")

")

Introduction

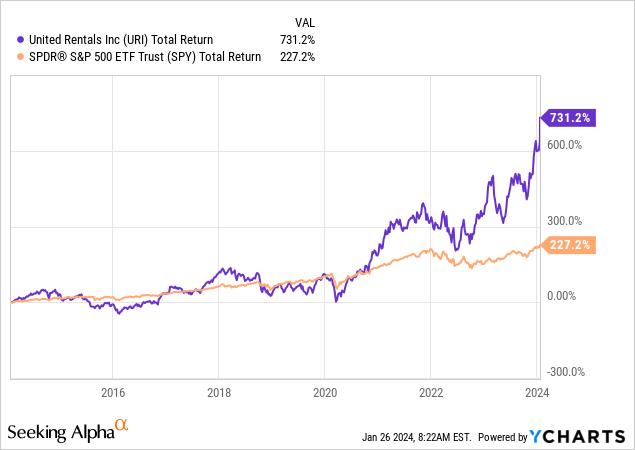

It’s time to talk about a company I have followed for many years. A company that, albeit with significant volatility, has turned into one of the biggest wealth generators on the market.

That company is United Rentals (NYSE:URI), which has returned more than 730% over the past ten years, which is more than 500 points higher than the already impressive 227% return of the S&P 500.

On November 28, I wrote my most recent article on the company, titled “What Makes United Rentals One Of The World’s Best Companies.”

Here’s a part of my takeaway back then:

United Rentals stands out as a top performer, earning a spot on TIME’s World’s Best Companies 2023 list.

Despite economic challenges, URI’s strategic focus on technology and unique customer demands has fueled its growth.

The company’s recent strong Q3 results, positive indicators for 2024, and robust financial position underscore its resilience.

Since then, URI shares have risen by 41%.

Let me say that again. Since the end of November, roughly two months ago, United Rentals has added more than 40% to its market cap.

In this article, we’ll re-assess the risk/reward using the company’s just-released earnings, which not only tell us a lot about the company but also about the market/economic environment.

So, as we have a lot to discuss, let’s get right to it!

United Rentals Is Firing On All Cylinders

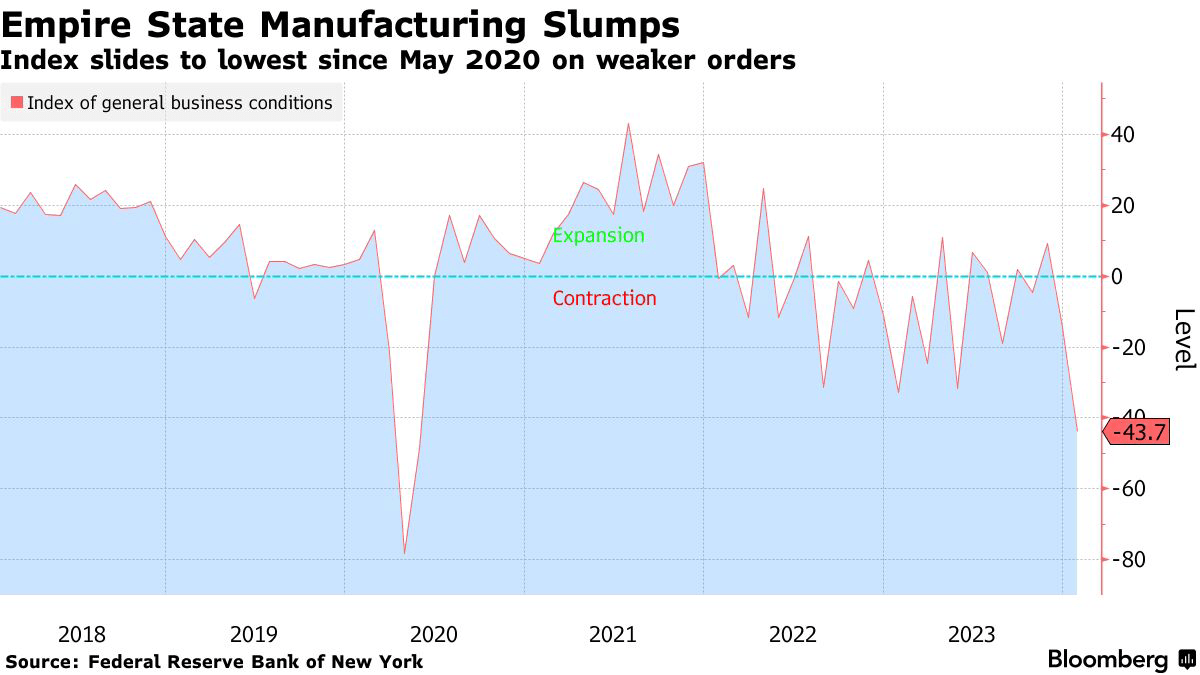

Although we’re seeing some economic weakness in manufacturing – one of them being the New York (Empire State) Fed Manufacturing Index – construction is doing just fine.

Bloomberg

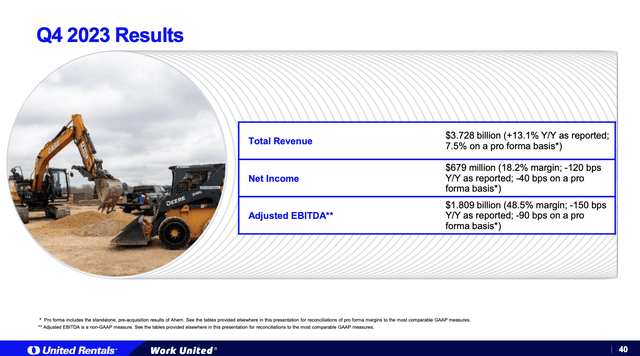

Rental revenue for the fourth quarter reached a record $3.12 billion, marking a substantial year-over-year increase of $372 million or 13.5%.

This impressive growth was attributed to the company’s solid positioning in large projects and the diverse strength observed across various end markets.

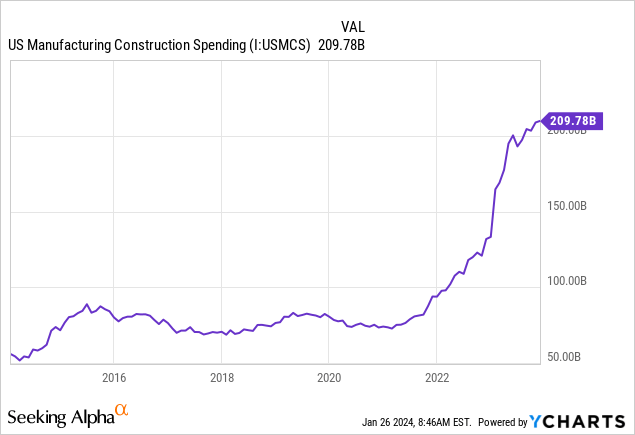

After all, this is what manufacturing construction spending in the U.S. looks like:

Breaking down the rental revenue, Operating Equipment Rental saw a significant increase of $313 million or 13.9%. This growth was facilitated by an expansion in the average fleet size, contributing 15.1%, while fleet productivity added a marginal 0.3%. However, there was a partial offset due to assumed fleet inflation of 1.5%.

Ancillary revenues within the rental segment also experienced a significant rise, higher by $61 million or 14.2%.

United Rentals

Furthermore, the used equipment segment saw positive results, with proceeds increasing by over 7% to $438 million in the fourth quarter.

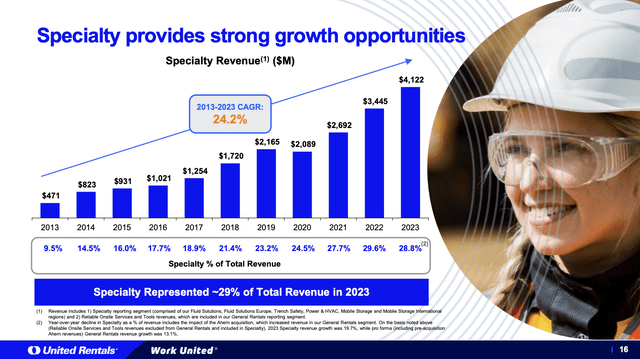

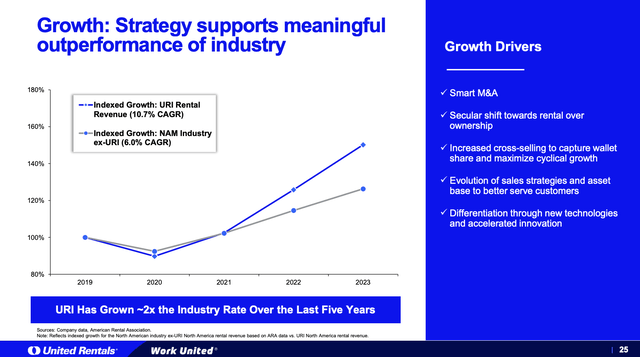

The Specialty business segment delivered another strong quarter, with rental revenue up 15% year-on-year. This growth was spread across all businesses within the Specialty segment and is a good sign that the company’s investments in specialty equipment are paying off.

Bear in mind that this segment has grown by 24.2% per year since 2013!

United Rentals

Meanwhile, the adjusted use margin remained flat sequentially at 55.3%, while adjusted EBITDA for the quarter reached a record $1.81 billion, reflecting a significant 10% year-on-year increase.

However, despite these numbers, the EBITDA margin decreased to 48.5%, primarily due to the combined impact of the Ahern acquisition and used margins.

Adding to that, the return on invested capital (“ROIC”) increased by 90 basis points year-on-year to 13.6%.

This number exceeded the weighted average cost of capital by over 260 basis points, indicating a strong financial performance.

Unsurprisingly, adjusted EPS saw notable growth, expanding by 16% to reach $11.26.

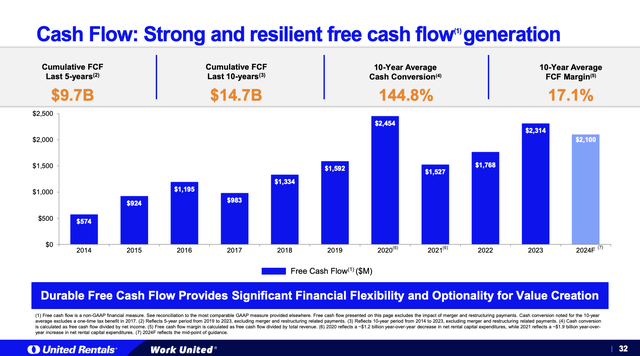

Related to that, free cash flow for the full year surpassed $2.3 billion, translating to a robust free cash margin of 16.1%.

United Rentals

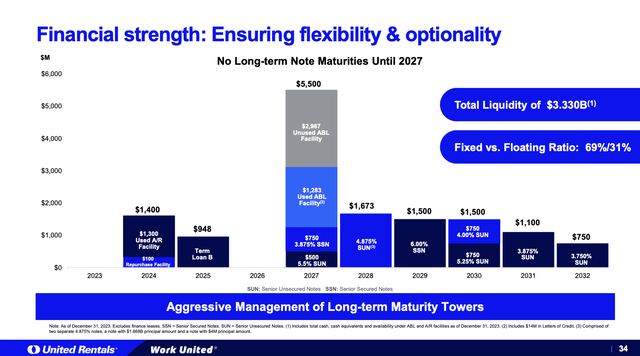

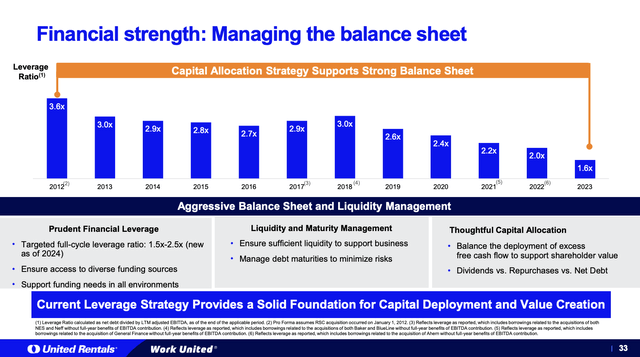

On top of that, the company lowered its net leverage ratio to 1.6x EBITDA. Total liquidity exceeded $3.3 billion, and URI has no long-term maturities until 2027, which buys it a lot of time in the current environment of elevated rates.

United Rentals

Going into 2024, the company has a net leverage ratio close to the bottom of its 1.5x to 2.5x range.

United Rentals

With all of this being said, let’s take a closer look at the market environment and the company’s outlook.

What’s Next?

During its earnings call, the company noted that customer activity and market trends revealed broad-based demand across geographies, verticals, and customer segments.

Industrial end markets experienced healthy growth, with a particular emphasis on industrial manufacturing and power sectors.

Within construction markets, both infrastructure and nonresidential demand showed solid growth year-over-year.

Notable projects included those in battery plants, semiconductor-related jobs, power, infrastructure, and data centers.

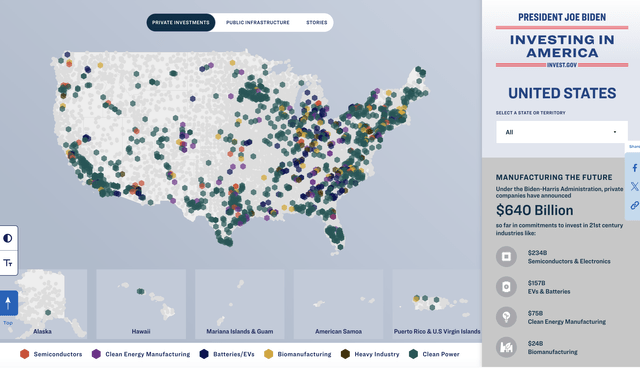

Related to these developments and the manufacturing construction spending chart I showed in this article, the map below shows major private construction investments in projects like semiconductors, clean energy, and others.

The White House

With these developments in mind, the company made clear that it believes that the future remains bright, with expectations of 2024 being another year of growth, primarily led by large projects.

This optimism is supported by positive customer sentiment indicators, solid backlogs, and feedback from field teams.

During the earnings call, the company also expressed confidence in its ability to outperform the industry, capitalize on opportunities, and achieve another record year in 2024.

United Rentals

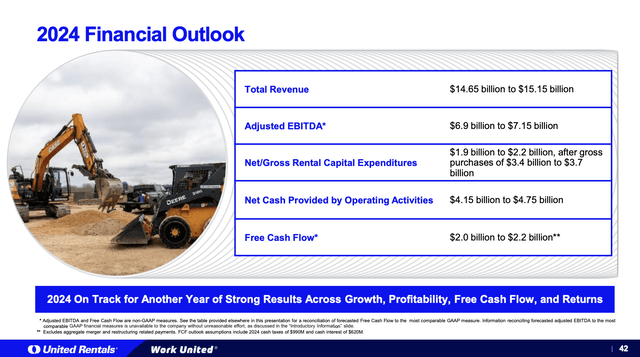

As a result, total revenue is expected in the range of $14.65 to $15.15 billion, implying a full-year growth of about 4% at the midpoint.

Adjusted EBITDA guidance was set at $6.90 to $7.15 billion.

United Rentals

Adding to that, one of the reasons why the company lowered its net leverage target range is to pave a healthier way for long-term shareholder distributions and financial health.

When adding this strong outlook, it is no surprise that management decided to ramp up shareholder distributions.

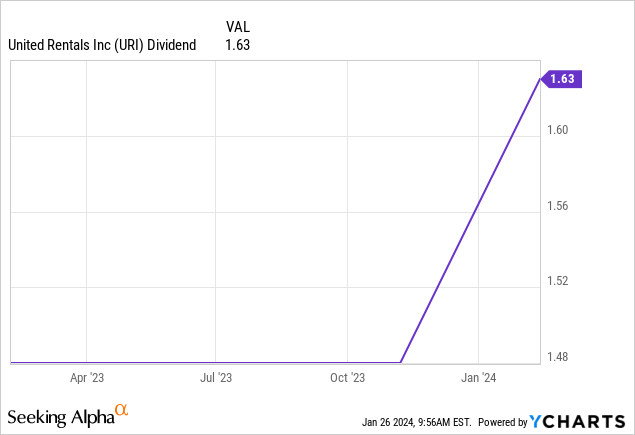

The company announced that the quarterly dividend would be increased by 10.1%, which reflects its commitment to consistent dividend growth aligned with long-term earnings.

URI currently pays $1.63 per share per quarter, which translates to a yield of 1.0%.

This is the company’s first dividend hike since it initiated its dividend last year.

Additionally, the company announced plans to repurchase $1.5 billion of common stock in 2024, representing 3.5% of the company’s current $43 billion market cap.

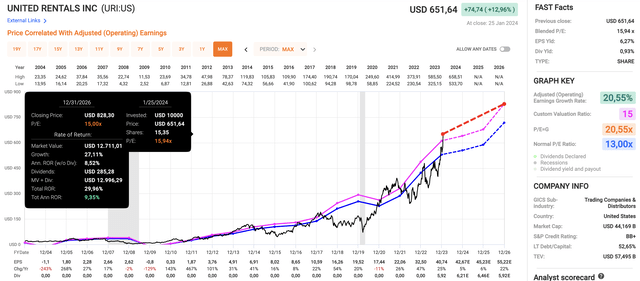

Valuation

When it comes to URI’s valuation, the stock continues to enjoy upside potential.

Using the data in the chart below:

- This year, EPS is expected to grow by 5%, followed by 6% growth in 2025 and 22% growth in 2026.

- Currently, URI trades at a blended P/E ratio of 15.9x, which is above its long-term normalized multiple of 13.0x.

- However, as URI has become more mature and significantly improved its financial position, I believe a 15x multiple is warranted.

FAST Graphs

Based on these numbers, the company has the potential to return roughly 9% per year through 2026. Since 2004, URI shares have returned 18.4% per year.

However, although I will remain bullish on URI, it needs to be said that after such a rally, it may be best to wait for a correction before jumping in. Unless manufacturing sentiment improves soon, we could see some selling pressure as market participants potentially bet on a manufacturing recession.

On a long-term basis, I expect URI to shine, benefitting from secular industry growth, a fragmented market, rising dividends, buybacks, and a healthy balance sheet.

Takeaway

United Rentals continues its impressive performance, demonstrating resilience in the face of economic challenges. The recent Q4 results showed substantial growth, with rental revenue hitting an unprecedented $3.12 billion. The company’s strategic focus on technology and diverse end markets, especially in large projects, contributes to its success. Despite the EBITDA margin dip, URI’s financial performance remains robust, with a significant increase in adjusted EPS and free cash flow.

Looking ahead, the company anticipates another year of growth in 2024, supported by positive customer sentiment and solid backlogs. Meanwhile, the decision to increase shareholder distributions reflects confidence in URI’s future prospects, making it a compelling long-term investment – preferably on stock price weakness.

Read the full article here

")

")

")

")

")