")

(NYSE:GE)")

General Electric (NYSE:GE) reported quarterly earnings for 4Q-23 on Tuesday which beat estimates: The industrial company said it earned $1.03 in adjusted profits, handily beating the Street’s $0.89 estimate.

The EPS outlook for 1Q-23 is what caused General Electric’s stock price to slump 3% in trading before market open on Tuesday. Nevertheless, the conglomerate is seeing robust order strength, particularly in its Aerospace segment which has started to shine in 2023.

The energy infrastructure business is expected to be spun out in the second quarter which will only serve to highlight General Electric’s robust Aerospace division performance.

Though I missed the boat on General Electric last year, I think that General Electric’s quarterly earnings were very solid, including its free cash flow outlook, and I think that General Electric, despite its high price tag, is a solid Buy.

My Rating History

General Electric, after reporting better-than-expected third quarter results caused me to modify my stock classification from Sell to Hold in October and I am further raising my stock rating by one notch to Buy after the industrial conglomerate completed the year with a stellar fourth quarter.

General Electric is seeing robust growth in the Aerospace business and reported a big increase in free cash flow in 2023. The forecast for 2024 implies that the company is set for robust growth as well and I think investors are overreacting to the 1Q-24 outlook.

General Electric Is Killing It In Aerospace

General Electric’s Aerospace segment killed it in the last quarter. The segment already did quite well in General Electric’s preceding quarters, predominantly because the airline industry is rebounding from the Covid-19 pandemic and ordering a boatload of airplanes. Thus, it did not come as a surprise that General Electric enjoyed some ongoing momentum here in the fourth quarter.

GE Aerospace, which is now the biggest sales contributor within General Electric and has profits of more than twice the size of the next-biggest segment, energy, is seeing robust growth in orders.

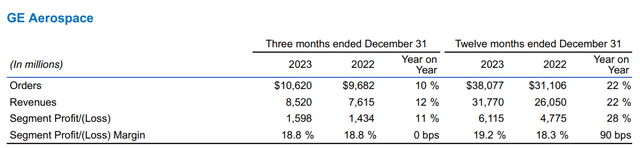

Orders in GE Aerospace were +10% YoY in 4Q-23 and 22% in 2023. Fourth quarter sales came in at $8.52 billion, reflecting 12% YoY growth. On a full year basis, the segment produced 22% sales growth and 28% profit growth, thanks to a resilient demand for commercial engines and related services.

GE Aerospace Segment (General Electric)

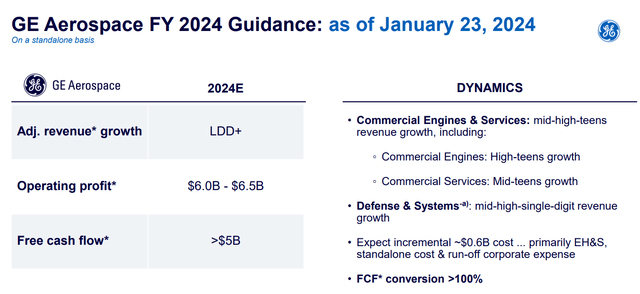

The industrial company also laid out its financial expectations for the Aerospace segment for 2024 which is expected to continue to rake in big bucks.

The segment is anticipated to grow at sales at least 10% this year and throw off more than $5 billion in free cash flow this year. Projections for 2024 are supported by strong trends supporting growth for commercial engines and defense systems.

GE Aerospace FY 2024 Guidance (General Electric)

The long term outlook is also positive. Obviously, based on its free cash flow guidance, General Electric expects resilient demand for jet and turboprop engines in 2024 and the aviation industry is in a broad upswing after Covid-19.

Global air traveler roared back in 2023 and with the market expecting a record year for airliners, I think that General Electric is set to see prolonged growth in its order and services book.

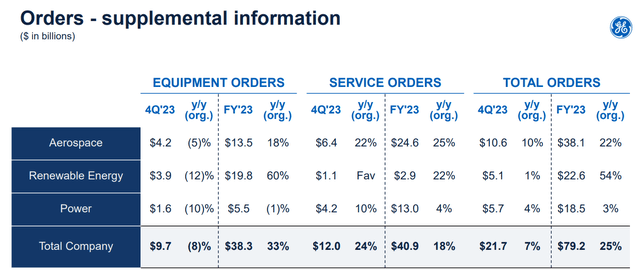

Aerospace is seeing momentum in both equipment and service orders, a trend that accelerated in 2023. Aerospace segment service orders skyrocketed 25% in 2023 and the generally positive aviation industry outlook should support robust growth in both services-related segment as well as equipment orders.

Orders (General Electric)

Free Cash Flow Is Ramping Up Big Time

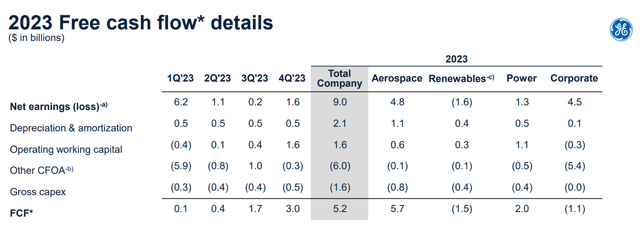

As far as the conglomerate’s free cash flow was concerned, General Electric had a top quarter here as well. Based on the cash flow summary released as part of General Electric’s 4Q-23 earnings, General Electric produced $5.2 billion in free cash flow in 2023 which reflects a YoY growth rate of 68%.

The industrial conglomerate added a total of $2.1 billion in free cash flow to its 2022 FCF total and the overwhelmingly majority came, you guessed it, from the Aerospace division. This segment contributed $5.7 billion in free cash flow in 2023 which was offset by a $1.5 billion free cash flow loss in the restructuring Renewables segment.

All things considered, GE Aerospace once again lifted up General Electric’s entire quarterly earnings.

2023 Free Cash Flow (General Electric)

1Q-24 EPS Outlook

General Electric forecasted $0.60 to $0.65 per share in adjusted profits which fell short of the consensus of $0.70 per share. The shortfall probably explains the market’s initially negative reaction, but it only clouded, in my view, an otherwise solid earnings release.

General Electric Is Not Cheap, But Does Have Upside (And A Catalyst)

General Electric’s free cash flow outlook for 2024 shows us that the conglomerate anticipates a rather solid year in operational and financial terms, particularly because of robust underlying demand from the airline industry.

Based on $5 billion in estimated free cash flow (GE Aerospace) for 2024 (plus $0.7-1.1 billion for GE Vernova, on a standalone basis), the conglomerate’s stock is selling for 25x free cash flow. 3M, Inc. (MMM), a peer industrial conglomerate, is at a much lower free cash flow multiple of 9x.

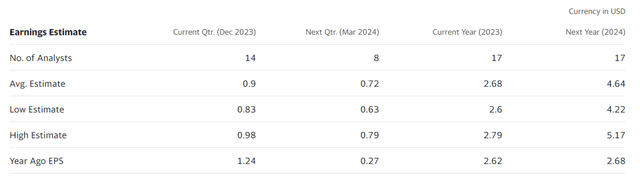

The market consensus estimate for General Electric’s 2024 profits is $4.64 per share and underpinned by expectations of a resilient market for engine parts and services.

General Electric is presently selling for 28x leading (2024) earnings while 3M sells for 11x leading earnings. Taking into account General Electric’s robust free cash flow forecast, upcoming Vernova spin, Aerospace focus and strong economic backdrop, I think that GE could achieve a 30x earnings multiple.

The stock price target with this multiple is $139.60 (based on leading earnings). This is my personal opinion and my willingness to pay a premium multiple depends primarily on the strength of the economy which presently provides crucial valuation support for the investment thesis.

Though 3M is cheaper, and I previously stated that I see 3M as strong industrial franchise value, I think that General Electric represents good value for investors regardless because it has a very substantial catalyst coming up: The industrial company is going to spin off its energy infrastructure business, GE Vernova, which creates a standalone aircraft engine manufacturing business with double-digit sales growth that is very profitable on a free cash flow basis.

Earnings Estimate (Yahoo Finance)

Why The Investment Thesis Could Be Challenged

The thesis is dependent, to a large extent, on ongoing momentum in the Aerospace segment which is, as I alluded to above, by far the biggest operating segment for General Electric in terms of sales contribution.

It is also the most promising, in my view, because of its double-digit sales growth. If this growth were to moderate, the Aerospace business on a standalone basis might attract a lower earnings and free cash flow multiple.

Furthermore, there can’t be any guarantees that the GE Vernova spin-off in 2Q-24 will increase interest in General Electric’s Aerospace business. Aerospace is also very cyclical, meaning General Electric, after the GE Vernova spin-off, could be viewed as having a much more vulnerable earnings profile.

My Conclusion

I missed the boat on General Electric last year, as I clarified in my coverage in October when I modified my stock classification to Hold.

After General Electric’s 4Q-23 earnings, however, I see the industrial conglomerate as a Buy due to the fact that

- The conglomerate’s Aerospace business is on fire, producing double digit sales and order growth; and

- The upcoming spin-off of the energy unit could recenter investors’ focus on the already robustly performing Aerospace division.

General Electric’s stock is not cheap for sure, and investors that seek a deep value industrial investment, may want to give 3M a shot which also just released quarterly earnings that were just as solid. With that being said, though, General Electric’s core business unit is seeing very robust fundamentals and it has a catalyst related to the energy spin-off coming up in the short-term as well.

Read the full article here

")

")

")

")