By Scott Glasser, Michael Kagan & Stephen Rigo, CFA

Among Animal Spirits, Monitoring Risks

Market Overview

The market roared in the third quarter, with the S&P 500 Index (SP500,SPX) rising 5.9%. It looks like the Fed stuck the soft landing and felt confident enough about inflation to cut rates by 0.5%. The index has now gained in seven of the past eight quarters, including advances in 10 of the past 11 months. The S&P 500’s advance of 22% year to date is the strongest three-quarter start to a calendar year since 1997 and the ninth best of all time. With a trailing 12-month return of 36% — the 95th percentile of one-year rolling returns since 1987 — it’s hard to describe this run as anything but superlative.

Real estate and utilities — sectors that traditionally benefit from lower interest rates — led the index in the quarter, rising 17% and 19%, respectively. The industrials sector also performed well, climbing 12%, driven by shares of construction and building products companies on hopes lower mortgage and financing rates would spur demand for renovations and new homes.

Energy shares were the worst-performing, meanwhile, on the heels of a 16% decline in the price of crude oil, which, at $68.17 per barrel, is the lowest it has been to end a quarter since March 2021. Information technology shares were a rare laggard as semiconductor stocks paused on a relative basis while software stocks struggled for footing as investors grow impatient about seeing these companies monetize their investments in generative AI.

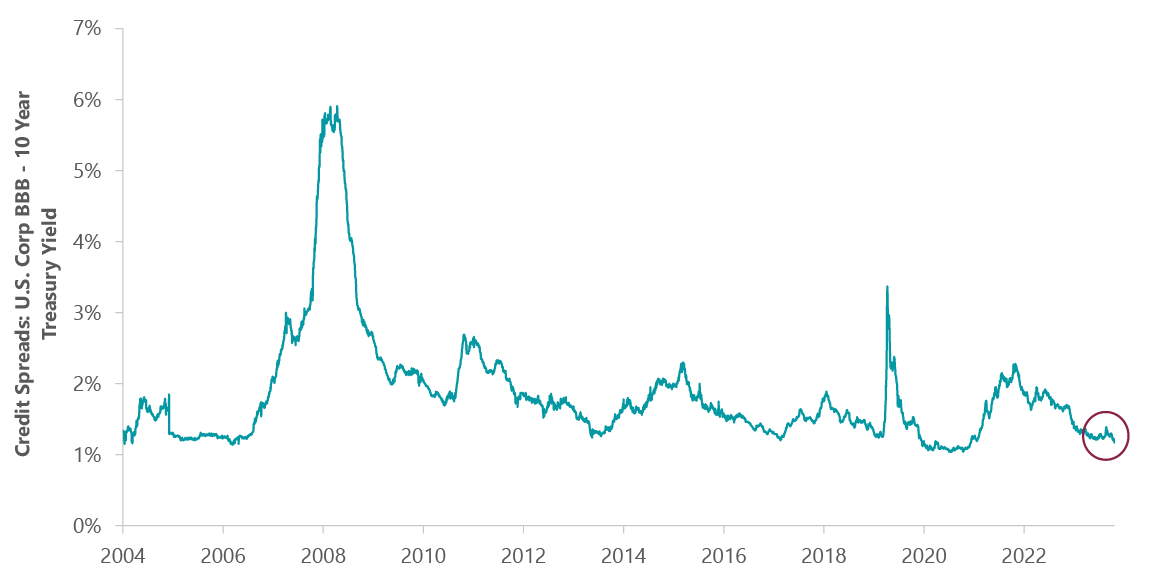

We follow measures of liquidity to assess the environment for risky assets and, at quarter end, liquidity has rarely been so plentiful. Credit spreads are within an earshot of all-time lows (Exhibit 1), while capital markets funding was wide open (corporate high yield issuance is +44% year to date). The yield curve is positively sloped for the first time in two years while lower interest rates have spurred a wave of mortgage refinancings, which are up over 100% from depressed 2023 levels. As risk-averse investors we had been incorrectly concerned that sustained high interest rates and the withdrawal of liquidity from a shrinking Fed balance sheet would tighten financial conditions. Today, with animal spirits vibrant, our focus is on monitoring risks that could alter the current favorable backdrop.

Exhibit 1: Liquidity Has Rarely Been So Plentiful

As of Sept. 30, 2024. Source: ClearBridge Investments, Bloomberg Finance.

Outlook

Although conditions today are clearly conducive for risk assets, we are at a key inflection point for investors, in our view. This is largely due to market expectations. First, investors expect the Fed will cut another 175-200 bps from interest rates over the coming 12 months, goosing what’s already fairly robust GDP growth of about 3%. Meeting this expectation will require a further moderation in inflation over the coming year, particularly in wages. Although many believe the labor market is weak, given a rise in the unemployment rate, much of the increase in unemployment can be attributed to an increasing labor force as job openings remain above pre-COVID levels. Moreover, at 4.2%, unemployment remains near a level considered full employment. Should labor prove tighter, the trend lower on wages will likely be bumpier than the market expects.

In addition, expectations for the impact of generative AI on economic growth remain sky high as cloud capex (data center construction, GPU procurement, and custom silicon investments) alone is expected to grow over 40% in 2024 to $218 billion. At some point investors will demand a return on investment on this capex, requiring companies to demonstrate more than just technology-related operating efficiency. Investors need to see applications beyond copilots to justify a continuation of the spend. Power supply also looks likely to constrain data center growth.

“As risk-conscious investors we believe when the sky is already blue it’s important to keep an eye out for storm clouds.”

That said, there are many anemic areas of the economy that could use a jolt from lower rates. Manufacturing has been in contraction for all but one month over the past two years; the Chicago Fed survey suggests that capital spending expectations over the coming 12 months continue to deteriorate; and housing remains unaffordable by historical standards. The all-important consumer appears to be struggling as spending remains muted while consumer loan delinquencies rise and underemployment trends higher.

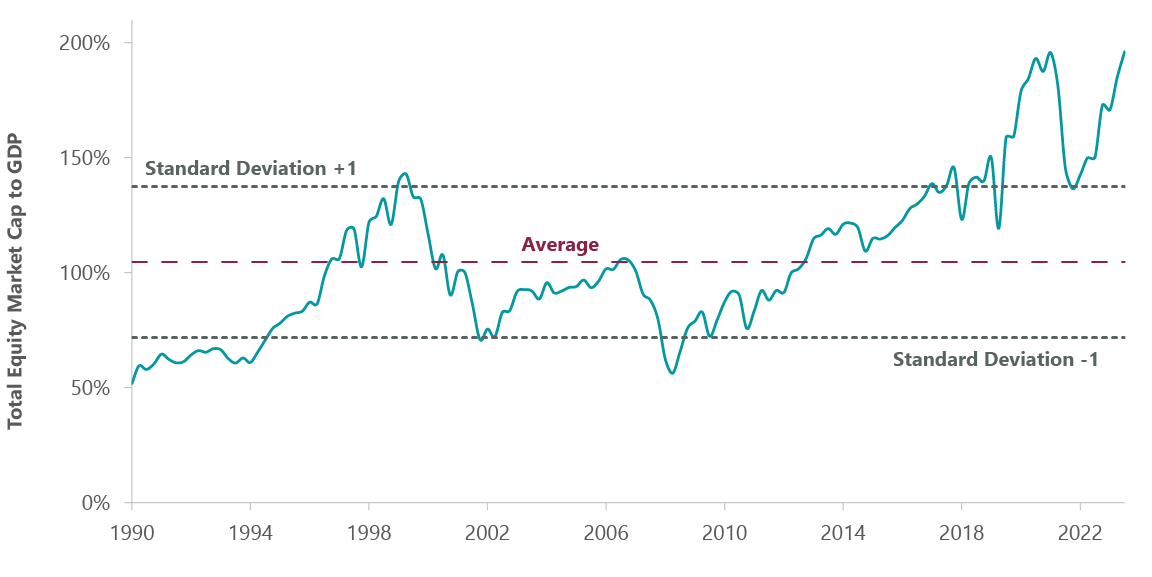

We would be remiss not to mention two other risks on our mind. The first is geopolitical. The impact from an escalation of the conflict in the Middle East could have wide-ranging implications on the global economy. We certainly hope for a peaceful resolution but, as of the publishing date, the risk of escalation looks high. Also, the uncertainty of the U.S. presidential election could cause business leaders to take a wait-and-see approach before investing in growth. The second is valuation. By almost any measure the stock market trades at highs last seen at the end of 2021. As example, the Buffett Ratio, which measures total equity market cap to GDP, stands at 196% (Exhibit 2). The last and only time total market cap to GDP stood at this level was December 2021 before the 2022 equity market downturn. While valuation is not a reason to trade, it does suggest to us there is elevated risk in the environment.

Exhibit 2: Buffet Ratio Suggests Valuations Are Extended

As of March 31, 2024. Source: ClearBridge Investments, Atlanta Fed, Bloomberg Finance.

In sum, the soft landing (or no landing) camp is currently in the driver’s seat. However, this is a “known known” driving the current risk-on environment and factored into today’s stock market expectations. We believe this dynamic has heightened the risk to the investment landscape should there be any stall in the disinflationary trend, disappointment in AI-driven capex or realization that the impact from rate cuts is more muted than past cycles. Our focus remains on whether: 1) corporate America monetizes its investment in AI enough to justify capital spending levels that support the valuations of AI-related stocks; 2) lower rates ease financial conditions and stoke the consumer into incremental spend; and 3) the deflationary force of technological advancement delivers disinflation supportive of further Fed rate cuts. As risk-conscious investors we believe when the sky is already blue it’s important to keep an eye out for storm clouds.

Longer-term, we worry about the sustainability of government debt and the burden of debt service on the budget deficit. At some point the U.S. will need to increase taxes and/or cut spending to prevent debt costs from spiraling out of control. Deficit spending at current levels cannot last forever. Both presidential candidates offer impractical budget plans that would greatly increase the deficit, an outlook that worries us further. Should investors require a greater risk premium (yield) to own a risk-free Treasury the next administration and Congress will face stark choices not in anyone’s current playbook. By no means is the U.S. dollar’s status as reserve currency our birthright.

While we are optimistic about the long-term benefits generative AI will have on workplace productivity, aggressive assumptions need to be made to justify current valuations for the direct hardware vendors. Software stocks have lagged this year, creating opportunities in companies that can successfully monetize generative AI. We admire the business models of the largest technology companies but are mindful of their regulatory and concentration risks they create for our portfolio. We are positive on select materials stocks such as construction aggregates where weather has disrupted near-term volume and lower rates could spur incremental demand. We believe select cyclical stocks have such low expectations that sustained economic growth could drive upside. Finally, we believe a steepening yield curve and relatively stable financial conditions will benefit select financial companies such as banks. We do not expect the top-heavy market to continue and believe a diversified portfolio with investments focused on durable growth at attractive valuations is best positioned in this transitioning interest rate regime.

Conclusion

Although we remain constructive on the medium-term outlook, we are mindful of high expectations and an expensive market. There are myriad risks to today’s placid environment, including the potential for escalation in the Middle East and the upcoming U.S. presidential election. We believe investors should anchor return expectations closer to longer-term trends (high-single digits annually) versus the current ebullient backdrop. There is value in many non-AI corners of the market, especially if Fed easing can reinvigorate more traditional sectors of our economy.

We are long-term investors focused on the risk-adjusted returns a diversified portfolio can deliver through a market cycle. Rather than trying to bet on near-term earnings trends, we believe it is better to look out two to three years and make investment decisions based upon our assessment of a company’s longer-term, sustainable growth rate relative to what is implied in today’s share price. .

Portfolio Highlights

The ClearBridge Appreciation Strategy underperformed the benchmark S&P 500 Index in the third quarter. On an absolute basis, the Strategy had positive contributions from 10 of 11 sectors. The financials sector was the main positive contributor to performance, while the energy sector was the sole detractor.

In relative terms, stock selection detracted while sector allocation was positive. Specifically, stock selection in the industrials and consumer discretionary sectors detracted the most, while an underweight to IT and stock selection in the consumer staples sector proved beneficial.

On an individual stock basis, the biggest contributors to absolute performance during the quarter were Apple (AAPL), Walmart (WMT), Berkshire Hathaway (BRK.A, BRK.B), Oracle (ORCL) and Meta Platforms (META). The biggest detractors were Alphabet (GOOG,GOOGL), Microsoft (MSFT), ASML, Merck (MRK) and Amazon.com (AMZN).

During the quarter, we initiated a new position in Broadcom (AVGO) in the IT sector and closed positions in Northrop Grumman (NOC) and United Parcel Service (UPS) in the industrials sector, ArcelorMittal (MT) in the materials sector and Home Depot (HD) in the consumer discretionary sector.

Scott Glasser, Chief Investment Officer, Portfolio Manager

Michael Kagan, Managing Director, Portfolio Manager

Stephen Rigo, CFA, Director, Portfolio Manager

|

Past performance is no guarantee of future results. Copyright © 2024 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance source: Internal. Benchmark source: Standard & Poor’s. |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here