")

Powell opens the dances, markets at ATH

In the third quarter, the global economy was shaped by easing monetary policies and evolving investor expectations. In August, a disappointing US jobs report and the Bank of Japan’s tightening measures led to a sharp market unwind, causing the VIX to spike to its highest levels since early COVID-19, a 20% drop in Japanese equities over three days, and a 75 basis points decline in the 2-year US treasury yield. Despite this upheaval, global equities rebounded strongly, reaching new highs in September. Disappointing US employment data was counterbalanced by other labour indicators, robust retail sales and earnings reports. A third consecutive surprise in lower headline inflation allowed Federal Reserve Chair Powell to adopt a dovish stance at Jackson Hole.

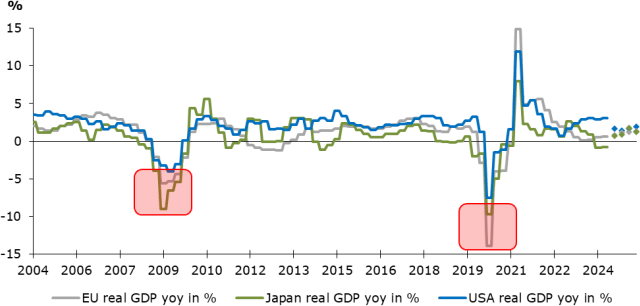

Chart 1: No shock wave, softer economic growth outlook

Source: Alpinum Investment Management

The US economy slowed, increasing the risk for a mild recession in 2025. Inflation eased in the US and Europe, though Europe struggled with services inflation. Central banks, including the Fed, ECB, SNB, BoC, BoE and PBoC cut rates, while Japan maintained its reflationary stance. China faced weak demand and declining profitability. (US-) Equity market valuations remained elevated, with defensive sectors and high-quality fixed-income assets well-positioned to weather potential market corrections amid easing monetary policies and the upcoming US elections.

United States

The US economy maintained strong momentum, with real GDP growing by 3.1% in Q2, largely driven by robust government spending and continued business investment, marking 14 consecutive quarters of expansion. The labour market is normalizing to pre-COVID trends, with payroll gains averaging 202,000 and the unemployment rate rising to 4.2%. Despite this rise, indicators like job openings and the participation rate remain near 2019 levels, signalling a resilient labour market. Inflation is moderating, though services-related inflation, particularly in insurance, remains a challenge. While shelter inflation is easing, inflation is expected to stay above the Fed’s 2% target for the remainder of the year, leading to a cautious approach to rate cuts. Equity markets reflect elevated valuations, with the S&P 500 forward P/E ratio at ~21x, suggesting lower forward returns. Market concentration remained a significant risk in Q3, even though nearly 70% of S&P 500 stocks outperformed the index, reversing Q2’s trend where fewer than a quarter did so. Despite this broader outperformance, the market’s heavy reliance on a few large-cap stocks increases vulnerability to potential negative fundamental surprises.

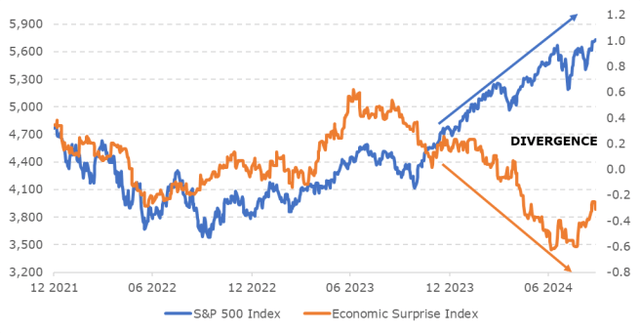

Chart 2: Economic surprises diverging from equity markets

Source: Alpinum Investment Management

Despite overall optimism, recent economic data have shown downside surprises, signalling potential vulnerabilities in the market. The Federal Reserve initiated its easing rate-cut cycle with a bang of 50 bps reduction at the September 18 FOMC meeting, with markets pricing in up to eight cuts through 2025, lowering the Fed funds rate to 2.9%. Uncertainty surrounding the presidential election is contributing to heightened volatility, a trend typical during election years. While the economy remains resilient, slowing growth and persistent inflation create a more cautious outlook for the remainder of the year, with investor complacency towards downside risks growing.

Europe

Europe’s economic outlook displayed a cautiously optimistic yet mixed trajectory. Major economies such as Germany and France showed resilience, though overall growth remained subdued. Consumer confidence fluctuated, reflecting both improvements and concerns over rising living costs and economic uncertainty. The Composite Purchasing Managers’ Index (PMI) rose to 50.9 in August, up from 50.1 in July, reflecting the fastest growth in three months, driven by stronger expansion in the services sector (52.9), while manufacturing stagnated at 46.0, underscoring ongoing difficulties in the industrial sector. The labour market remained stable, with the Eurozone unemployment rate declining to a record low of 6.6% in July. Inflation moderated during the quarter, with the headline rate easing to 2.2% in August from 2.6% in July, marking the softest increase since July 2021. This decline was largely attributed to a sharp drop in energy prices (-3.0%), though inflation for services (4.2%) and food (2.4%) remained elevated. Core inflation, excluding energy and unprocessed food, remained steady at 2.8%, indicating persistent inflationary pressures in non-energy sectors.

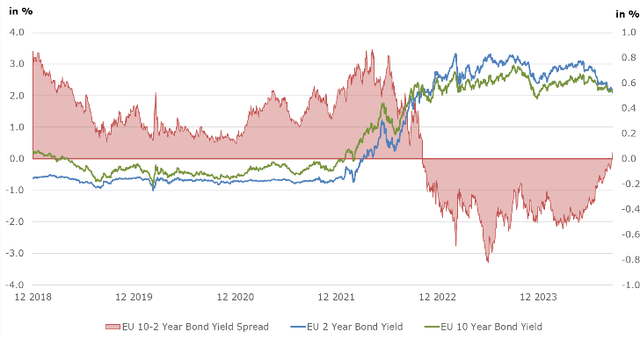

Chart 3: Gradual normalization of the eurozone yield curve

Source: Alpinum Investment Management

In response to moderating inflation, the European Central Bank (ECB) cut its deposit rate by 25 basis points to 3.50% in September, following a similar cut in June. Market expectations point to further rate cuts before year-end, reflecting the ECB’s continued efforts to balance growth with inflation control. Equity markets in Europe experienced volatility during the quarter. The Euro Stoxx 50 saw sharp declines beginning of August, followed by a rebound in the second half of the month, driven by positive economic data and anticipated monetary easing. Government bonds saw increased demand as investors sought safe-haven assets, while the yield curve began to normalize.

China and emerging markets

Despite some cautious optimism, China’s economic landscape faced ongoing challenges. GDP growth decelerated to 4.7% year-over-year in Q2, down from 5.3% in Q1 and falling short of the 5.1% forecast. This slowdown reflects ongoing struggles in the property sector, weak domestic demand and ongoing trade frictions. The Caixin China General Manufacturing PMI improved slightly to 50.4 in August from 49.8 in July, signalling a modest expansion in manufacturing as new orders increased. However, foreign demand fell for the first time this year, indicating some external pressure. In August, China’s CPI and PPI both fell short of expectations, reflecting worsening deflation pressures. CPI rose 0.6% year-over-year, below the forecasted 0.7%, while core CPI growth slowed to 0.3%. PPI fell -1.8%, exceeding the anticipated -1.5% decline, underscoring weak domestic demand and producers’ difficulties in passing on costs. The labour market remained stable but exhibited signs of strain, as the unemployment rate increased to 5.3% in August, up from 5.2% in July and 5.0% in June.

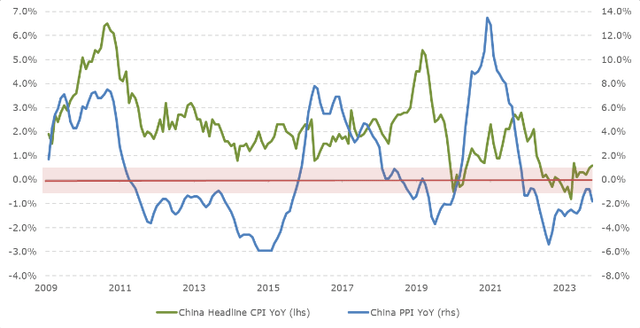

Chart 4: Deflationary headwinds intensify in China

Source: Alpinum Investment Management

The People’s Bank of China held the one-year and five-year loan prime rates at 3.35% and 3.85%, respectively, after recent rate cuts. It also reduced the seven-day reverse repo rate to 1.5% and injected CNY 234.6 billion into the banking system to boost economic support. The yuan appreciated from 7.27 to approximately 7.01 per dollar, reflecting a weakening US dollar. The CSI 300 index fell 8.7% during the quarter but quickly regained losses in just over a week, driven by PBoC policy stimulus. The property market continued to struggle, with new home prices dropping by 5.3% year-over-year in August.

Investment conclusions

The initial August market slump has been quickly reversed, though concerns persist about a potential economic downturn. While a mild slowdown is likely, a severe recession is not on the cards. The anticipated easing of monetary policies and a weakening USD will contribute to a normalization of the yield curve and a subsequent economic recovery. However, this may limit the upside potential for equity markets, which are already priced at relatively high valuations. Despite potential volatility, the overall outlook for the market remains neutral. The current environment favours active portfolio management across asset classes and supports credit markets, although selective credit risk remains a concern.

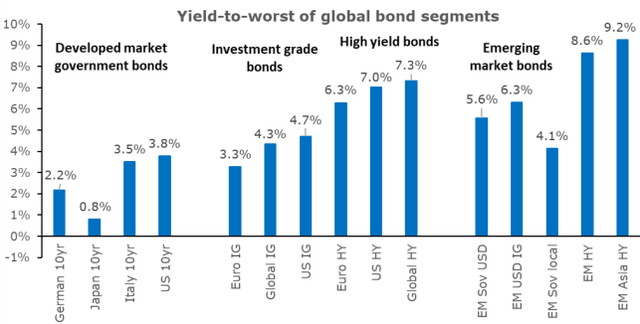

Chart 5: Yield-to-worst of global bond segments

Source: Alpinum Investment Management

Bonds: The global shift towards looser monetary policies, excluding Japan, contrasts with commercial banks’ continued tightening of credit conditions, hindering corporate borrowing. While default rates have risen slightly, selective credit opportunities remain.

Equities: Equity valuations seem reasonable considering lower interest rates and moderate growth prospects. Limited upside potential exists, particularly for large US equities with high valuations.

A blended investment style is advised, as we maintain a positive outlook for US treasuries and short-term high-yield bonds, and a neutral outlook for equities. In the credit market, we anticipate a modest increase in default rates, leading to slightly elevated levels. However, we consider current credit spreads to be relatively tight, but still aligned with the broader economic outlook, providing a reasonable risk-reward profile for investors.

Read the full article here

")

")