")

")

")

Intro

Our initial bullish call in Viemed Healthcare, Inc. (NASDAQ:VMD) came in December 2021 on the back of aggressive revenue growth, growing equity, and a bullish technical formation. Although shares did not bottom in earnest until February of the following year, the stock has still returned just under 35% since that bullish call. For comparison purposes, the S&P500 has returned approximately 14.7% over the same timeframe.

In our most recent commentaries, however (November 2023 & April of this year), we reverted to a ‘Hold’ rating, primarily due to growth concerns & the absence of a defined bullish trend on the technical chart. However, after digesting the bottoming of the stock in July of this year followed by an encouraging Q2 earnings report (Announced on the 8th of August this year), we are upgrading Viemed Healthcare to a ‘Buy’ once more. Let’s start with some technical analysis that explains our reasoning for the rating upgrade.

Technical Analysis

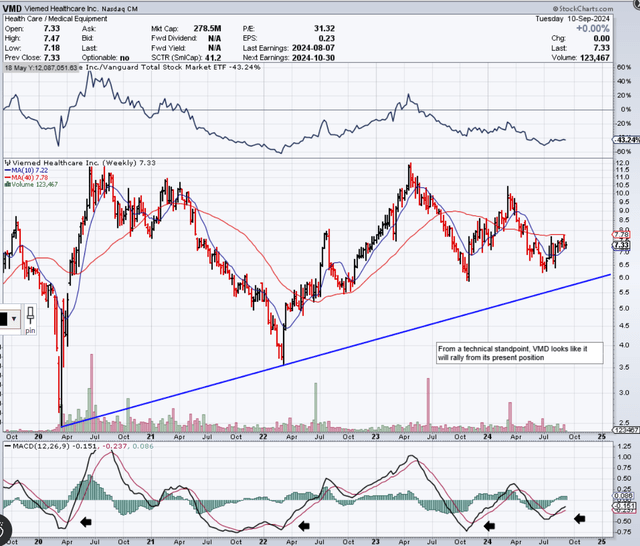

If we first pull up an intermediate 5-year chart, we can see that bullish share-price action in Viemed over the past two months or so has resulted in a bullish crossover of the MACD. MACD crossovers are noteworthy on long-term charts due to the dual role of the indicator (Trend & Momentum) and how a significant amount of information makes up the readings. Prime conditions for the use of the MACD are when the crossover takes pace well below the zero line (Oversold) & when the stock in question is in a bull market. These are the conditions we presently have in Viemed which makes us believe history will repeat itself once more here, culminating in a sustained move to the upside.

Viemed Healthcare Intermediate Technicals (Stockcharts.com)

12-Month Technical Chart

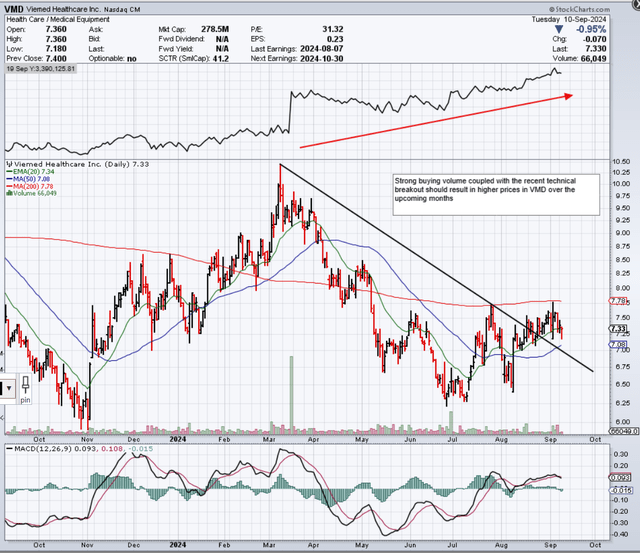

On Viemed’s short-term chart, we see several encouraging trends.

- Firstly, Viemed’s encouraging second-quarter earnings report enabled shares to break out above the bearish trend line depicted below. Although the 200-day moving average of approximately $7.78 put a halt to the post-earnings rally, we believe it will only be a matter of time before this resistance level gets surmounted.

- Secondly, since this year’s March highs of approximately $10 a share, although shares have fallen by 27%, buying volume through this period has been very strong. Suffice it to say, given that volume trends in the main precede share-price action, this divergence cannot continue in its present form which is why we are banking on the share-price to rise from current levels.

Viemed Healthcare 12-Month Technicals (Stockcharts.com)

Encouraging Q2 Trends

Top-Line Growth Acceleration

Revenue in the second quarter rose to a record-beating $55 million (27% rolling quarter growth), boasting $900k organic growth to boot & a 4.4% increase in active ventilator patients. Through smart investment plays (such as the recent majority interest acquisition of HomeMed) where the integration has hit the ground running along with sustained organic growth (which management believes is attainable), Viemed looks like it will continue to go from strength to strength concerning top-line growth & patient numbers.

Sales Force Hitting Performance Targets

The restructuring of the company’s sales personnel (so more patients could be reached) earlier in the year seems to be paying off in spades. This trend can be seen individually (through monthly setups sales representatives are achieving) & performance-wise (concerning targets), resulting in a much hungrier sales force overall. Suffice it to say, we now expect management to leverage this new model by bringing in more personnel to scale Viemed’s ventilator growth path over time.

Sleep Business Organic Growth Remains Strong

Whereas initially, investors may have thought that the introduction (and strong traction) of GLP1 drugs would have encroached on Viemed’s ‘Sleep’ business, recent trends reflect nothing of the sort. Although GLP1 offerings may very well reduce the risk of COPD, their place in the market seems to have put more attention on ‘Sleep’ offerings in general. To this point, since their inception, GLP1 drugs seem to have increased awareness in a significant way, resulting in sustained growth in Viemed’s CPAP & Sleep lines in recent quarters.

Phillips Recall Opportunity

The recent recall of Phillips’ ventilators has presented an opportunity for Viemed to significantly improve its fleet. In essence, management turned a problem into a workable solution through a buy-back deal where older units will be changed for newer units at a reduced price. Furthermore, on top of the initial financial advantage, ongoing servicing of the older units no longer in stock has also been done away with.

The recent Philips recall of these older machines has presented a unique opportunity to replace these devices and alleviate the need for future servicing. We’ve entered into an agreement with Philips to buy back a large number of our affected events. By leveraging substantial volume purchase discounts with manufacturers of new ventilators, we can use the proceeds from the buyback to significantly reduce the average age of our VIP fleet without negative impacts on our overall cash flows and P&L.

Shares Remain Cheap From An Assets & Sales Perspective

Although Viemed’s trailing GAAP multiple of almost 32 does not look cheap, the company’s sales & book multiples are very attractive when compared to 5-year averages. In fact, the company’s trailing book & sales multiples are north of 40% below the 5-year averages for this company, as we see below.

| Multiple (Trailing) | VMD | 5-Year Average | % Difference To 5-Year Average |

| Price To Sales | 1.37 | 2.54 | – 45.9% |

| Price To Book | 2.38 | 4.00 | – 40.3% |

This is noteworthy because the cheaper one can buy assets & sales (the very areas that enable earnings growth to happen) of a company, the more probable earnings growth comes as a result. To this point, shares have only rallied a mere 14% over the past five years.

Conclusion

Therefore, to sum up, with technological investments remaining to the fore concerning Viemed’s Engage platform, we expect to see the fruit of these investments in upcoming quarters. Furthermore, the company’s encouraging technicals, growing ventilator patient count, and attractive valuation point to a rising share price over the near term. We look forward to continued coverage.

Read the full article here

")

")

")