")

(NASDAQ:META)")

")

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company (“BDC”) sector from both the bottom-up – highlighting individual news and events – as well as the top-down – providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the first week of September.

Market Action

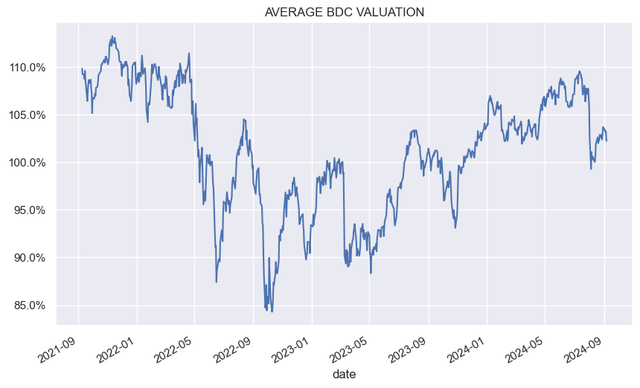

BDCs were down around 1% on the week. Outperformers this week were the lower valuation BDCs such as MRCC, PSEC, WHF and others, something which happens regularly in down markets. The weak start to the month is in line with the three previous months, which finished flat or down for the sector.

The bounce from the early August drawdown has stalled, and BDCs in our coverage finished the week with an average valuation of 103% – well below the recent peak of 110%.

Systematic Income

Market Themes

Analyzing net investment income or NII is a key part of the due diligence for many income investors. One element of the process is gauging how much of NII is due to common shareholders and how much is due to preferred shareholders. This is something we have discussed over the last several years in the context of a number of equity CEFs, particularly the Gabelli funds such as GUT, as well as PIMCO Muni CEFs such as PML and others.

As many investors know, perpetual preferreds, unlike term preferreds, are not considered interest expense and are not subtracted from NII for GAAP purposes. However, preferred dividends still need to be paid and that will come out of NII or capital gains / ROC, if there is not enough of NII. What this means is that common shareholders who take NII at face value may be overestimating common dividend coverage or how much “yield” they are actually earning. What makes this particularly challenging is that few CEFs use preferreds for financing, and so many investors simply take a given NII at face value without subtracting preferreds dividends from it.

A similar situation exists in the BDC space as well. To our knowledge only CGBD and PSEC have been using preferreds with the CGBD preferred now having been converted to common shares at the NAV. In the case of CGBD, the preferred was issued to an affiliate of Carlyle during the COVID drawdown as an emergency measure. In the case of PSEC the preferreds are business-as-usual and a significant part of its asset growth.

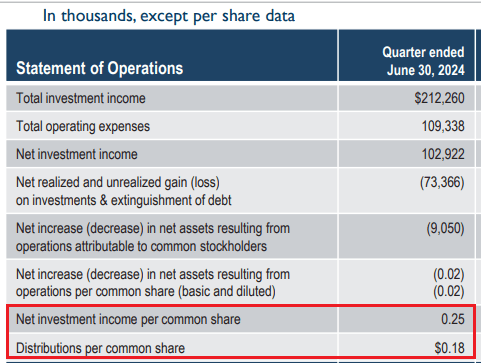

If we look at the earnings presentation, what we see is NII of $0.25 vs distributions of $0.18, suggesting ample common dividend coverage of 139%.

PSEC

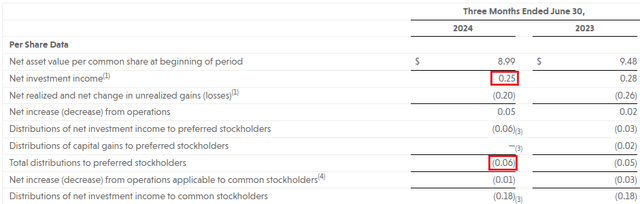

We need to go to the press release to figure out the NII which actually goes to common shareholders. Here we see that $0.06 is used to pay the preferreds dividends, leaving around $0.19 for common shareholders, resulting in lower coverage of around 105.5%.

PSEC

PSEC do provide the following comment “Net investment income less preferred dividends exceeded cash common distributions by 124% for LTM June 2024”. This is certainly a useful comment, however it does overstate today’s situation for the simple reason that last quarter’s net investment income is below the LTM figure and that preferreds distributions have grown over the past year to a new high.

CGBD were very upfront in their presentation about the impact of the preferred dividend and, in fact, the only version of NII they showed in the presentation was the one with the preferred dividend subtracted, whereas for PSEC it’s the other way around. Hopefully, PSEC can make a similar update to make it more explicit what is going on. Until then, investors have to do their own homework.

Market Commentary

With the BDC earnings season firmly behind us, there has been little market-moving information. The usual run-of-the-mill events like new portfolio investments and credit facility upsizes have dominated news flow.

Main Street Capital (MAIN) completed a new investment of $11.2m in MoneyThumb – a software provider for companies in the accounting industry. Trinity Capital (TRIN) announced a $20m commitment to Kymeta – a satellite antenna company.

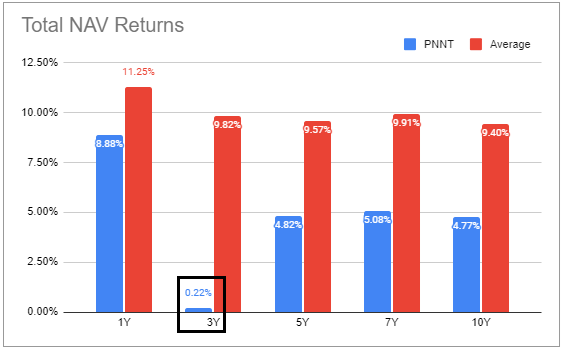

PennantPark Investment Corp (PNNT) agreed to invest an additional $52.5m in PennantPark Senior Loan Fund – a joint venture with Pantheon Ventures. PNNT said the JV has generated strong returns which is more than we can say for PNNT whose 3Y total NAV return is not much above zero.

Systematic Income BDC Tool

Stance And Takeaways

The average BDC valuation remains above 100% (the median is at 96%) which is slightly expensive of fair-value in our view. We added a number of BDCs to our Income Portfolios after the initial drop in prices in early August. Since then, however, we have held off. If BDCs regain their previous peak of around 110%, we would look to downsize our allocation. On the other hand, a further drop below 100% would likely bring out new opportunities. In our view, the coming drop in short-term rates, in the absence of a recession, is unlikely to cause a drop in BDC prices or a widespread cut in BDC dividends despite opinions to the contrary. This is why we would view occasional panic as an opportunity to add.

Read the full article here

")

(NASDAQ:META)")

")

")