metric in the profitability section of Seeking Alpha’s comparison table that ALB is victorious in.

Right now, the profitability still has some uplift from high prices, but this year numbers will reflect what it’s like to operate in a price-deflated market. Why does SQM have better profitability numbers overall? One thing is the cost curve, as SQM mainly uses brine extraction, which is faster and cheaper than the hard rock mining method that Albemarle uses in the US and Australia sites. Second, Chile’s production costs are lower than other countries, giving SQM an advantage.

Seeking Alpha

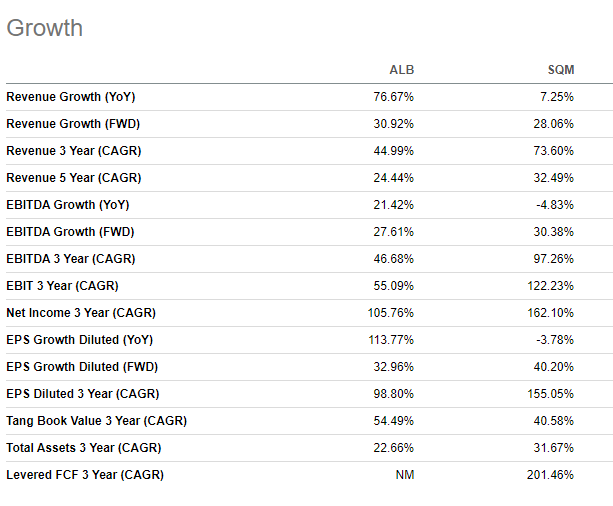

The last comparison is growth. This can be misleading akin to the profitability segment, as growth for the past years has been extraordinary for lithium and is not likely to resume, in my opinion. Forward estimates indicate that these two are likely to grow their revenues at a related pace, ALB at 30.92% and SQM at 28.06%. A similar trend is also visible with EBITDA growth (‘FWD’).

Seeking Alpha

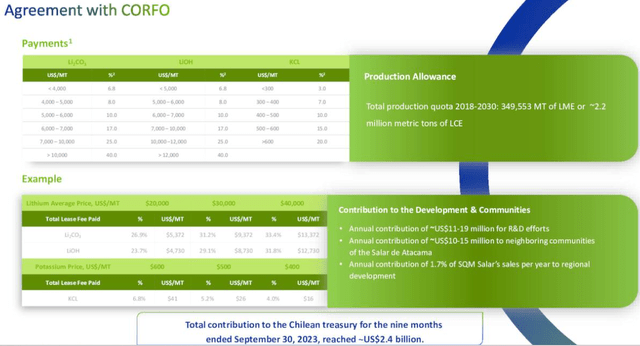

All in all, SQM seems to be the one with better numbers. However, it doesn’t make it a better investment, in my opinion. As I mentioned earlier, SQM is a Chilean company subject to various political changes and uncertainties. While some fears were subdued with a new contract to Salar de Atacama mines until 2060, politics still play a significant variable with this company. Salar de Atacama is a significant asset in both SQM’s and ALB’s arsenal, as it possesses one of the highest concentrations of lithium globally. The issue isn’t with accessing the mines and extracting lithium, but with nationalization fears and heavy taxes in company operations. For SQM, the new higher taxes are progressive, meaning the more they make, the higher percentage they will be taxed. In addition, there’s a 35% dividend tax. The picture below is from SQM’s Q3 Earnings Presentation, illustrating the progressive taxes with examples.

SQM

Codelco, a state-owned copper mining company, will own 51% of SQM’s growth starting from 2030. This was necessary evil for SQM to gain access to the Salar de Atacama for the next three decades, but not something you like to see as an investor. The following quote is from an Energy Connect article regarding the deal:

Through 2030, SQM will retain control over operations with equal board representation, although Codelco will have some veto rights. Then from 2031 through 2060, the operation would switch to a new mining lease to be signed by Codelco, with the state copper behemoth getting both boardroom and operational control, although SQM will have some veto rights.

When there’s government involvement, it’s highly incendiary for the company and investors. Imagine the company redoing its leadership after every election with members with different political views and plans driven by ulterior motives that aren’t for the company or shareholders. While SQM operations are good, combining the lithium volatility and uncertainty with this issue is a pass for me. In my view, ALB is much more stable and diversified globally.

Valuation

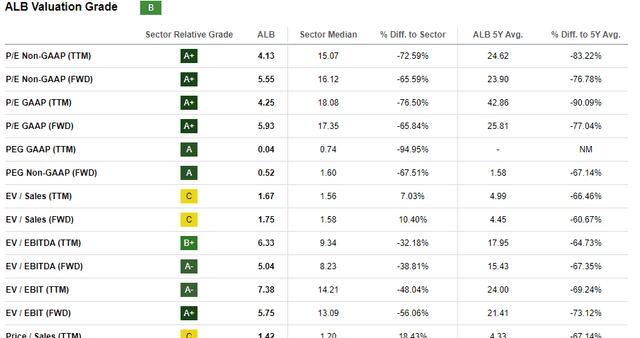

I deter from doing excessive calculations in valuation with this company. For one, cyclical nature of lithium weighs on aspects such as margins, cash flows, earnings, and dividend growth. To have any viable projections, one should guess the price of lithium for the next five years at least. Second, the lithium industry and its supply & demand mechanics are entirely different than ten years ago. Thus, the historical comparison is almost redundant, as we have also experienced a pandemic and a commodity supercycle in the not-too-distant past. These aspects make it very hard to anticipate even the next five years. That said, Seeking Alpha’s valuation ratings provide an optimistic view of the current price relative to the company’s prospects and compared to sector peers. If and when the earnings disappoint, these valuation grades quickly change into less appealing grades.

Seeking Alpha

Per Seeking Alpha’s information, Albemarle’s book value per share is currently $84.34. Should the stock price reach this level, it would provide a good margin of safety and some support for an investor to make good returns. Moreover, tangible book value per share sits at $68.44. If the stock price drops to this level without any meaningful threat to secular tailwinds of the commodity or company, buying would be a terrific opportunity.

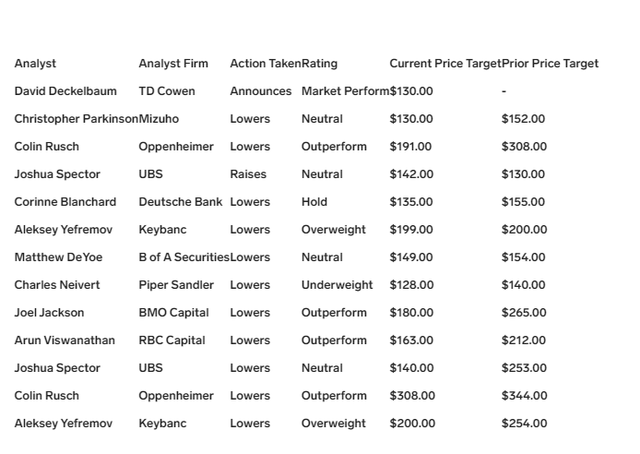

Of course, fair value is higher, and analysts from several firms have issued their fair prices for the company, ranging from $130 to as high as $308. The average of these is $169, 46% higher than the current price of $116 per share. However, it’s important to realize that some price targets follow momentum and quickly react to negative or positive short-term changes, while some price targets assume exuberant growth without a hitch. The reality is often somewhere in the middle, hence the average price target.

Business Insider

Lithium and EV Supply/Demand Commentary

In 2021, the price of lithium started to skyrocket once it became clear that society would invest heavily in a carbon-neutral car industry. Car brands such as Volvo (OTCPK:VOLAF), Mercedes Benz (OTCPK:MBGAF), and Toyota (OTCPK:TOYOF), among dozens of others pledged to move forward with the plan. For a long time, Tesla (TSLA) was the face of all this, groomed to become the absolute leader in the EV space due to its technological, production, and public relations superiority, and for a while the company did rule indeed. However, after billions of investments from companies, different funds, and governments, the EV space is now highly competitive.

As the macroeconomic situation globally isn’t particularly inspiring, demand growth for lithium-powered EVs is decreasing. Higher interest rates make it less appealing to buy cars altogether, which widens the relationship between supply and demand. In addition, higher interest rates and the slowdown that comes with it, decrease the price of oil, making it more alluring to buy an ICE(Internal Combustion Engine) vehicle. A resolution in either the Gaza or Ukraine conflict would also steepen the depreciation of oil. Then again, slowing inflation and the lower price of oil also benefits material and energy cost moderation for miners like Albemarle.

Currently, there are positive signs regarding the FED’s decision to cut rates multiple times this year. Should that come to fruition, businesses would have more leeway to invest in EV tech, making cars more compelling, and consumers would be more inclined to purchase cars again. In the EU, experts expect inflation to come down in 2024, possibly allowing rate cuts once the data shows that 2% inflation will be achieved. If something breaks in the system, the rates should be expected to come down sooner. In China there are numerous challenges in the economy, such as the real-estate crisis and potential deflation. If the central government launches effective policies to combat these problems, there could be light at the end the tunnel. All this leads to the point that with a better economic situation globally, the supply & demand relationship doesn’t worsen as feared.

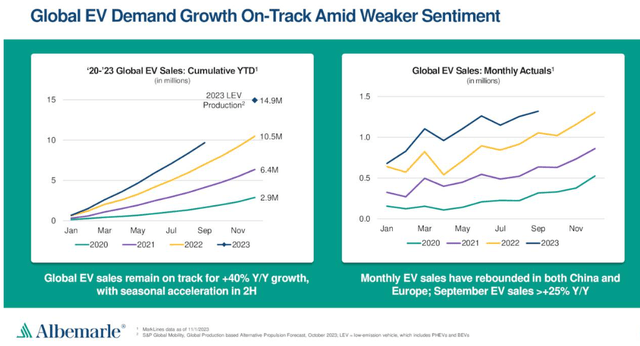

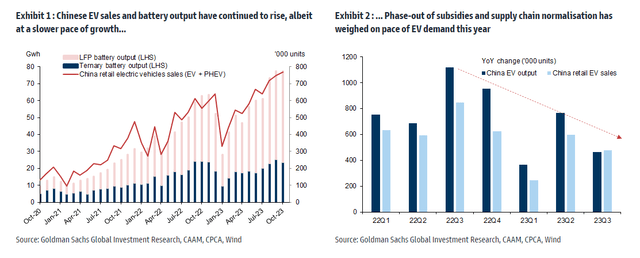

In China, EV sales still increased 38% in 2023 despite the macro headwinds. Globally, the EV market showed a 31% increase in sales in 2023 per market research firm Rho Motion. Below the paragraph is a piece from Albemarle’s Q3 report regarding global EV sales. Again, I refer to Albemarle’s untrustworthy and perhaps exuberant estimations, as in Q3 they expected the 2023 global sales to be +40% Y/Y, but Rho Motion states that the global EV sales were up 31% Y/Y.

Albemarle

Then there’s the other side of the coin. If the supply curve stays the course or outperforms while demand growth continues to fall, it can be another -50% for the lithium prices. What’s worse, those prices can stay stunned as far as 2030. That’s a long time to hold a company like Albemerle.

A Wood Mackenzie article stated on lithium batteries that: “Supply will grow by 45% in 2023 alone, amounting to an excess of 1,380 GWh, and while demand will also increase somewhat, the oversupply issue is expected to persist.”

It doesn’t even matter if the demand picture doesn’t worsen. If it stays the same while supply increases to meet the demand for years in the future, the short-term prices will take a hit nonetheless. Moreover, one needs to remember that even the slightest differences in future CAGR projections can have a meaningful impact on supply/demand equilibrium.

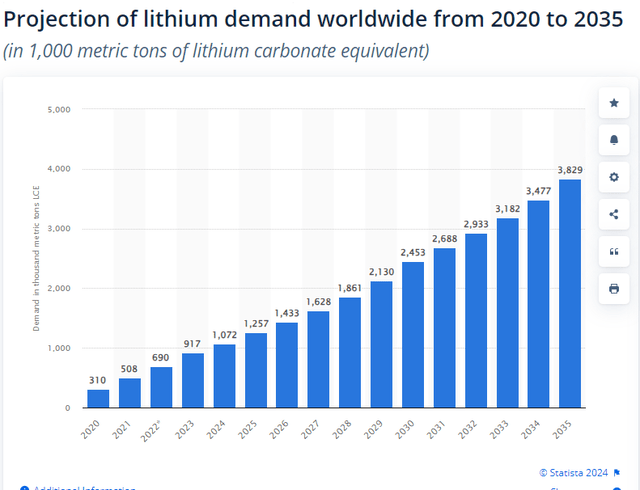

Statista

Statista expects the lithium demand to grow about 14% CAGR from 2025 to 2030. But what if the projection is off by 2%? Instead of LCE demand growing from 1,257 to 2,453 metric tons (in thousands), it will grow only to about 2,220 metric tons. A 2% deviation is likely in either direction since projections for half a decade rarely hit the mark. In reality, the deviation can be much more than 2%, and as the basis point difference grows in CAGR, the projections go awry exponentially.

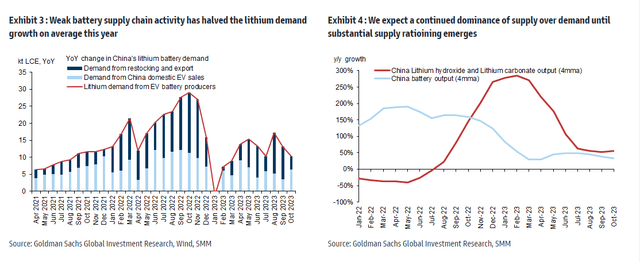

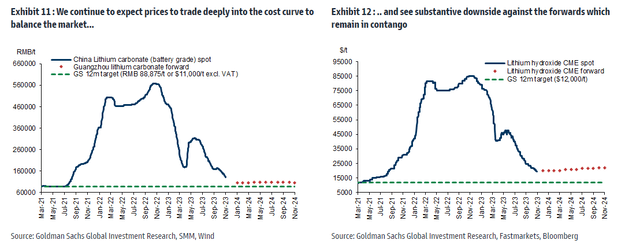

Meanwhile, if the ramp-up in supply persists or intensifies, we look at a whole different supply & demand environment. A higher CAGR in supply compared to demand will have a substantial impact on supply surplus in six years, and that surplus can last for years. Goldman Sachs published an article regarding these surplus issues.

Goldman Sachs Goldman Sachs

This is why it will be prudent to look at production and demand numbers from lithium producers, but also market researchers and end-market businesses like car companies, and how these projections will eventually materialize. As stated previously, lithium producers like Albemarle tend to have much higher expectations, so their projections should be taken with a grain of salt. Growth will not be linear.

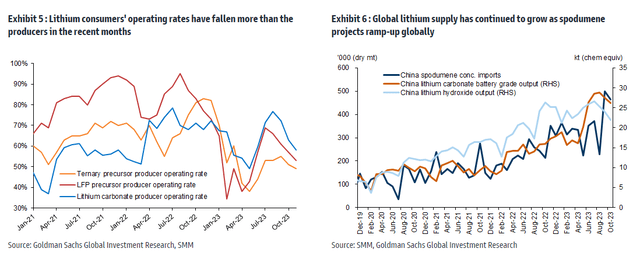

It isn’t clear how much of the current issues are baked into the prices. I suspect the current headwinds are well reflected in prices. However, if the economies of the US and Europe take a step backward or policies change for the worse, there could be additional pressure on prices. In addition, China’s economic performance remains one of the key factors.

Goldman Sachs Goldman Sachs

Altogether, these graphs by Goldman exhibit the risks that prevail in the current lithium market that can linger for years. In Exhibit 11, Goldman anticipates prices to trade down “into the cost curve to balance the market” meaning several project halts and a decrease in supply growth, as it wouldn’t be beneficial for some companies to keep producing. Despite the huge drop in lithium prices, it could very well go even lower and stay there longer than anticipated.

As a native Finn, the EV revolution has yet to provide significant steps in our country’s infrastructure. Excluding the largest cities, the infrastructure is very limited. As the distance covered increases in rural areas, the allure of owning an EV decreases with limited range, maintenance costs, and total price-to-quality relationship. On social media platforms, there seems to be a lot of pessimism and ill-will about full EVs, as people on the more conservative side belittle these vehicles and what the implementation of these vehicles tries to accomplish. Moreover, whenever there’s a crash or a singular flaw involving a Tesla, the brand is always first to be mentioned in a headline. The picture below gives an example of a Finnish tabloid Iltalehti article about an accident that involved a Tesla going through a rail in Turku(nobody died). I have no doubt this phenomenon of getting clicks and conversation is global, but this always paints a more negative picture regarding EVs, which Tesla is the face of. You don’t see these kinds of headlines when a vehicle is a Toyota.

Iltalehti

What follows is that there will be less incentive to invest in EV endeavors or vote for politicians driving the change. Thus, the EV infrastructure remains relatively insignificant, keeping up the vicious cycle. Of course, per EU’s new regulation, all new cars and vans registered in 2035 and after in the EU are set to be zero emission. This is still 11 years away, but at least there is a time horizon for concrete change. However, the EU only accounts for 448 million people of the 7.8 billion global population, which is rather meager considering the total population. Also, the German government increased short-term headwinds by discontinuing a subsidy program for EVs.

This all points to the presumption that while the EV revolution is undoubtedly gaining ground, the macroeconomic environment, particularly in Europe, doesn’t bode well for short-term investment toward electrifying the traffic or the demand for lithium-ion batteries. It’s also worth noting that 2024 is a super year for elections globally, with most elections in history for one year. For example, the US, EU, and UK will all see elections this year. This can have considerable implications for subsidy programs regarding EVs and the clean energy industry overall.

Risks

There are multiple risks regarding the investment.

- The mining industry is subject to regulatory and political issues regarding ESG. A report from Chile came out that about 500 protesters, mostly indigenous groups, interfered with lithium salt flat operations by blocking several roads to the site. While Albemarle stated that operations “continue as usual”, the matter has not likely seen the end of it. Regulatory issues could affect aspects of the business, such as access to resources and cost structure. One main concern of this is politics in Chile, which remains uncertain. As stated earlier in the SQM discussion, nationalization effects shouldn’t be taken lightly.

- Sodium-ion batteries pose a competitor for their lithium counterpart. Sodium batteries are 30% cheaper than lithium batteries, which makes them more financially accessible. However, sodium batteries also contain lower energy density, resulting in lower battery life. This means less range and power for EVs, for example. BYD(OTCPK:BYDDF) launched its Seagull model in April 2023 and plans to adapt sodium-ion, and lithium-ion battery versions. In short, sodium batteries would be more practical in metropolitan areas with a vast charging infrastructure, and lithium batteries would be more suited to rural areas and perhaps high-performance vehicles. There is also constant development of new technology to improve the EVs, which poses potential challenges for lithium if a challenging technology emerges.

- The commodity market is also known for being highly volatile and unpredictable. This means that the price of lithium can drop even further without breaking a sweat if variables like economic slowdown fuse with a supply glut. Because of the high correlation between lithium prices and the stock price, the stock can stay down indefinitely without any regard for prospects or intrinsic value. However, it’s better to buy into a business when its underlying commodity with secular tailwinds has dropped more than 80%.

Whenever there’s been a significant oversupply of anything, it’s more often than not a good time to buy if there are long-term tailwinds. Oil has always been the prime example of this. In the middle of the 2008 financial crisis, the oil demand plunged, and Crude Oil WTI reached $42. From 2014-2016, booming US production resulted in a supply glut, and oil prices dropped 70%. While lithium is not as essential to the way of life as oil has been, the growing demand is indisputable. The same cyclical logic can be applied to lithium, until there’s a replacement for lithium.

Macrotrends

- The greatest risk remains timing. I do not doubt that in the long-term, the investment done today makes you nominal returns in the future. The question remains: how fast and how much? In a commodity business, timing is much more important due to its cyclical nature, and buying low and selling high is the trade investors try to make when there aren’t spectacular dividend payments incoming. There is a chance that opportunity cost is what hurts the most, not the depreciation of the stock. If the price stays negative or flat for multiple years, it becomes increasingly difficult to hold on without concrete short to medium-term catalyst in sight. Especially if other stocks and commodities rally. Stomach and conviction are a must.

Final Thoughts

All things considered, it’s not the right time to get in despite the horrendous drop in share price, secular tailwinds, and healthy financials. I would wait until I see more clearly which way the demand and supply dynamics are leaning. Current and prospective shareholders should especially keep an eye out for quarterly results and guidance and how those reflect the comments and expectations from previous quarters. Of course, current shareholders could DCA(dollar-cost average) if the average cost basis is higher than the current price. One should also have the liquidity to continue should the price plummet further.

This could very well be an ultimate buying opportunity, as many of the recent articles make it out to be, but this could also be an investment without meaningful capital gains years from now. Even so, long-term investors are in no rush and can afford to wait years for that appreciation and pump more into the position as long as prices stay down, perhaps leading to a market-beating CAGR in the long run. Nonetheless, I still think there are better risk/reward securities that I’d buy right now rather than lithium stocks. As attractive as ALB and other lithium plays seem, I will gladly miss out on some first gains until there’s a clear indication that there’s not an ugly and lengthy supply glut incoming.

And if it turns out to be the feared supply glut, prospective buyers should be patient to see the bottom accompanied by project halts from even the biggest producers.

Read the full article here

")

Q4 2024 Earnings Call Transcript")

")

")

")