(NASDAQ:META)")

")

")

")

Investing in basic materials companies requires a very different approach to other segments of the equity market. As opposed to most cyclical stocks, companies operating in the agricultural space are exposed to much longer cycles in prices of the underlying commodities.

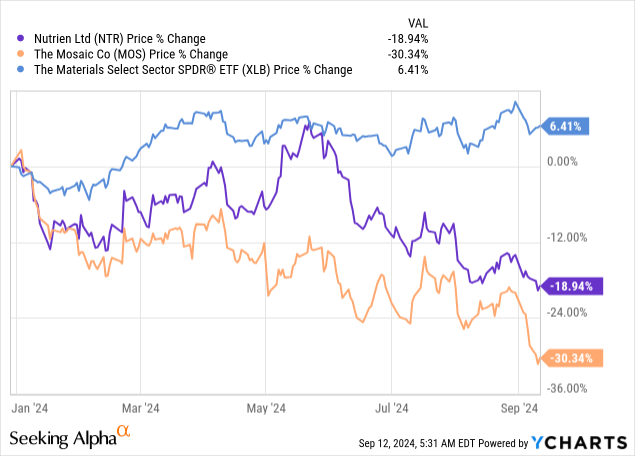

That is why, it is so important for investors in Nutrien Ltd. (NYSE:NTR) not to be swayed by short-term oriented analysts and market commentators. The reason why I am saying that is because NTR has been an utter disaster for shareholders since the beginning of 2024 and most market observes would have a hard time recommending a stock that is down nearly 20% year-to-date.

As we could see from the graph above, the basic materials sector (XLB) has not been a good spot either, even though the ETF is up by more than 6% during the same period. Nutrien’s major peer, however, Mosaic (MOS) is down by more than 30% since January which highlights the state of the fertilizer market at the moment.

I went through the sector related risks back in November of last year and then reiterated my long-term view on the stock in July when I showed why we could soon see a reversal of the stock’s downtrend. In spite of all that I kept a hold rating on NTR over this period due to the very strong industry-wide headwinds. As these trends continue, however, NTR has now become too cheaply priced and for the reasons that I outline below is also in buy territory for long-term investors.

Rock Bottom

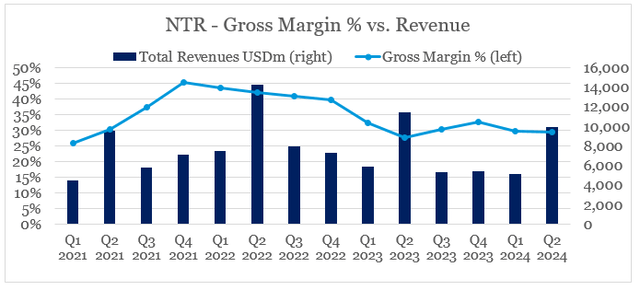

NTR stock reached an all-time high in early 2022 when commodity prices skyrocketed and fertilizer pricing drove record sales and margins for the company. Since then, however, we have seen a gradual decline in sales and gross margins reached a rock bottom over the past year or so.

From a seasonal point of view, the second quarter of each fiscal year is the most important when most revenue is realized. Unfortunately, as we could see below Q2 2024 sales were down roughly 13% from a year ago and Q2 2023 sales were 20% lower to Q2 2022.

prepared by the author, using data from Seeking Alpha

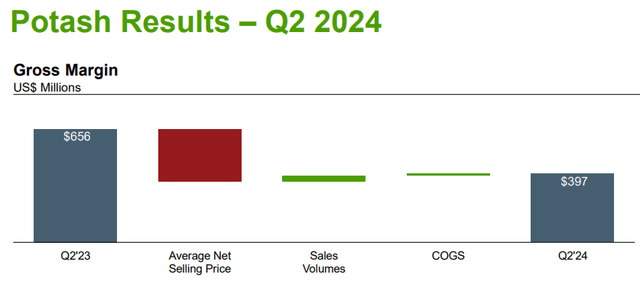

The good news is that volumes have stabilized somehow, as selling prices continued to put downward pressure on margins.

Nutrien Investor Presentation

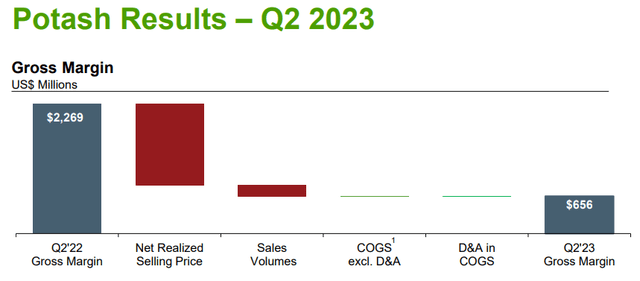

We could contrast these results to the Q2 2023 ones when the negative impact of net realized selling price was much larger and volumes contracted – thus having a double whammy effect on margins.

Nutrien Investor Presentation

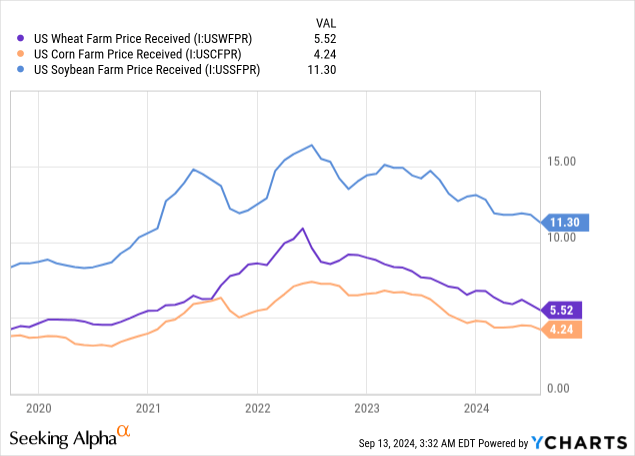

This is hardly a surprise as agricultural commodities fell sharply from their 2022 highs and have been on a gradual decline since then.

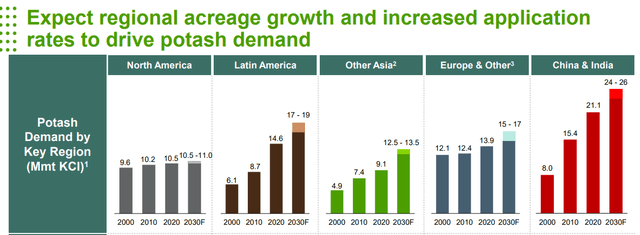

As agricultural commodity prices are still on a downward trend and fertilizer pricing is likely to remain a headwind in 2024, Potash demand in Latin America, Europe and China is expected to grow meaningfully over the next 5 years.

Nutrien Investor Presentation

This creates significant imbalances within the fertilizer industry from a supply-demand point of view. Canada, Russia, China and Belarus are by far the largest producers which makes certain regions heavily dependent on imports. In that regard, NTR is well-positioned to continue to expand in South America while being well-established in North America.

Although the latter region is not expected to grow as much and Nutrien sales fell precipitously in the U.S. over the past year, the company has significant competitive advantage derived from its geographical footprint in the region. Lower natural gas pricing in North America is also highly beneficial for the company’s fertilizer production in the region.

Priced Too Conservatively

While sales and margins would recover sooner or later as smaller and high cost producers either go out of business or reduce their supply, the main question for NTR shareholders is what the downside risk is, if the current pricing environment remains for a prolonged period of time.

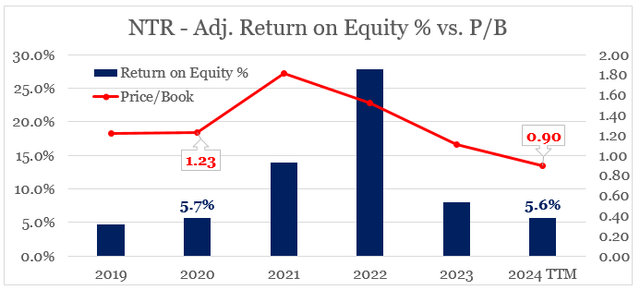

For the past 12-month period, NTR’s return on equity (adjusted of intangible asset impairments) stands at 5.6% which is not viable for the company’s survival in the long-run. The stock, however is priced at record-low levels with the price to book ratio of only 0.9.

prepared by the author, using data from Seeking Alpha and SEC Filins

The current P/B multiple of below 1 suggests that the market is assuming that NTR’s ROE would remain below the company’s cost of equity, which depending on one’s assumptions should be around 8.5% to 9% and appears to be within reach. Moreover, the company is priced at a significant discount to fiscal year 2020, when adjusted ROE was at similar levels.

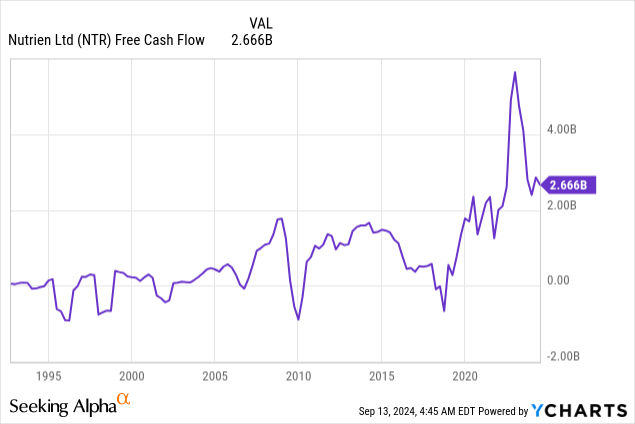

The company’s finance costs stand at around $760m for the past 12-month period and the annual dividend payments are roughly $1.1bn. When taken together and compared against NTR’s free cash flow of almost $2.7bn, we see that there isn’t any immediate risk for the company.

Nutrien’s management has also provided a similar picture during the last conference call which includes capital expenditures in excess of the level needed to sustain operations. Furthermore, management appears confident that the share buyback program could be restarted in 2025.

So, we have a very targeted and I would say, exciting program on the investing side that, along with sustaining CapEx, adds up to that $2.2 billion to $2.3 billion.

As you say, we’ve got about $450 million in leases and then about $1 billion for the dividend. So, that all adds up to about $3.7 billion. And as we watch the year unfold and as we head into the fall here and into 2025, as you say, as we look at incremental cash above those levels, certainly, we will look at buying back our shares, among other opportunities, which could include ongoing retail tuck-in opportunities in North America and Australia, and maintaining the flexibility for those when they come up, but also, as you say, share repurchases.

Source: NTR Q2 2024 Earnings Transcript

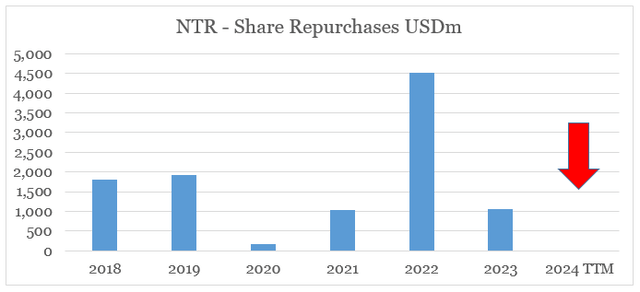

Over the past 12-month period, NTR did not buyback any shares as management looks to conserve cash and increase investments. On one hand, this move is prudent as future fertilizer prices are uncertain and the company should be prepared for the worst case scenario. On the other hand, however, this is not optimal as NTR stock now trades at record low levels and buying back shares is now highly accretive for long-term shareholders.

prepared by the author, using data from SEC Filings

Conclusion

Nutrien’s share price continued falling over the course of 2024 with the stock down by nearly 20% year-to-date. Even though the current environment does not allow for a different outcome, the assumptions currently built-in the share price are unlikely to persist beyond the near-term. Volatility in the short-term is to be expected, but for anyone with a long investment horizon the share price is now in a buy territory.

Read the full article here

(NASDAQ:META)")

")

")

ECTRIMS 2024 Investor Science Call Transcript")