(NASDAQ:META)")

")

")

")

Since I initiated a ‘Buy’ rating on Tractor Supply (NASDAQ:TSCO) in March 2015, the stock price has surged by more than 270%, significantly outperforming the S&P 500 Index (SPX). In my initiation report, I highlighted Tractor Supply’s strong same store sales driven by their pricing power and growth in rural lifestyle products. I remain confident that Tractor Supply will recover their same store sales growth in the near future. I reiterate a ‘Buy’ rating with a one-year target price of $310 per share.

Acquisition of Orscheln Farm and Home

In February 2021, Tractor Supply announced to acquire Orscheln Farm and Home for $320 million. I favor the acquisition for the following reasons:

- Orscheln Farm and Home is a farm and ranch retailer with 167 stores located in 11 states. Orscheln’s core business closely aligns with Tractor Supply, and the deal could enhance Tractor Supply’s presence in the Midwest. Orscheln is a family-owned business with strong customers relationship. Orscheln’s high customer loyalty reduces the risk of business integration.

- During the integration of Orscheln, Tractor Supply successfully incorporated key supply chain and IT systems, strengthening its supply chain for farm and ranch-related product categories.

- Lastly, the acquisition helped Tractor Supply eliminate a regional competitor, positioning Tractor Supply as a leading retailer in the rural lifestyle market.

Organic Growth & Store Growth

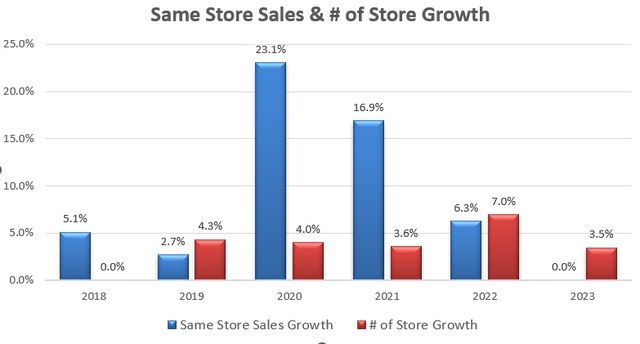

As depicted in the chart below, Tractor Supply experienced strong growth during the global pandemic period, then the same store sales growth started to normalize afterward. Due to the high-interest rate, consumer sentiment is quite weak in 2024. During the latest earnings call, the management indicated the weak consumption across different income levels. I think the weak consumer market make senses as other major retailers, such as Walmart (WMT), Dollar General (DG) and Home Depot (HD), also experienced similar patterns of weak consumer consumption.

Tractor Supply 10Ks

Tractor Supply continues to open new stores, with 3.5% year-over-year growth in FY23. The company operates 2,459 stores at the end of Q2 FY24. Walmart has more than 4,600 stores in the U.S. market. As such, I think Tractor Supply has a long way for their store growth in the future.

Recent Result and Outlook

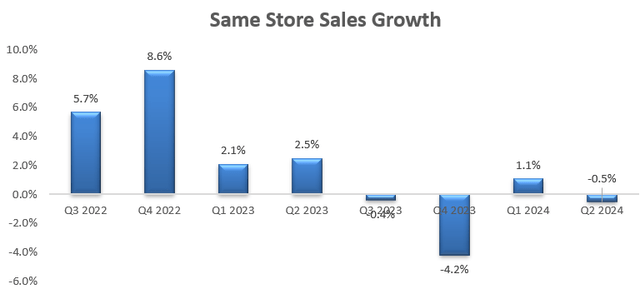

Tractor Supply releases its Q2 FY24 result on July 25th, reporting 0.5% decline in the same store sales due to the weak consumption sentiment as discussed previously.

Tractor Supply Quarterly Results

My biggest takeaway is the company’s ongoing efforts with their Neighbor’s Club loyalty program. As communicated over the earnings call, 15% of members are new to Tractor Supply, and the Neighbor’s Club comparable sales outpaced the overall sales growth. The company has more than 36 million loyalty members, having added 5 million over the past 12 months. The strong growth in their loyalty members indicates that Tractor Supply has successfully engaged with their customers, recognized and awarded their best customers, and driven store traffics from these members.

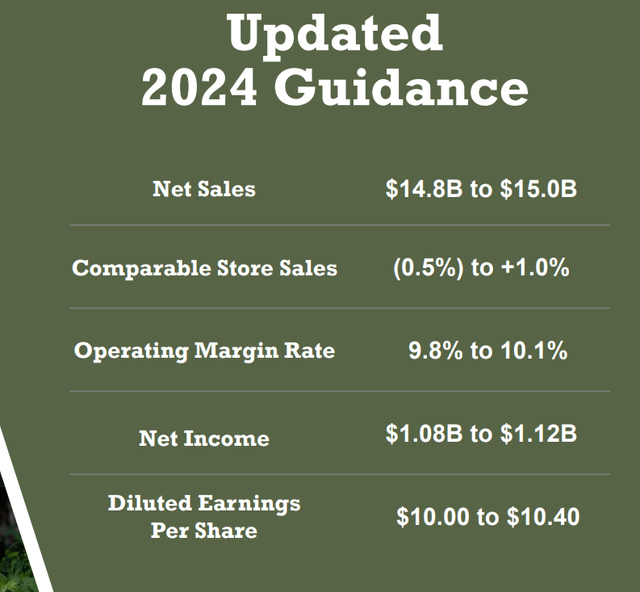

Due to the weak economy, Tractor Supply guided for -0.5% to 1% same store sales growth for FY24, as detailed in the slide below.

Tractor Supply Quarterly Results

For the growth from FY25 onwards, I break down the growth into same store sales and new store contributions as follows:

- Same Store Sales Growth: Livestock, Equine & Agriculture and Companion Animal account for more than 50% of total store revenues. Historically, livestock and companion animals have grown by mid-single-digit and double digit, respectively. The livestock growth is quite stable driven by pricing growth and moderate volume growth. As more young people prefer raising pets at home, the demand for companion animals has been quite strong in recent years, especially during the global pandemic period. I estimate Livestock, Equine & Agriculture and Companion Animal could drive 4% same store sales growth for Tractor Supply. Seasonal & Recreation, Truck, Tool, & Hardware and other product categories make up half of total revenue. I estimate these categories will contribute an additional of 2% to the same store sales growth.

- New Store Opening: As discussed previously, I think Tractor Supply has significant potential for store growth. I calculate the new stores could contribute 2% to the overall sales growth.

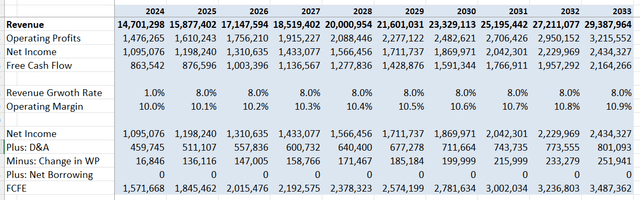

DCF Valuation

As discussed above, I estimate Tractor Supply will generate 8% total revenue growth in the near future. I model 10bps margin expansion primary coming from the operating leverage from SG&A expenses. As a retailer, it is challenging to achieve significant margin expansion, as customers are highly sensitive to product pricing. The best way for retailers to expand margin is to optimize their back office and supply chain, and improve productivities.

With these assumptions, the DCF and cash flow from equity (FCFE) can be summarized as follows:

Tractor Supply DCF

The cost of equity is calculated to be 9% assuming: risk-free rate 3.6%; beta 0.78; equity risk premium 7%. Discounting all the future FCFE, the one-year target price is calculated to be $310 per share, as per my estimates.

Downside Risks

During the quarter, Tractor Supply experienced weakness in discretionary product categories including clothing, footwear, décor and hardline products. I think as consumers are facing challenges with their cash flow, it is quite reasonable for customers to reduce spending on discretionary items.

In addition, Tractor Supply exited the quarter with $3 billion in merchandise inventory, reflecting a 10.2% growth. The company has been stocking their big-ticket products, as their stores experienced strength in these products. However, a weaker than expected consumption could potentially lead to working capital issues due to the increased inventory levels.

End Note

I view Tractor Supply as a unique retailer in the rural lifestyle market with no nationwide competitors. I think their growth will recover once the U.S. economy entering an interest rate cut cycle. I reiterate a ‘Buy’ rating with a one-year target price of $310 per share.

Read the full article here

(NASDAQ:META)")

")

")

ECTRIMS 2024 Investor Science Call Transcript")