(NASDAQ:META)")

")

")

")

Aurora Innovation (NASDAQ:AUR) is a developer of autonomous driving technology for trucks. The company is initially focused on highway miles, operating between distribution centers in metro areas, which avoids much of the complexity of urban driver. Aurora plans on commercializing its technology in the next year with an autonomous service from Dallas to Houston. It then plans on launching additional routes in Texas, before expanding more broadly across the Sunbelt over the next few years. While Aurora’s service should be cost competitive early on, particularly as support costs decline, the real benefit of autonomous trucking is on longer routes (>600 miles), where restrictions on driver hours come into play.

Aurora is taking an asset light approach, leveraging the capabilities of Continental and Truck OEMs on the manufacturing and installation side. The company also has strong partners like Ryder, FedEx and Uber Freight that will help with commercialization.

While Aurora is a leader in the space, along with companies like Kodiak and Torc, its market capitalization already prices in considerable success. Aurora’s valuation also appears high when compared to other leading companies in the autonomous vehicle space (Waymo, Cruise, Baidu).

This probably won’t matter in the short term, but it will take time for Aurora’s revenue to scale, and cash burn will remain elevated in the meantime. As a result, Aurora’s cash balance is likely to run out in the next 2 years. The company’s large market capitalization affords it flexibility in respect to financing, though.

I expect Aurora’s investor appeal to wane after the commercial service is launched and investors are faced with the realities of trying to scale a business with physical operations. Particularly given that economic data continues to weaken and freight demand could eventually be hit by this.

Market

Trucking is the main method of transporting inland freight in the US and a 1 trillion USD industry. While the market is only expanding at a modest rate, labor shortages are expected to become a problem in coming years due to an ageing workforce. There is currently an estimated shortage of around 50,000 drivers, which is expected to exceed 160,000 by 2030. These driver shortages are an important contributor to rising transportation costs. Autonomous trucking is a potential solution to this labor shortage, even if human drivers are still be needed for the foreseeable future to operate trucks on the first and last miles of routes.

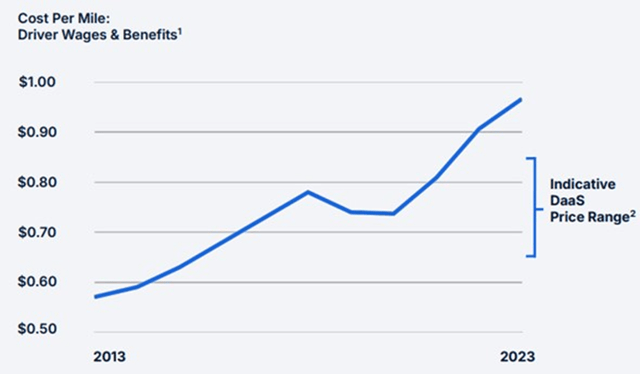

Trucking currently costs around 2.27 USD per mile, with labor, fuel and equipment dominating costs. Aurora believes that it can cut its customers’ costs by 25-40%, primarily by reducing labor expenses. This includes eliminating the driver, eliminating the need to recruit and train drivers, and reducing the overheads needed to support drivers. Aurora’s technology could also reduce fuel use by up to 32% through more efficient vehicle operations. Trucks in a platoon reduce cut resistance, reducing fuel consumption by around 5% for the lead truck and 10% for following trucks. Self-driving trucks should also result in improved utilization, as drivers are subject to 11 hours of service limitation. Autonomous trucks could also help to improve road safety, with 94% of crashes tied to human choice or error. As a result, safer operations should also help to reduce insurance costs.

Figure 1: Trucking Labor Costs Continue to Rise (source: Aurora Innovation)

Transportation on highways between metro areas should be relatively amenable to autonomous vehicles as they are better able to handle situations that occur more frequently. Interstate highways are built to the same general standards and typically have fewer obstacles. Other vehicles are also travelling in the same direction and tend to be travelling at similar speeds.

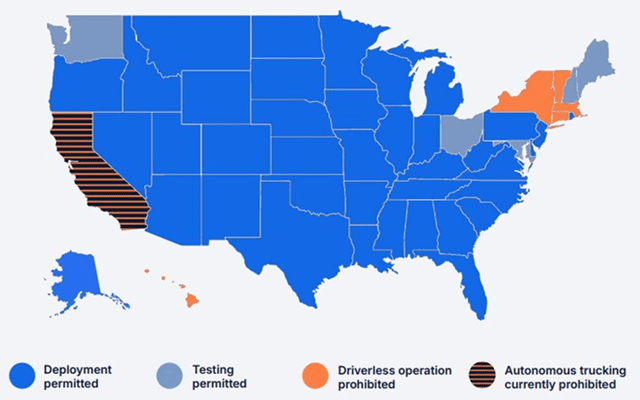

Under existing laws and regulations, autonomous vehicles can be deployed in most states. In particular, Aurora plans on launching its commercial services in Texas, which does not currently require additional regulatory steps. Autonomous vehicle legislation also continues to advance across the US. Given the technical challenges facing autonomous technology developers, regulatory risks are a secondary concern at this point in time.

Figure 2: Autonomous Vehicle Regulations in the US (source: Aurora Innovation)

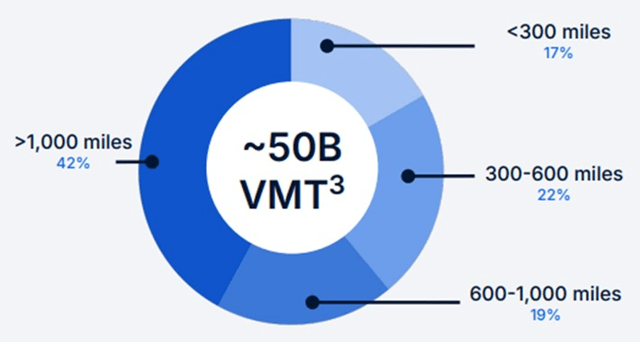

Aurora believes its serviceable addressable market will be 50 billion VMT by the start of 2028. While human-driven trucks are significantly more expensive than rail, autonomous trucks should be cost competitive or even lower cost, which could help to expand the market.

Figure 3: Aurora VMT by Length of Haul (source: Aurora Innovation)

Competitors in the space include Einride, Embark, Kodiak, Torc, TuSimple, and Waymo. The self-driving truck challenge hasn’t proven easy though, and as a result, the field is thinning over time. For example, Torc was acquired and TuSimple abandoned its autonomous trucking ambitions.

TuSimple shut down its self-driving truck efforts in December 2023 after losing its partnership with Navistar. It also laid off most of its staff and pared down its operations, shifting focus to the Chinese and Japanese freight markets. TuSimple had been working with Navistar and UPS and conducting testing in Arizona and Texas using its fleet of 40 trucks, including depot-to-depot supervised autonomous runs.

Waymo has also suspended its autonomous truck development efforts but has stated that it will return to the market in the future. The move was reportedly driven by a decision to focus on the ride-hailing market. Waymo began testing its technology in trucks in 2017, before launching a pilot program in 2018. These efforts were grouped into Waymo Via, a logistics unit focused on autonomous delivery.

Commercial trucks equipped with Kodiak’s technology currently operate on freeways with a safety driver onboard. Kodiak operates its vehicles in 10 states, both on test runs and carrying customer cargo between Dallas and Houston, Austin, Oklahoma City, and Atlanta. Kodiak also recently completed a pilot run between San Francisco and Jacksonville, Florida. After 5 years of testing, including 5,000 loads carried more than 2.5 million miles, Kodiak recently decided that a safety driver would no longer be necessary.

Kodiak is also working on an off-road solution for the military. While this effort is somewhat tangential to its main business, Kodiak won a 50 million USD contract from the DoD to help the Army automate ground vehicles. Building on this work, Kodiak is now launching a fully driverless trucking service in partnership with Atlas Energy Solutions, a provider of proppant and oilfield logistics. The deal will involve two trucks to start, with potential for more to be added over time. Atlas will purchase the trucks from an OEM and Kodiak will install its tech and provide monitoring and ongoing support for the service.

Aurora Innovation

Aurora is taking an asset light approach to the self-driving truck market, choosing to focus on the segment of the value chain where value is created (self-driving hardware and software). The company is leveraging partners to manufacture hardware (Continental) and install the hardware in trucks (OEMs). Customers operate the vehicles, with Aurora receiving a Driver-as-a-Service fee.

Aurora’s technology (Aurora Driver) is built to eventually be deployed in a range of vehicles (trucks for freight, vans for local goods delivery, cars for passenger mobility). Aurora is trying to create a solution that exhibits human-like behavior, follows the road rules and is transparent. To do this, Aurora combines a rules-based approach with AI, although the company considers it an AI first approach. While the hand coded approach creates a minimum viable product, it doesn’t scale, making AI a necessity.

An end-to-end AI solution may exhibit unpredictable behavior though and lacks transparency. Transparency is beneficial from a regulatory perspective, both in terms of justifying why the system is safe and addressing issues when they occur. An AI only approach is also complicated by the fact that it is difficult to collect enough data to handle all edge cases. Even when data on edge cases can be collected, training on these cases can lead to unexpected failures in other scenarios. This leads to a train and pray type approach, which is unacceptable in safety critical applications. Training data is also often dominated by undesirable behavior, like failing to fully stop at a stop sign. Hard-coded rules are a relatively straightforward way of addressing some of these issues.

Aurora makes extensive use of testing to ensure its system is safe to operate on the road. This includes both virtual testing and a small amount of testing with a physical truck on a test track. Virtual testing involves running the self-driving software offline using synthetic or real historical data. This enables Aurora to conduct millions of tests each day, assessing different permutations of the same scenario in a safe and scalable manner, and fine-tuning new capabilities quickly.

Perception tests are conducted to assess whether the software can correctly detect and identify objects of interest. This is generally done with real-world data, but Aurora is also developing realistic sensor simulations that will allow it to generate tests for unusual scenarios. While game engine outputs are sufficient for the human eye, they are not the same from a sensor input perspective. Driving evaluations compare the performance of Aurora’s self-driving software to the behavior of humans in the same scenario.

Aurora continues to improve the Aurora Driver’s autonomy performance and prepare for commercialization. This includes advancing its launch lane Safety Case. Safety Case is Aurora’s evidence-based approach to demonstrating that its self-driving vehicles can safely be operated on public roads. Aurora quantifies its progress with its Autonomy Readiness Measure, which is a weighted measure of completeness across all claims of the Safety Case for its launch lane. As of mid-April, ARM was 95%.

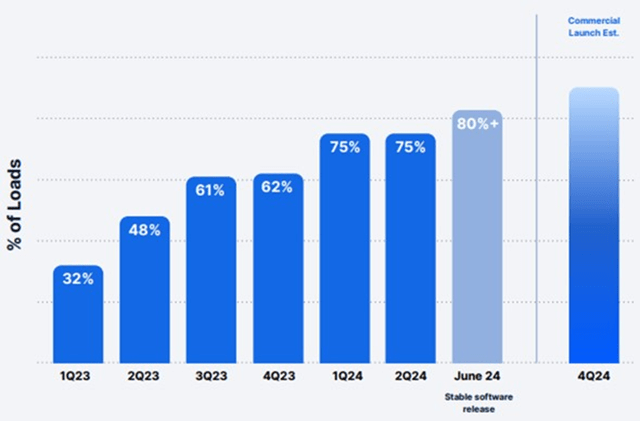

Performance is also assessed using API (Autonomy Performance Indicator). This indicator penalizes the use of onsite support, which will be the most expensive support provided. A commercial load that doesn’t require any form of on-site support would have 100% API. Aurora achieved an aggregate API of 99% in the last quarter. The company is now focused on increasing the percentage of commercial loads that do not require any onsite support. During the first quarter, 75% of the commercial loads in the launch lane had 100% API, up 13% sequentially. This figure is expected to be around 90% at commercial launch.

Figure 4: Aurora 100% API Loads (source: Aurora Innovation)

Aurora plans on introducing its next-generation Aurora Driver hardware kit in 2025. This kit is expected to bring performance gains and is designed for 1 million miles, improved reliability and assembly by contract manufacturers. Aurora is targeting a 50% cost reduction for this kit, driven by material costs and increased reliability.

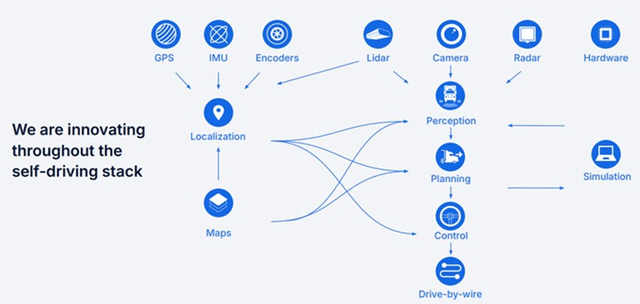

Figure 5: The Self-Driving Stack (Aurora Innovation)

Sensors are an important part of the self-driving tech stack, with Aurora choosing to leverage a range of high-fidelity sensors. While this adds to costs, Aurora believes that it accelerates the path to human level performance and enables superhuman performance (e.g., long range in vision in foggy conditions).

Different modalities have distinct strengths and weaknesses, meaning a system incorporating multiple modalities tends to have improved reliability. While this approach requires Aurora to map out routes, the company has suggested that little driving is needed on new routes to generate a map. Given the company’s focus on a limited number of defined routes, this shouldn’t be an issue anyway.

The perception system (lidar, cameras, radar) is a critical part of the tech stack in autonomous trucks, as the speed and mass of the vehicle means it needs to be able to see a long way ahead. Aurora is relying on lidar in this regard and has made significant investments in support of its capabilities.

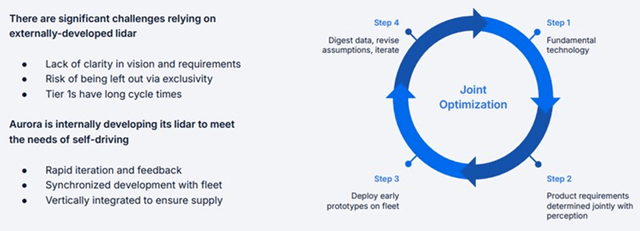

Aurora acquired Blackmore in 2019 for its Frequency Modulated Continuous Wave Lidar technology. Aurora also acquired OURS for its solid-state scanning mechanism and FMCW technology. FMCW provides simultaneous range and velocity detection at every point using the Doppler effect, which enables a faster response to changes on the road. It also eliminates virtually all interference from sunlight and other sensors. Aurora’s FMCW lidar also operates around the 1550nm wavelength band, allowing it to emit stronger light pulses while still meeting eye safety standards.

Figure 6: Advantages of Developing Long-Range Lidar In-House (source: Aurora Innovation)

Aurora has OEM and Tier 1 partnerships with a range of companies across manufacturing, hardware installation and fleet management. Continental will be manufacturing/assembling Aurora’s hardware, although the Continental kit isn’t expected to be in Aurora trucks until 2027. The company also recently engaged Fabrinet to assemble its next-generation Aurora Driver hardware kit. This will support Aurora’s initial scaling efforts before Continental starts production.

Aurora also has a number of OEM partners that will integrate Aurora’s self-driving tech into their vehicles. These OEM partners collectively represent nearly 50% of the US market. Aurora began by retrofitting existing trucks for pilot programs, but OEM partners have now developed specially built trucks for commercialization.

Volvo is one of Aurora’s OEM partners, with Volvo recently introducing the Volvo VNL Autonomous truck. The truck is designed for autonomous operations and features Aurora’s self-driving tech, along with a range of backup systems. Volvo has already started to manufacture an initial test fleet and Aurora plans on starting to use these to haul freight in the next few months.

Paccar is another one of Aurora’s OEM partners. The companies have an agreement to develop, test and commercialize autonomous Peterbilt and Kenworth trucks.

Aurora partnered with Ryder to provide on-site fleet service for its pilot programs. Ryder technicians are embedded in Aurora’s terminal, providing maintenance and servicing. The companies are also collaborating on other services, like roadside assistance.

Aurora has also partnered with a number of logistics companies, which will help to drive demand as commercialization begins. Pilot customers include FedEx, Werner, Schneider, Hirschbach, Uber Freight and others.

Aurora’s partnership with Uber Freight provides Uber Freight carriers with a streamlined path to purchase and onboard the Aurora Driver. It gives early access to over 1 billion driverless miles through 2030. Aurora hopes the program will accelerate adoption of its Driver-as-a-Service solution.

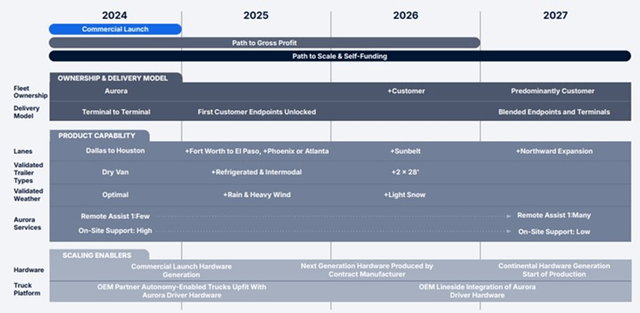

Aurora is currently scheduling 140 loads per week, nearly triple the commercial volume from a year earlier. Through to the end of July 2024, Aurora had delivered a total of 6,785 commercial loads across over 1.8 million miles. This is up from 5,450 loads and 1.5 million miles through the end of April. Aurora is currently targeting a commercial launch in late 2024, with expansion across the Sunbelt expected in 2026.

Figure 7: Aurora Driver Indicative Roadmap to Scale (source: Aurora Innovation)

Financial Analysis

Aurora is currently generating a small amount of revenue from its pilot programs. The company generated 565,000 USD pilot revenue in the first quarter, up nearly 100% YoY. This continues to be recorded as a contra R&D expense.

Longer term, Aurora’s revenue will rise as it drives more commercial miles. Aurora has a Driver-as-a-Service business model where customers are charged on a per mile basis. Pricing should be largely dictated by market rates on the routes that Aurora operates.

Aurora bears the cost of product development, hardware, remote assistance, on-site support, insurance, etc. and believes that it can generate high gross margins while still providing a TCO benefit to customers. This will be dependent on competition from other AV players, though.

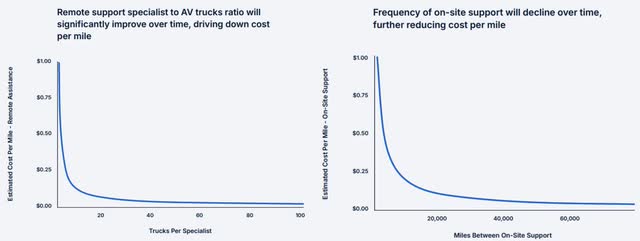

Aurora is targeting gross profits by the end of 2026, which is expected to come from a combination of revenue growth (lane penetration and expansion) and cost reduction (reduced remote assistance and on-site support, next-gen hardware).

Figure 8: Expected Decline in Remote and On-Site Support Costs (source: Aurora Innovation)

Aurora’s operating expenses totaled 193 million USD in the first quarter, driven by R&D. Excluding SBC, operating expenses were 157 million USD. Aurora used approximately 150 million in operating cash during the first quarter, including 9 million USD in prepayments for hardware components to support the commercial launch. CapEx was 8 million USD.

Quarterly cash use is expected to be 175-185 million USD on average in 2024 as Aurora prepares for its commercial launch. Q2 cash spend is expected to be above this range though due to the payments associated with Aurora’s 2023 annual incentive compensation program.

Aurora ended the first quarter with 1.2 billion USD in cash and investments. The company expects its liquidity to be sufficient to support its commercial launch and fund operations into the fourth quarter of 2025.

Conclusion

While Aurora may seem highly speculative, particularly given the struggles of many other players in the space, I think the company is credible and has a real shot at building a strong business. Aurora is backed by Sequoia Capital and Amazon and Uber also has a stake. This came after Aurora took control of Uber ATG and received a 400 million USD investment from Uber in return for a 26% stake in the combined company. Aurora’s partners also mean that it should be able to rapidly scale the business if the software performs well.

The economics of Aurora’s business should be strong while AVs have a small market share, particularly as the need for on-site support declines. Margins may compress over time though if AVs come to dominate the market and competition is fierce.

Despite Aurora potentially approaching an inflection point in the next few years, its valuation may still mean that returns are poor for shareholders. Aurora probably needs to be doing something like 500-1,000 million miles per year to make its current market capitalization appear more reasonable. There is significant technology and execution risk involved in achieving this type of scale, which doesn’t appear to be priced into the stock.

Read the full article here

(NASDAQ:META)")

")

")

ECTRIMS 2024 Investor Science Call Transcript")