")

Main Thesis/Background

The purpose of this article is to evaluate the Nuveen California Quality Municipal Income Fund (NYSE:NAC) as an investment option at its current market price. This is a closed-end fund whose objective is to “seek current income exempt from both regular federal income taxes and California personal income tax; its secondary investment objective is the enhancement of portfolio value”.

I cover the California muni sector often, and that includes reviews on NAC. The last time I wrote about this fund was back in June, when I saw quite a bit of inherent value. I thought the muni sector was due for a comeback and NAC was a smart way to play it – and I sure was right in hindsight:

Fund Performance (Seeking Alpha)

Victory lap aside, I think this rapid push higher should give investors some pause. Yes, momentum plays can continue for a while, but when I see fixed-income CEFs generating equity-like returns in a short period, I need to at least reflect on the likelihood of this continuing.

In the case of NAC, I think some tempering of expectations is in order. The fund’s discount to NAV has narrowed because of the move higher, and I also think the rush into bonds as a whole will slow as the Fed disappoints on rate cutting in the months ahead. For these reasons, I think investors should approach new positions a bit more carefully and a downgrade to “hold” for NAC is justifiable going forward. I will explain the rationale in more detail below.

Discount To NAV Has Narrowed

I want to be clear from the onset that I am not bearish on this fund. I still have a generally favorable view of munis as a whole, and I think NAC will hold up reasonably well going into 2025. But I think the key element of this review is to emphasize that the opportunity to get into bonds – including munis – is starting to get inherently more limited. Investors have been rushing into the sector as a whole to front-run interest rate cuts from the Federal Reserve. This has been a nice tailwind for income investors and helps explain why NAC has performed so well over the last quarter. The gain was strong and justified, and that is what investors want to see.

But I am concerned that people who are buying in now may have too high of expectations, and that is what I want to manage. Can NAC, and similar funds, continue to move higher? Absolutely. But I wouldn’t expect a repeat of what we have seen very recently, and that is why I am downgrading my view.

One of the central reasons behind this premise is that NAC’s valuation has gotten a bit less attractive. To be fair, it still sports a reasonable discount to NAV, and that could draw in some value-oriented buyers. But at 7% currently, that is noticeably narrower than the discount above 10% that I saw back in June:

NAC: Quick Stats (Nuveen)

Now I am not going to sit here and say that NAC is over-priced. The fund’s discount is still wide and it could represent value. But I am making the point that it was cheaper three months ago and about half its total return since my last review was due to discount narrowing. This suggests less value than when I last recommended it and helps to justify my downgrade to “hold”.

Income Boost Was Nice, But Likely Not Sustainable

My next topic is a bit of a twist on an attribute I talked about in my last article. This was the fund’s hike to its distribution, which readers will recall was something I presented as a bullish factor. Simply put, the fund manager (Nuveen) embarked on an income hike program for many of its muni CEFs in an effort to stir-up interest in the funds and ultimately narrow the ever-present discounts to NAV those funds traded at. This is not my speculation on their motive, it was clearly spelled out in the company’s press release prior to doing the increases back in June of this year.

The takeaway was that I saw the potential for an increase in buying by retail investors, who were encouraged by the higher yields. This has certainly turned out to be the case. NAC – and other funds that were included in this program – have been performing quite well, and the distributions have thus far been either sustained or increased again. This could be looked at as a win-win for investors and justified my prior “buy” call.

While I still believe some investors could be attracted to these higher payouts, we have to remember that these yields are likely not sustainable for the long term. The fact is that Nuveen’s attempt to bring in money has succeeded, but the management teams have been dipping into the CEFs capital in order to pay these higher amounts. Essentially, the funds are returning capital to shareholders in order to maintain these payouts, rather than increasing net investment income to cover it. While some may not care about this if they are focusing solely on the yield itself (and not the underlying reason behind how the current yield is being paid) they will care once they realize that sustainability of a yield is just as important as the numerical value of it.

This is important because for NAC, the return of capital (ROC) metric is quite substantial. This means without something fundamentally changing for the fund, the current level will eventually have to be cut to more properly align itself to what the fund is actually bringing in through investment income:

NAC’s ROC Figure (Nuveen)

I am not trying to be alarmist here and suggest readers need to run for the hills. But I am trying to be realistic. NAC has seen a great bump in price, and part of that has been due to its higher distribution level. But that distribution will not be sustainable forever, and that puts the fund at risk of a correction when it inevitably gets cut. That may not happen for a long time – some funds sustain payouts with ROC for years. But it is something investors in the fund need to watch closely and be prepared for. Given that NAC has already benefited a great deal from the hike, I would caution that upside from this metric alone will be limited going forward.

Analysts Still Bullish On California

While I am concerned about NAC’s valuation and distribution going forward, the story is not all bad. This is central to why I see merit to owning/holding this CEF going forward, and why I don’t see a compelling argument to be too negative on this fund. Importantly, my concerns about NAC don’t extend to the bulk of the underlying securities in the portfolio. This is because California – despite many negative headlines – has enough cash to pay its debts.

While I will not deny that structural changes need to be made in that state, the short-term outlook is fine in my view and shared by the ratings agencies:

Fitch’s Outlook (Fitch Ratings)

This gives me confidence in the fund more broadly and supports why I continue to make the argument that California muni bonds could be a strong core holding for residents of that state.

Remember This Sector Is For High Earners Primarily

I have laid out a few reasons why I still like munis as a whole (and from California) and why there are a couple attributes about NAC that give me some pause at the moment. But now I want to shift the focus to a reminder on who muni bonds are most appropriate for. What I mean is, who benefits the most from owning this type of security in their portfolio?

To me, this asset class is most appropriate for high-income earners, or those who have a high amount of taxable income. The reason is two-fold. One, the more of your income that is taxable, the more you benefit from shielding some of that income from Uncle Sam. By contrast, if you have a low amount (or none) of taxable income, then the benefit of owning tax-exempt securities is limited by design.

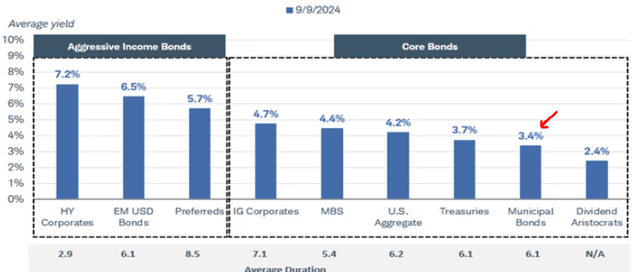

Two, the muni sector has a yield right now that is less competitive than most other fixed-income sectors. This means investors really need to be capturing a much higher tax-equivalent yield in order for this idea to be competitive:

Current Yields (By Sector) (Charles Schwab)

This second point really expands on the first one. If one is not earning a lot of money and/or is in a higher tax bracket, then the income derived from this sector will likely be less than what they could earn from rating-equivalent bonds in corporate or mortgage debt. This doesn’t make munis “bad”, but it does reiterate that readers should understand their own unique situation when evaluating whether or not this sector (whether through NAC or any other fund) is the best play for them to earn yield.

Bottom-line

NAC has really delivered since mid-June, and that has been a welcome development for shareholders. While I was bullish on this fund and expected to see gains, the sharpness of the recent increase in such a short time period gives me some pause. While I think more gains could be possible, the narrowing of the fund’s discount to NAV and high level of ROC to pay its distribution tells me that the “easy” money has probably been made already.

This means that I would urge my followers to be selective with new positions going forward and to verify this asset class (munis) is the best fit for them based on their income and level of taxation. As a result, I see the downgrade to “hold” as the right move for NAC at this time.

Read the full article here

")

")