Q2 2025 Earnings Call Transcript")

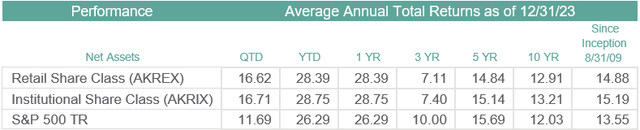

The fourth quarter offered a distinct final chapter to the shifting quarterly narratives of 2023. The “higher for longer” interest rate concerns of the third quarter gave way to optimism that the Federal Reserve is done raising interest rates and that the economy, having skirted the much- anticipated recession thus far, was more likely to achieve the dream scenario of a “soft landing.” Combine that with the Federal Reserve’s signaling of potential interest rate decreases in the back half of 2024, and it made for a heady holiday season. The S&P 500 finished the year with nine consecutive weeks of gains. Our Fund’s performance during the quarter proved even stronger, lifting performance for the year ahead of the S&P 500, despite not owning any of the “Magnificent 7” names so disproportionately responsible for the S&P 500’s advance.

The Akre Focus Fund’s fourth quarter 2023 performance for the Institutional share class was 16.71% compared with S&P 500 Total Return at 11.69%. Performance for the trailing 12-month period ending December 31, 2023 for the Institutional share class was 28.75% compared with S&P 500 Total Return at 26.29%.

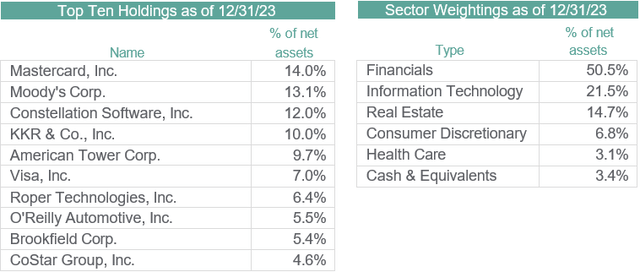

The top five positive contributors to performance during the quarter were Moody’s (MCO), KKR (KKR), American Tower (AMT), Constellation Software (OTCPK:CNSWF) and Mastercard (MA). Nothing notable to call out.

The only two negative detractors from performance this quarter were Lumine Group (OTCPK:LMGIF) and Veralto Group (VLTO). Veralto, a spinoff from Danaher (DHR), was sold in mid-October.

Cash and equivalents stood at 3.4% of the Fund’s net assets as of December 31 compared with 6.1% at the end of the third quarter.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Fund performance current to the most recent month-end may be lower or higher than the performance quoted, and can be obtained by calling 1-877-862-9556. The Fund’s annual operating expense (gross) for the Retail Class shares is 1.31% and 1.04% for the Institutional Class shares. The Fund imposes a 1.00% redemption fee on shares held less than 30 days. Performance data does not reflect the redemption fee, and if reflected, total returns would be reduced.

Mutual fund investing involves risk. Principal loss is possible. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. In addition to large- capitalization companies, the Fund invests in small- and medium- capitalization companies, which involve additional risks such as limited liquidity and greater volatility than larger capitalization companies.

Despite the positive results for the year on an absolute and relative basis, our goal as investors is to perform well over time—not all the time. The distinction is an important one because it speaks to what our investors should expect: (1) We will be periodically out of step with prevailing market fashions; (2) We will stick to our quality standards and valuation discipline even when faced with compelling new themes that capture the imagination of investors; and (3) We will continue to own what we believe are great businesses through inevitable periods in which their share prices drag on the Fund’s performance. In short, we will not abandon what works over time to chase what’s working at the time. That has, and will, lead to periods where our results trail those of the broader market. In our view and experience, this is a necessary ingredient to achieving above-average rates of compounding over the long term.

As we look to 2024, we remain agnostic as ever about market direction. Consider that just a year ago, the consensus market outlook for 2023 called for recession and a commensurately gloomy outlook for stocks as the necessary and logical outcome of interest rate tightening by the Federal Reserve. Clearly, the market had other ideas!

As we hope you have come to understand and expect, we do not invest on the basis of headlines, market prognostications, or geopolitics. As interesting as these can be, they are lousy guides when it comes to compounding capital. We focus instead on quality and value as the primary drivers of investment decisions. Whatever the new year has in store, business quality and value will remain our touchstones.

We wish you a wonderful winter, and thank you for your continued support.

The composition of the sector weightings and fund holdings are subject to change and are not recommendations to buy or sell any securities. Cash and Equivalents include asset backed bonds, corporate bonds, municipal bonds, investment purchased with cash proceeds for securities lending, and other assets in excess of liabilities.

The S&P 500 TR is a broad-based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general. It is not possible to invest directly in an index.

The Fund’s investment objectives, risks, charges, and expenses must be considered carefully before investing. The summary and statutory prospectus contains this and other important information about the investment company, and it may be obtained by calling (877) 862-9556 or visiting www.akrefund.com. Read it carefully before investing.

The Akre Focus Fund is distributed by Quasar Distributors, LLC.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here

Q2 2025 Earnings Call Transcript")

")