")

")

")

")

Momentum solves 80% of your problems. – John C. Maxwell

It has only been ten weeks since my last piece on ADMA Biologics, Inc. (NASDAQ:ADMA). However, there has been a cascade of good news around this intriguing small cap name over that time. The company is entering 2024 on a roll. The stock is up nearly 10% in the early stages of this year and more upside could be ahead. An updated analysis follows below.

Seeking Alpha

Company Overview:

This small biopharma concern is headquartered in New Jersey. ADMA Biologics manufactures and markets specialty plasma-derived biologics for the treatment of immune deficiencies and infectious diseases. With the rally in the shares since the end of October, the stock sells near the five buck a share level and sports an approximate market capitalization of $1.1 billion.

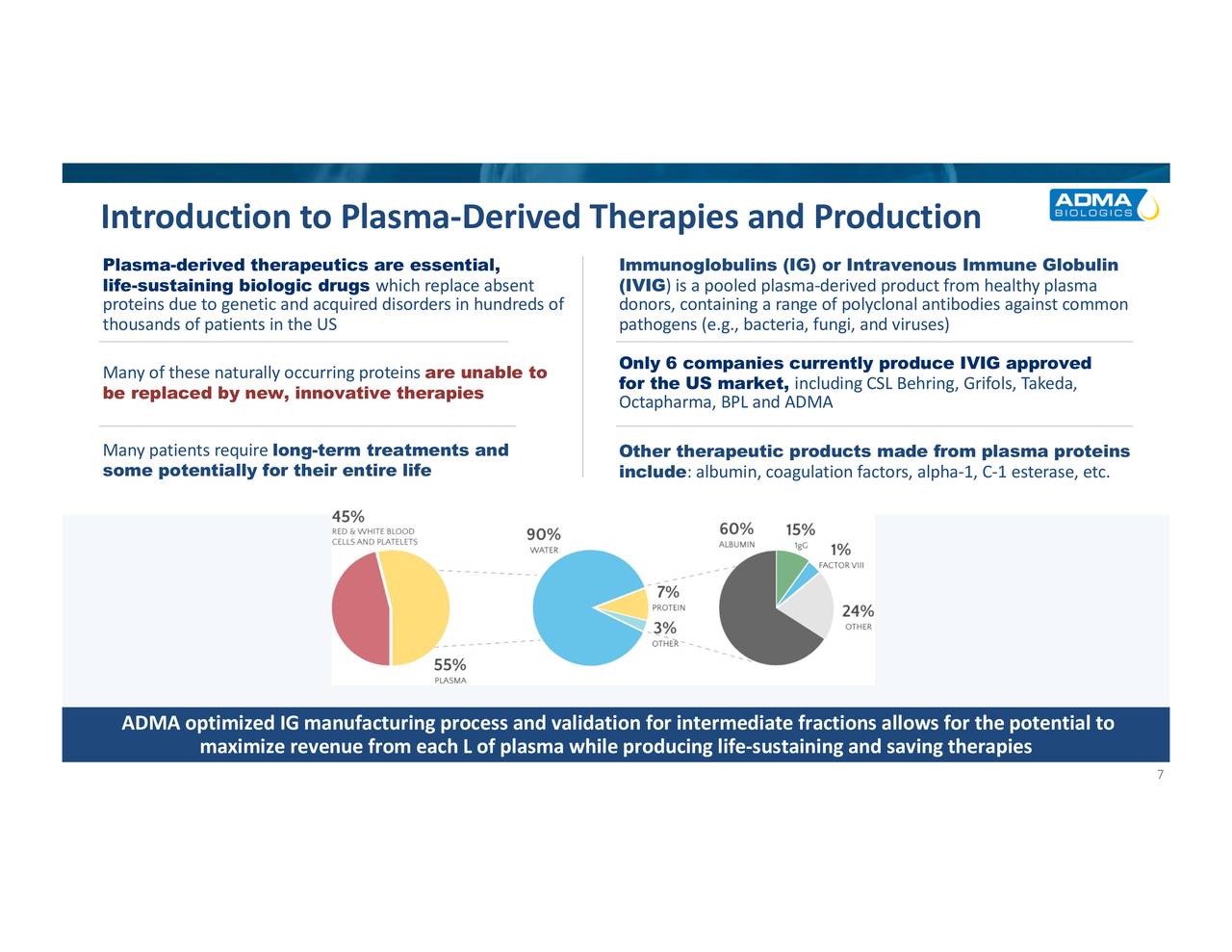

ADMA Company Presentation

The company has two key products on the market, both of which were approved by the FDA in 2019. The first is called BIVIGAM, which treats a condition called primary humoral immunodeficiency or PI. The second is ASCENIV™. This is an Intravenous Immune Globulin drug product that is approved to treat Primary Humoral Immunodeficiency Disease in adults and adolescents (12 to 17 years of age).

ADMA Company Presentation

Recent Developments:

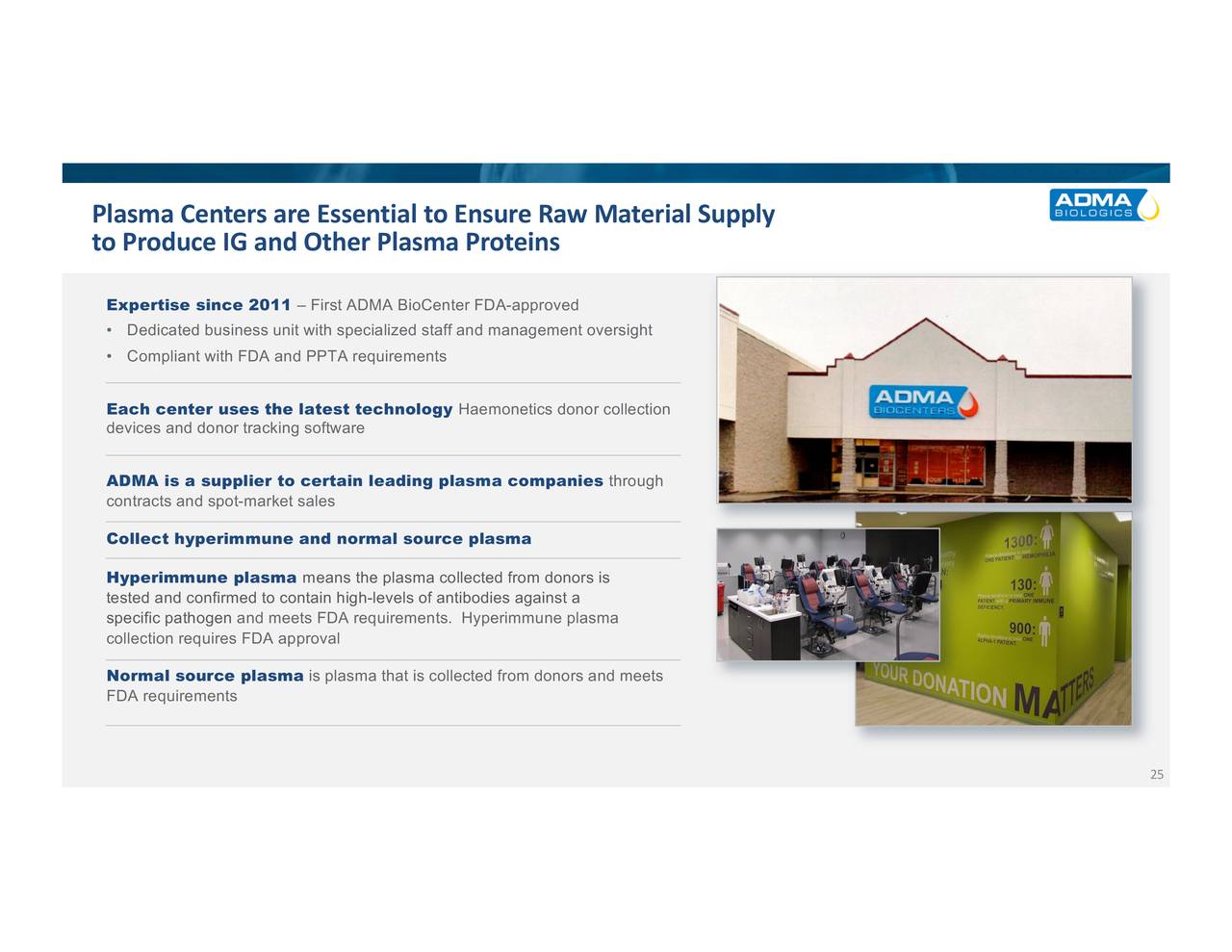

A week after my last article on ADMA, the FDA granted the company approval for its tenth plasma collection facility in Laurel, Maryland. It was the tenth of ten facilities management has committed to building out its network. On December 12th, the company was the recipient of another positive FDA action. This time the government agency gave the green light to Bivigam to treat primary humoral immunodeficiency in patients aged 2 years and older.

ADMA Company Presentation

Last week, management disclosed it now sees FY2023 revenue in the $256 million to $258 million. This is up from the $250 million figure, leadership provided with its third quarter results. Leadership also projects FY2024 net income being between $60 million to $110 million, up from its previous guidance of $55 million to $100 million.

Analyst Commentary & Balance Sheet:

Since ADMA Biologics posted solid Q3 numbers on November 8th, Cantor Fitzgerald ($6 price target), Mizuho Securities ($7 price target) and H.C. Wainwright ($6 price target) have all reiterated Buy ratings on the shares.

Approximately three percent of the outstanding float in the shares is currently held short. Two insiders bought just over $575,000 worth of shares collectively in late September of last year. That was the last insider activity in the stock. As of September 30th, ADMA Biologics had nearly $75 million in cash and marketable securities on its balance sheet. The company has just over $140 million of senior notes on its balance sheet as well.

On December 18th, the company announced it was replacing its current debt with a $135 million senior secured credit facility. According to management, this new credit arrangement ‘materially reduces ADMA’s nominal interest rate and significantly lowers their total debt by 15%‘

Verdict:

The company lost 33 cents a share in FY2022 on $154 million in revenue. The currently analyst firm consensus projects the company will close out FY2023 with a two penny a share loss on a surge of sales to $255 million. Next year they see 21 cents a share of profit on $308 million in revenue.

Management at ADMA Biologics is executing very well against its game plan. In the third quarter, the company posted $12 million in positive operating cash flow. This was the first time ADMA had done so on a quarterly basis in its history. With its plasma center network now complete, the company should be a growing and profitable enterprise in the years ahead.

As my late father like to quip ‘if it ain’t broke, don’t fix it‘. I have maintained a decent size stake in ADMA primarily via covered call holdings over the past couple of years. It has been a profitable trade over that time and will remain how I hold this stock in my portfolio.

Never confuse motion with action. – Benjamin Franklin

Read the full article here

")

")

")

(NASDAQ:NFLX)")

")