")

Q1 2025 Earnings Call Transcript")

")

Picking the right stock to buy is a big responsibility, as it should be, considering that you’re essentially putting your hard-earned capital to work for you while you sleep.

This is akin to hiring the right employee for the job, especially for long-term investors who’d prefer not to constantly switch in and out of stocks, resulting in high turnover in a portfolio.

As such, these are potential questions that one may want to ask themselves about a stock before making a purchase:

- Does the company have durable assets and competitive advantages?

- Does the stock have the potential to pay a steady and growing dividend backed by strong cash flows?

- Is the stock reasonably value and does it carry a strong balance sheet?

Going through this mental checklist can help you to filter out those stocks that don’t meet your criteria and zero in on those that do.

This brings me to the following 2 picks which appear to check a lot of those aforementioned boxes and make them sleep well at night for income and potentially strong total returns, so let’s get started!

#1: American Tower

American Tower (AMT) is the largest cell tower REIT on the market today, with a strong presence in both the U.S. and internationally. At present, it has a network of 224K communications sites and a highly interconnected collection of U.S. data center facilities.

AMT is the type of business that is able to grow in both good times and bad, given the essential nature of its communications sites that serve major telecoms AT&T (T), Verizon (VZ), and T-Mobile (TMUS).

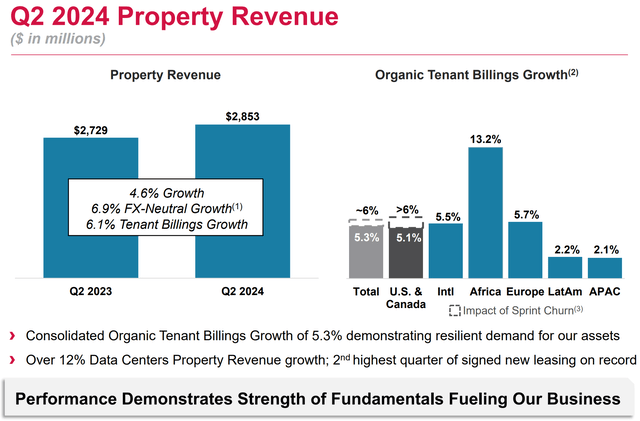

This includes the most recent Q2 2024, during which AMT saw property revenue grow by 4.6% YoY and adjusted EBITDA growth of 8.1% YoY. Importantly, AFFO per share grew by a robust 13.4% YoY. These results were driven by steady growth in the core cell tower business along with net new signings from CoreSite, AMT’s data center business.

As shown below, organic tenant billings growth came from all geos, specifically in Africa and Europe, which led international growth.

Investor Presentation

In fact, AMT’s CoreSite achieved its second-highest quarter of signed new business on record, further validating the potential of AMT’s data center strategy and the acquisition made in 2021. CoreSite saw double-digit revenue growth and is seeing high demand from clients with 60% of its projects currently under development being pre-leased, sitting at 4x the historical average.

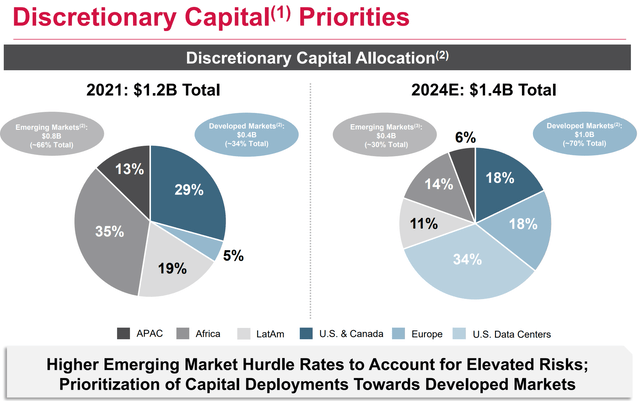

Management raised its full-year AFFO per share guidance from $10.42 previously to $10.60 per share, representing an impressive 7.4% YoY growth considering the current higher interest environment. This is driven by a pivot in management’s strategy as it looks to optimize the portfolio toward higher yielding assets, which includes divestiture of certain assets in Asia and investments into data centers.

As shown below, Asia now represents just 14% of 2024 capital investments, down from 35% in 2021 and Data Centers now comprise 34% of investment capital, up from zero in 2021.

Investor Presentation

Meanwhile, AMT carries a solid balance sheet with BBB- credit rating from S&P. This is supported by a net debt to EBITDA ratio of 4.8x, sitting below the 5.0x from Q1 and below the 6.0x level generally considered safe for REITs, and $9.2 billion in total liquidity. Moreover, 89% of AMT’s debt is held at fixed rate with a weighted average remaining term of 5.8 years.

This lends support to the 2.9% dividend yield, which is well-covered by a 61% payout ratio. While management did reset the dividend to $1.62 after topping out at $1.70 in Q4 of last year, this puts AMT on better financial footing for operational and dividend growth.

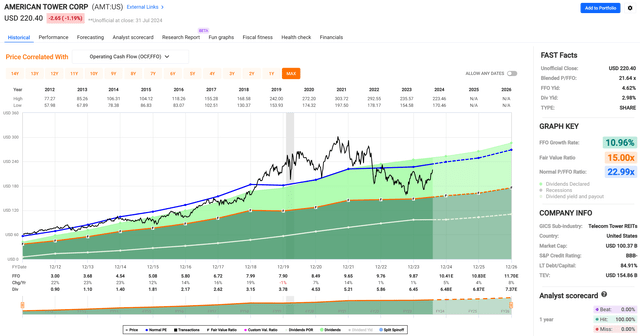

Lastly, while AMT isn’t particularly cheap at the current price of $220.40 with forward P/FFO of 20.8, it is cheaper than its historical P/FFO of 23.0, as shown below.

FAST Graphs

With mission-critical assets, a near-3% dividend yield, and long-term FFO/share growth estimates in the 7-10% range, AMT represents a compellingly strong income and growth stock opportunity with sleep-well-at-night attributes.

#2: Alexandria Real Estate

Alexandria Real Estate (ARE) is another moat-worthy REIT that holds irreplaceable and mission-critical assets. This includes a strong portfolio of office properties that are strategically located in innovation clusters, serving tenants in the biotech sector.

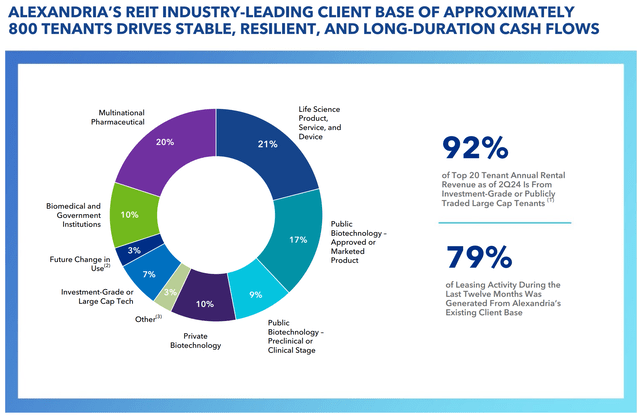

ARE’s markets include New York City, Boston, SF Bay Area, San Diego, Seattle, Research Triangle of North Carolina, and Maryland, and serves 800 tenants in the life science, biotech, and pharmaceutical industries. As shown below, 92% of ARE’s rental revenue is generated from investment grade rated or large cap publicly traded tenants.

Investor Presentation

ARE has a strong track record of value creating compared to peers. While ARE is technically an office REIT, its tenant base makes it closer related to healthcare REITs, especially considering that diversified healthcare REITs like Ventas (VTR) and Healthpeak Properties (DOC) are pivoting toward the life sciences sector.

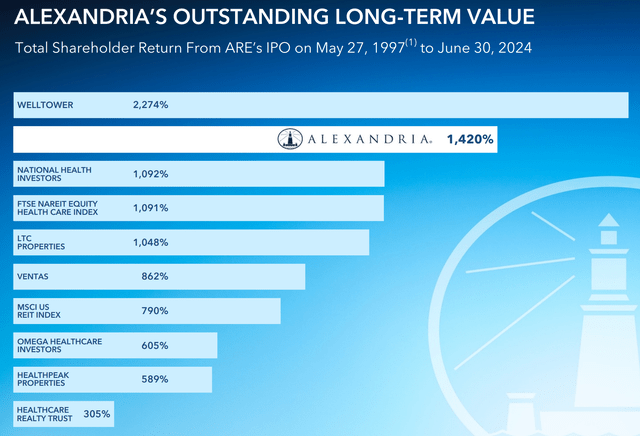

As shown below, ARE’s total return is second only to Welltower (WELL) since its inception in 1997.

Investor Presentation

Like AMT, ARE is also performing strongly in the current environment, with same property NOI growth of 3.9% YoY and FFO per share growth of 5.4% YoY during Q2 2024. For the entire first half of the year, ARE achieved solid FFO/share growth of 6.3% over the prior year period.

This was driven by ARE’s high-quality asset base with amenities and sticky tenant relationships, especially considering that 83% of ARE’s leasing activity during the second quarter was existing tenants. This helped ARE to achieve GAAP and cash rental rate increases of 7.4% and 3.7%, respectively, in the quarter.

Management is guiding for AFFO per share of $9.47 at the midpoint of range for the full-year 2024, representing 5.6% growth from 2023. This is to be driven by continued strong expectations for strong leasing activities. ARE also plans to recycle capital and double-down on its strategy of investing in mega campuses. At present, 74% of ARE’s annual rental revenue comes from mega campuses and management expects to raise that to 90% over the next few years, furthering its moat and attractiveness to both new and existing tenants.

ARE’s continued transformation is supported by one of the best balance sheets in the REIT sector, and it carries BBB+/Baa1 credit ratings from S&P and Moody’s. It has a low net debt + preferred stock-to-adjusted EBITDA ratio of 5.1x and significant $5.6 billion in liquidity. The majority (97%) of its debt is held at a fixed rate with a weighted average remaining debt term of 13 years, one of the longest in the REIT industry.

Importantly for income investors, ARE currently yields an appealing 4.4% and the dividend is well-protected by a 55% payout ratio. It also comes with 13 years of consecutive growth and a 5-year dividend CAGR of 5.6%.

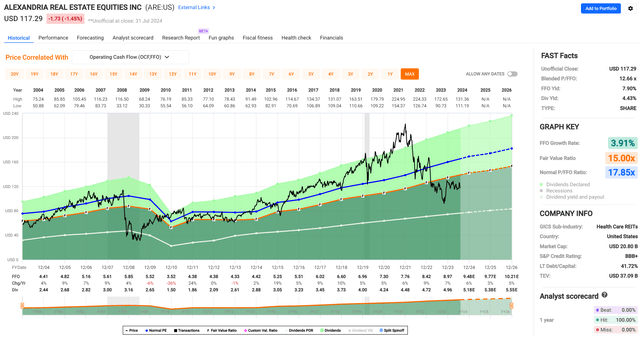

Lastly, ARE is attractively valued at the current price of $117.29 with a forward P/FFO of 12.4, sitting far below its historical P/FFO of 17.9, as shown below.

FAST Graphs

With a 4.4% yield and potential for mid to high-single digit annual FFO per share growth over long term, driven by rental increases and portfolio transition toward even stronger assets, ARE could produce market-beating returns and a potential reversion to its mean valuation could provide an extra return kicker beyond that.

Investor Takeaway

American Tower and Alexandria Real Estate both present moat-worthy opportunities with mission-critical assets and robust financial performance. AMT, the largest cell tower REIT, benefits from its expansive network and data center strategy, demonstrating steady growth and a solid balance sheet, making it a reliable income and growth stock.

Similarly, ARE carries a strategic portfolio in innovation clusters catering to the biotech sector, supported by high-quality tenants and a strong balance sheet. Both companies offer attractive valuations, dividends and growth potential, making them ideal for long-term investors seeking potentially strong total returns.

Read the full article here

")

Q1 2025 Earnings Call Transcript")

")

")