")

")

")

I initially covered AFC Gamma (NASDAQ:AFCG) in May, rating it a Hold. This decision was informed by a mostly positive view of its role as a real estate lender for the cannabis industry, where supply of capital is low and allows for attractively high yields on its loans. AFCG’s story, however, was complicated by its portfolio of distressed, non-cannabis loans in commercial real estate that were pending SEC approval for a spinoff into Sunrise Realty Trust (SUNS).

Since then, the spinoff was approved and completed, and Q2 2024 results were also released. It’s time to take another look and see how AFCG fares with these changes

Q2 Results

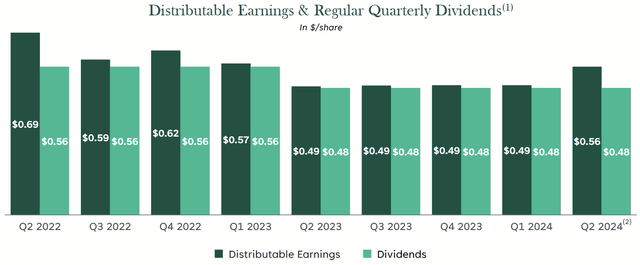

The first thing to observe is that distributable EPS increased in Q2 after a trend of slacking.

Q2 2024 Company Presentation

Standing at $0.49 from Q2 2023 to Q1 2024, it rose to $0.56 this quarter. The quarterly dividend remained at $0.48.

Q2 2024 Company Presentation

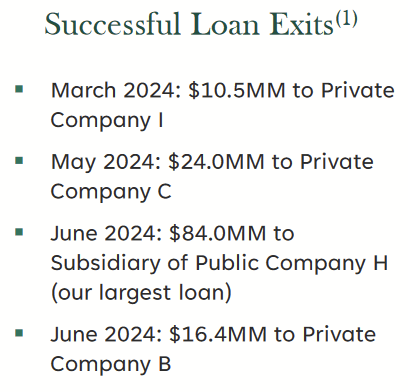

The period also featured some important exits of loans that were experiencing trouble. Crucially, their $84M loan, the largest on their book, was sold for par plus accrued interest. This and similar moves showed the resourcefulness of management in preserving capital and adapting to the distress on the book.

Effects of Spinoff

I would say more about the details of Q2, but many of them were quickly rendered obsolete, as these results include those of the CRE portfolio that was spun off just days after the end of the quarter, so any further discussion of those financial figures needs to be done in this context.

First, let’s discuss the perceived discount to book value that persists.

AFCG P/B 6M History (Seeking Alpha)

Prior to the spinoff, there was a discount. The steep drop in July makes it appear that an even steeper one emerged, but this is not the case, as Price/Book quotes utilize the most recently disclosed book value, and that would be based on Q2’s balance sheet that still contains the CRE.

Management did provide clarity on the material difference, however, during the earnings call:

As of June 30, 2024, our total shareholder equity was $314.3 million, and our book value per share was $15.21. After the quarter ended, we completed the spin-off of our CRE portfolio, which included the distribution of approximately $115 million of loans and cash or approximately $5.56 of book value per share.

Simple math suggests that book value should be about $9.65 per share based on that, and Q3 will provide an update in line not only with the spinoff but that quarter’s activity. With that in mind, the P/B is at least 1.0 and likely at a modest premium.

The dividend was also called into question during the call, and management gave an oblique answer:

So from a dividend standpoint, I think as Dan said in his remarks, the Board will declare their dividend on the normal cadence. If you think about – we’ve declared a $0.48 dividend for the last five quarters, I believe. And if you just think about the spin-off, we kept about two thirds of assets and we spun off one third of the asset.

It requires some interpreting, as “normal cadence” means the quarterly payment schedule is likely to continue, but it only implies that distributions will remain the same.

We do have some clues, however. Sunrise, now spun off, announced what their full quarterly distribution will be: $0.42 per share. With about 6.9M shares outstanding as of August 14th (SUNS latest 10Q), that resolves to a cash distribution of about $2.9M, while AFCG’s distributions for Q2 amounted to about $9.9M, for a difference of about $7M. This suggests AFCG’s quarterly dividend could be 70% of what it has been until recently, close to the two-thirds impact to book that was mentioned.

This would resolve to about $0.34 per share, for an annual yield of about 13%.

Other Updates

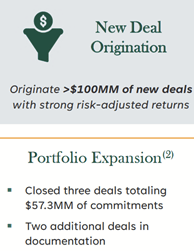

In addition to all of this, AFCG recently issued three new loan deals.

Q2 2024 Company Presentation

This brings YTD total investments to $57M, with the full 2024 goal to reach $100M.

Q2 2024 Company Presentation

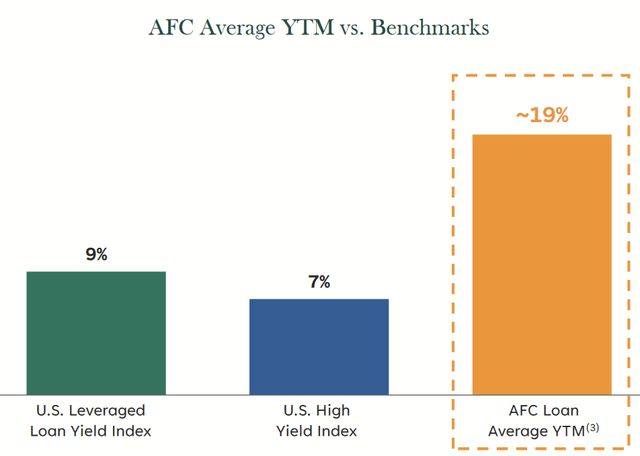

Throughout all of this activity, they reported a yield-to-maturity of 19% on their loan book, down slightly from 20% since my last coverage but otherwise attractive.

Q2 2024 Company Presentation

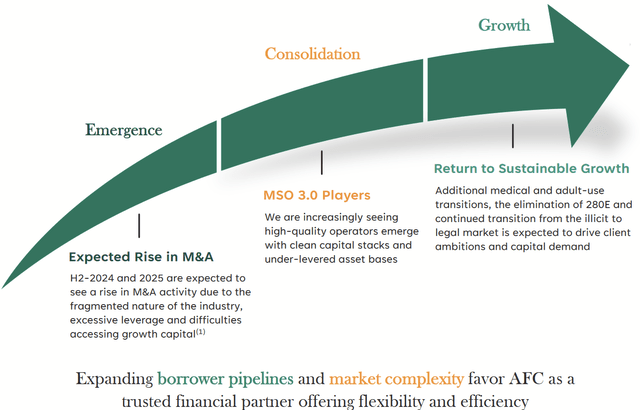

While trends toward growth in the cannabis industry have been the main selling point for both operators and REITs like AFCG, management provided more insight on the near future. They believe that M&A activity will pick up and drive further demand for capital.

This is not just a growth opportunity, but consolidation in the cannabis industry could lead to improved cost structures and thus a better credit profile of the existing portfolio, as well as their deal pipeline.

As Q3 approaches, I think it will be important to review the updated portfolio, along with which liabilities they kept and which ones were imparted to SUNS.

Conclusion

AFC Gamma took some important steps in the last few months, improving their loans and successfully spinning off Sunrise without regulatory hiccups to become a cannabis pure play. This simplifies the future outlook and removes the headache of the risky commercial real estate segment.

Not all the smoke has cleared, however, as quarterly results sans Sunrise’s results will be helpful to show how the company does without them. Information provided by AFCG and SUNS since the spinoff does help us determine that book value is likely just under $10 per share and that the dividend yield may only be 13%. For those reasons, I suspect AFCG is fairly valued for now, and it’s better as a Hold until there’s a more apparent discount or more reason to think that these investment opportunities will translate to growth in distributable EPS.

Read the full article here

")

")