")

")

Introduction

In 2023, Casgevy was the first (alongside Lyfgenia) gene editing treatment approved in the US. Casgevy is jointly owned by Vertex Pharmaceuticals (VRTX) and Crispr Therapeutics (NASDAQ:CRSP) who’s shared interest is split 60-40. Casgevy edits patient stem cells to treat sickle cell disease and beta thalassemia by editing the BCL11A gene using the CRISPR/Cas9 technology.

bluebird bio’s (BLUE) Lyfgenia’s works slightly differently, but ultimately both treatments show significant positive outcomes for patients in trials. In Casgevy trials, more than 93% of patients didn’t have any vaso-occlusive crises in the 12 months following treatment. For more background on Casgevy, please see my previous article, where I discuss the pros/cons and the treatment process for patients.

To note Lyfgenia’s black box cancer warning could have easily been on both treatments as busulfan (chemo conditioning) which is used for both options, is problematic because patients with SCD have a high risk for haematologic malignancy (two patients). Therefore, I wouldn’t say the black box warning is an advantage, rather the significantly cheaper price point ($900k cheaper) and the backing from Vertex is what gives Casgevy an advantage over bluebird bio’s Lyfgenia.

Casgevy – $2.2m

Lyfgenia – $3.1m

Furthermore, it seems Casgevy is easier to understand for patients vs Lyfgenia which uses something called lentivirus to edit patients cells. Vertex is a $120bn established pharmaceutical company and Crispr is a pre-revenue biotech specialising in gene editing with a number of assets in development. A significant benefit of partnering with a giant like Vertex is that Gasgevy will have more distribution resources behind it in order to develop a bigger network of ATC’s (Advance Treatment Centres) compared to bluebird bio.

bluebird bio has $174m in cash and is valued at an all-time low of $100m, suggesting the company lacks resources to ramp up as aggressively as Vertex. Although, bluebird bio announced earlier this year a $175m term loan facility from private credit VC lender Hercules Capital. A speculated buyout isn’t likely in the short term, but it remains a possibility. I’d argue if it wasn’t for Casgevy, bluebird bio would’ve been acquired a long time ago.

Crispr themselves are well capitalised with $2bn in cash and boasts an extremely healthy balance sheet with a Current Ratio above 15x.

Huge TAM But Slow Uptake

Crispr told investors that there are circa 35k severe patients across the US/EU with SCD and TDT that would be suitable for Casgevy. In speaking with experts who treat SCD, many argue it will take many years to even put a small dent in that 35k figure due to an extremely slow roll out.

Casgevy is now rolled out across 26 ATCs in the US and as of July, Vertex has activated 35 ATCs globally. The problem, once the patients’ stem cells have been collected it, takes up to 6 months to edit and return, which is why treatment time can be between 7-10 months per patient. Investors are eagerly waiting to see if Casgevy’s treatment time will improve over the coming years, as this could lower treatment cost, increase uptake and lead to more revenue in each period. Specifically, any technological advancements to improve CRISPR/Cas9 gene editing manufacturing time.

Vertex is also doing preclinical research into a less toxic conditioning medicine for Casgevy. Before newly edited cells can be returned, a preconditioning treatment with Busulfan is used to clear existing patient stems, which will make room for newly edited cells. By using an alternative to Busulfan with a lower toxicity, the addressable patient population could increase to 150k across the US and EU. This could be a huge development, as Casgevy would be a much easier (and much safer) treatment process for patients.

Quick Sales Exercise

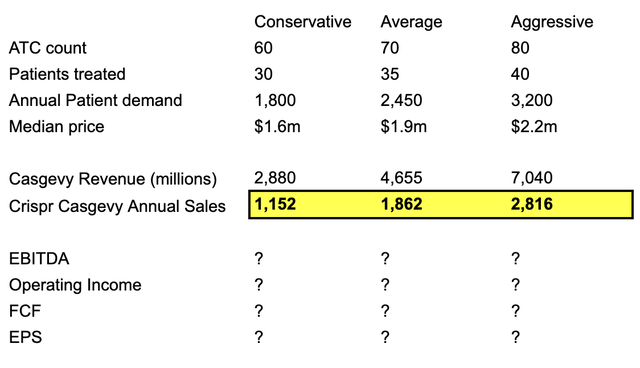

Without knowing how profitability will evolve for Crispr, it might be interesting to do a simple revenue exercise. The table below illustrates what revenue might look like in 5 years time, assuming Vertex almost doubles their ATC network from 35 to 60 over this period as the conservative estimate. Based on experts I’ve heard from, 20-40 patients would be treated in each centre, but maybe this improves to 30-40 range over 5 years.

Created By Author

Therefore, sales towards the end of the decade could be between $1.2bn – $2.8bn assuming capacity is the limiting factor and the “35k patients” marketed from Vertex and Crispr is accurate. 19 sell-side analysts expect sales of $1bn in FY27, thus $1.2bn – $2.8bn seems very reasonable around 2029.

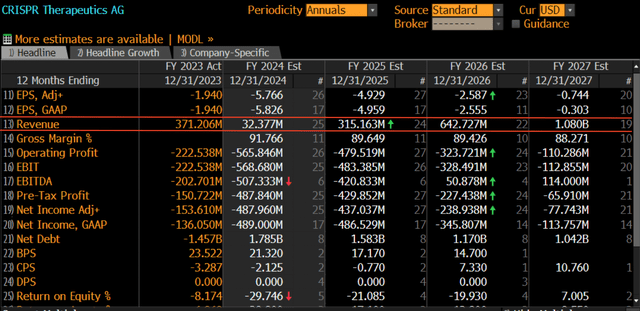

Bloomberg Terminal (EEO)

Considering today’s market cap of $4bn and potential Casgevy sales in 5 years of around $2bn with a secular growth runway is very attractive. However it’s worth noting the further out a forecast the harder it is to be precise, I’ve seen 12 month consensus estimates missed by significant amounts, so don’t base your thesis on this alone.

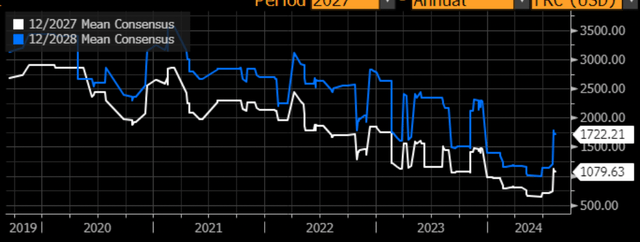

Bloomberg Terminal (EEB)

Above is the change in revenue projections for FY27 and FY28 overtime. Recently, both figures have shot up as news on Casgevy ramp up is being delivered to the market. Overall, these estimates are positive for long-term investors and suggest to me that Crispr’s valuation is not too “excessive”.

Conclusion

Each time I come back to Crispr it’s an exciting read; however, future profitability still seems elusive, making it hard to value the company. Today’s $4bn valuation could be undervalued or overvalued, as it’s impossible to build out financial assumptions with any degree of conviction. Furthermore, it’s difficult to put a number on Crispr’s pipeline potential. Although long-term there’s a strong argument that Crispr’s revenue will easily break $1bn within 5 years and quite possibly $2bn, but what sort of margins and profitability levels this leads to is another big question mark for investors.

One area not discussed in this article was payer coverage. While the 2 new approvals for SCD won’t cover 100% of lives under Medicaid, it’s likely the outcomes-based reimbursement will cover the initial majority with severe SCD. Vertex has communicated they’re in talks with 18 states; however, it’s unlikely payers would include fertilisation services as part of coverage. With the current pre-conditioning regime, patients will be unable to have children after treatment. Thus, freezing of sperms/eggs is currently an additional cost for patients.

According to FINRA, as of August 15th, there were 17.17m Crispr shares sold short, resulting in a 20% short interest based on 84.92m shares outstanding. This signals that L/S funds expect Crispr to underperform, at least in the short term.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")