")

")

")

")

")

APP’s High Growth Investment Thesis Remains Valid, Despite The Balance Sheet Headwinds

We previously covered AppLovin (NASDAQ:APP) in May 2024, discussing why we had rated the stock as a Buy then, attributed to its robust performance metrics, excellent gaming advertising partnerships, and upcoming entry to other in-app advertising markets from FQ2’24 onwards.

Combined with its high growth prospects and raised consensus forward estimates, we believed that the stock might continue to offer excellent upside potential.

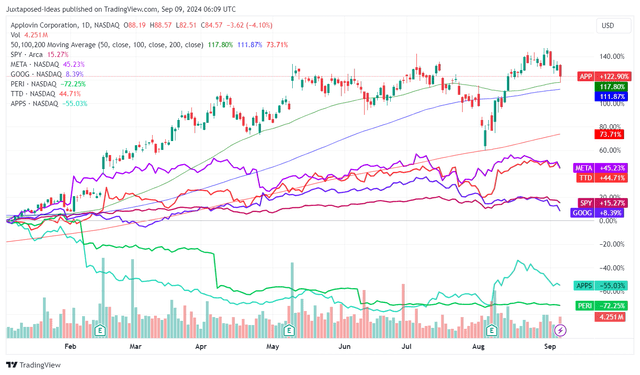

APP YTD Stock Price

Trading View

Since then, APP has had a robust YTD stock performance, one similarly observed in numerous ad-tech peer and advertising giants, including Trade Desk (TTD), Meta (META), and Alphabet (GOOG), with these stocks rapidly recovering after the recent market rotation in July 2024.

This outperformance is not surprising indeed, attributed to the “healthy global advertising demand” and “strong growth from China-based advertisers,” as reported by META in the latest earnings call.

The same has been reported by APP, with its Rest of the World’s revenues growing to $448.61M (+5.9% QoQ/ +51.3% YoY) – accelerated compared to the one observed in the US at $631.5M (-0.4% QoQ/ +39.1% YoY) in FQ2’24.

Combined with the growing Average Revenue Per MAP [ARPMAP] of $52 (+8.3% QoQ/ +13% YoY) albeit the lower Monthly Active Payers [MAP] of 1.6M (-11.1% QoQ/ -5.8% YoY), it is unsurprising that the ad-tech company has reported a bottom-line beat in the recent earnings call.

This is with revenues of $1.08B (+2.8% QoQ/ +44% YoY), adj EBITDA margins of 55.6% (+3.9 points QoQ/ +11.2 YoY), and GAAP EPS of $0.89 (+32.8% QoQ/ +304.5% YoY).

Most of APP’s tailwinds are attributed to the Software Platform comprising 65.8% of its sales (+1.8 points QoQ/ +11.7 YoY) with an increasingly rich adj EBITDA margins of 73.1% (+0.6 points QoQ/ +6.2 YoY), with the +4.8 QoQ/ +75.1 YoY rate growth in sales well exceeding the management’s long-term growth target of between 20% to 30%.

The success is naturally attributed to the company’s ongoing expansion across new verticals beyond gaming to eCommerce, CTV, original equipment manufacturer [OEM], and carrier-related markets, thanks to its new AI-powered advertising engine AXON, AppDiscovery, Adjust, and MAX auction.

Even so, readers need not be concerned about the impact of APP’s growth initiatives on the bottom-line, as observed in the robust FQ2’24 results, since the management plans “to expand our teams in a very lean and targeted manner,” with it “illustrating our ability to remain disciplined with our costs, growing revenue while remaining lean and efficient.”

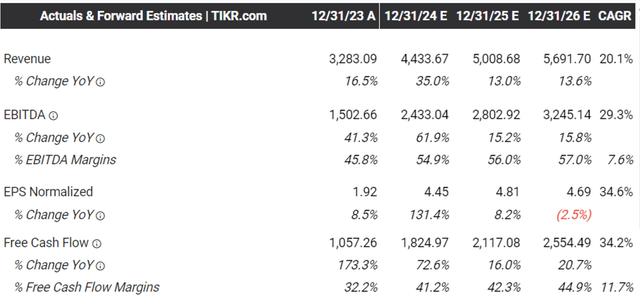

The Consensus Forward Estimates

Tikr Terminal

As a result, it is unsurprising that APP has also offered a promising FQ3’24 earnings guidance, with revenues of $1.125B at the midpoint (+4.1% QoQ/ +30.2% YoY) and adj EBITDA of $640M (+6.4% QoQ/ +52.7% YoY).

This may also be why the consensus have raised their forward estimates, with the ad-tech company expected to generate an accelerated top/ bottom line growth at a CAGR of +20.1%/ +29.3% through FY2026.

This is compared to the previous estimates of +18.1%/ +25.9%, while building upon the historical growth of +46.6%/ +35.6% between FY2018 and FY2023, respectively.

These growth rates do not appear to be overly aggressive as well, as APP hints at promising early results into the web advertising pilot launched in Q2’24, with it being “materially better than what we would have expected this early in our progression.”

With the management already scaling and guiding a material impact in FY2025/ beyond, we believe that there are great chances of its upgraded top/ bottom-line estimates, given that Statista already expects the global in-app advertising market to grow from $352.7B in 2024 to $534.1B in 2029, expanding at a CAGR of +8.65%.

This is especially since APP continues to report growing market share in the advertising/ monetization Software Development Kits on Google Play from 15% in May 2024 to 16% in September 2024, with its market share on the iOS platform stable at 13% – allowing the company to increasingly monetize its ad-tech offerings ahead.

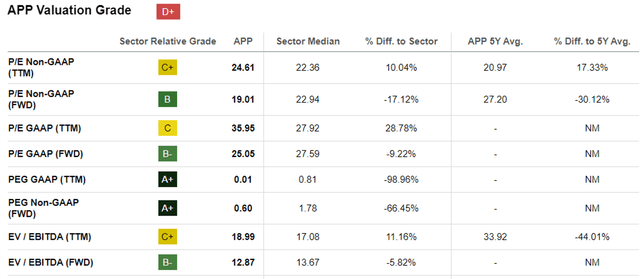

APP Valuations

Seeking Alpha

And it is for this reason that we believe APP remains cheap at FWD EV/ EBITDA valuations of 12.87x, compared to its 3Y mean of 16.42x and the sector median of 13.67x.

Based on the FWD P/E GAAP valuations of 25.05x and the projected GAAP EPS growth at a CAGR of +74.9% through FY2026, we are looking at an extremely cheap FWD PEG GAAP ratio of 0.33x, compared to the sector median of 0.81x.

Even when comparing APP’s FWD PEG non-GAAP ratio of 0.60x to the sector median of 1.78x and the ad-tech peers, such as the highly profitable TTD at 2.45x, Perion Network (PERI) at 0.29x, and the yet profitable Digital Turbine, Inc. (APPS) at 0.51x, we believe that the former remains reasonable at current levels.

So, Is APP Stock A Buy, Sell, or Hold?

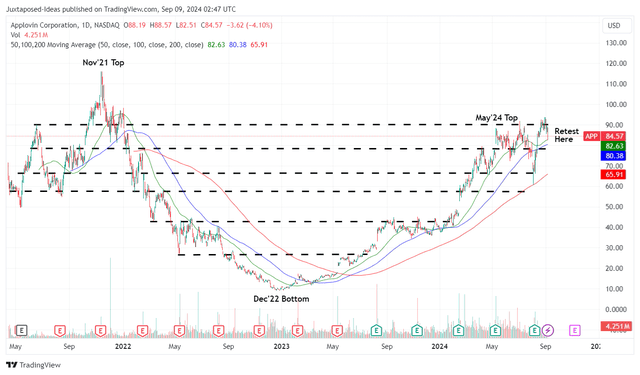

APP 3Y Stock Price

Trading View

For now, APP has mostly traded sideways since May 2024, aside from the one-time correction linked to the July 2024 market rotation, with the recovery since early August 2024 highlighting the immense bullish support.

For context, we had offered a fair value estimate of $72.60 in our last article, based on the FQ1’24 annualized GAAP EPS of $2.68 (+36.7% QoQ/ +6800% YoY) and the FWD P/E GAAP valuation of 27.10x.

Based on APP’s FQ2’24 annualized GAAP EPS of $3.56 (+32.8% QoQ/ +304.5% YoY) and the moderately downgraded FWD P/E GAAP valuation of 25.05x, it appears that the stock is trading cheaper than our updated fair value estimates of $89.20.

Based on the consensus’ stable FY2026 GAAP EPS estimates of $4.69, there remains an excellent upside potential of +38.9% to our reiterated long-term price target of $117.50 as well.

Readers must also note that APP has been returning great value to its existing shareholders with -5% of its float already retired over the LTM, or -10% since FQ4’21, with it implying the management’s competent use of rich cash flow.

With $500M remaining in its share repurchase program, we believe that the ad-tech company remains well positioned to continue doing so moving forward.

As a result of the highly attractive risk/ reward ratio, we are reiterating our Buy rating for the APP stock here.

Risk Warning

Despite APP’s accelerating growth prospects, readers must note its burgeoning net debts on balance sheet at $3.05B (-1% QoQ/ +31.4% YoY), albeit with moderating net-debt-to-EBITDA ratio of 1.42x by FQ2’24, compared to 1.74x in FQ1’24 and 2.07x in FQ2’23, thanks to its expanding adj EBITDA generation.

Even so, based on the $1.96B of shares repurchased (+161.3% sequentially) and $1.36B in Free Cash Flow generation over the LTM (+62.3% sequentially), it appears that the management is seemingly relying on debt to return value to shareholders – a strategy that may not be sustainable in the long-term.

With the higher debt levels already triggering expanded interest expenses of $294M over the LTM (+27.8% sequentially), readers may want to pay attention to APP’s near-term execution indeed, since it may trigger the deceleration in its GAAP EPS expansion moving forward.

Read the full article here

")

")

")

")

")