")

(NASDAQ:FTNT)")

Investment Thesis

Fortinet’s (NASDAQ:FTNT) recently concluded Q2 quarter was an enlightening revelation.

On one hand, the billings slowdown persisted just as I noted in my earnings preview of Fortinet’s Q2 quarter, with Fortinet’s management keeping full-year CY24 billings guidance unchanged from their previous quarters.

Then, on the other hand, management surprised everybody with a high-octane expansion of consolidated business margins across the board driven by increased operational efficiency through its business and the first possible signs of demand returning back to its products, such as firewalls and security appliances.

These signs were also seen in inventory levels that showed robust improvements for the first time in years, pointing to signs of demand weakness for Fortinet’s hardware products finally stabilizing.

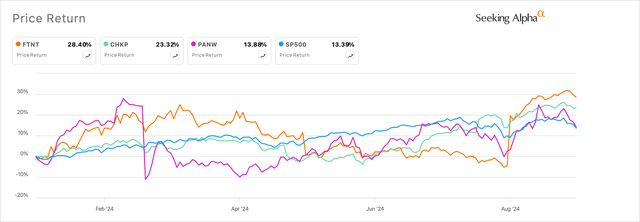

The solid surprise that Fortinet delivered was eventually seen in the company’s stock price, which surged right after its Q2 earnings report.

Exhibit A: Fortinet’s stock price is up 28% all thanks due to a robust Q2 earnings report. (Seeking Alpha)

In my view, the company’s Q2 report was a huge boost to the company’s outlook in terms of its margins, at the very least aided by a possible bottom in the contraction of Fortinet’s firewall and product business.

I am upgrading Fortinet to a Buy.

Billings Slowdown Still Persists, But Slowdown in Product Revenue Normalizes

In my previous coverage, I did expect a tempered outlook in Fortinet’s top line, mainly due to two factors:

First, the lack of chest-thumping that management usually does when parading its big sales deals at any opportunity they get. The mild/moderate tone of sales deals continued in the Q2 call, where management spoke about lumpiness and long sales cycles paired with an improving sales efficiency outlook as Fortinet absorbed the sales teams from its recent Lacework and Next DLP acquisitions. Still, management did highlight a few 7-figure deals on the call.

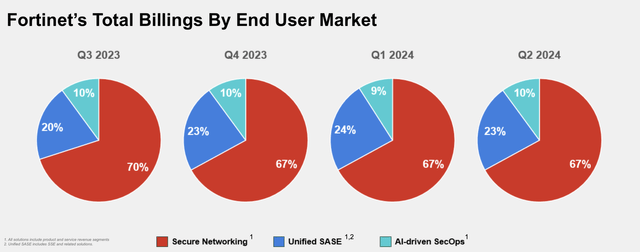

Second was the continued range-bound momentum in their Unified SASE and AI SecOps Billings, which flatlined after rapidly growing last year, as noted in Exhibit B below.

Exhibit B: Fortinet’s Billings By End User Market Solutions (Investor Presentation, Fortinet)

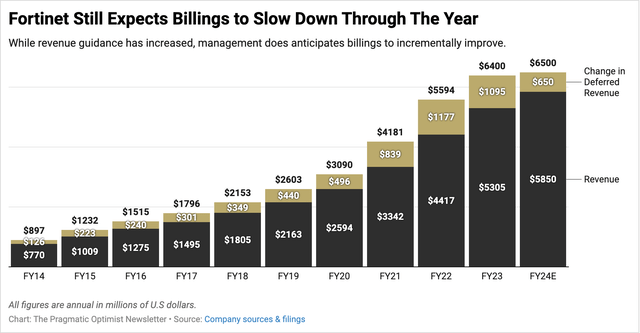

I did expect management to revise their billings guidance higher, at least after accounting for the inorganic lift that the Laceworks and Next DLP acquisitions would give the company’s consolidated billings. Unfortunately, management held the CY24 billings target in the range of $6.4-6.6 billion by mentioning that the inorganic lift in billings due to acquisitions was small, hence no change in billings.

Exhibit C: Fortinet’s Billings dollar volume by year including its 2024 target range (Company sources)

One of the surprises in the top line was the slower than expected decline in its product revenue, which dropped just 4% to $452 million in the quarter, much better than I expected. This was due to better-than-anticipated sales of the company’s firewall products and other security appliances and software licenses. Service revenue, which includes products in the SASE space, continues its strong double-digit growth, growing 20% to $982 million, but I was taken aback by the massive improvement in the company’s product revenue, which contracted at rates much better than I feared.

The reversal in product revenue contraction is good news for Fortinet, which should now boost overall revenue growth for Fortinet, which was being pulled up by the double-digit growth rates seen in its service segment.

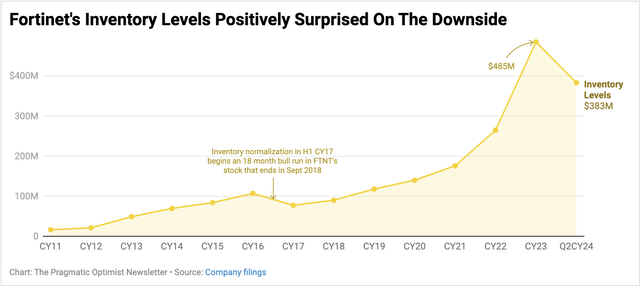

The smaller contraction trend in Fortinet’s product revenue also is confirmed by Fortinet’s inventory levels, which for the first time in many quarters dropped, pointing to signs that there is a reversal in the weak demand that was plaguing Fortinet’s revenue growth.

Exhibit D: Fortinet’s Inventory levels fall for the first time in many quarters. (Company filings)

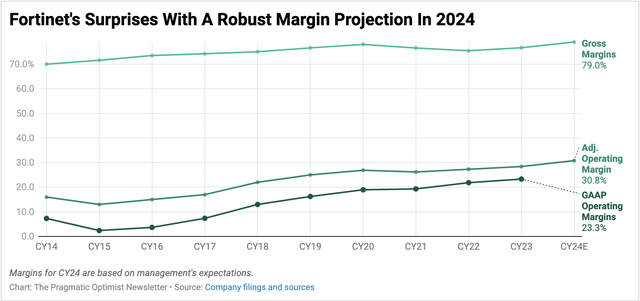

Margins On Steroids: The Big Takeaway

What Fortinet’s improving inventory levels have actually done, apart from improving top-line growth, is boosted the overall margin profile of the company as it ships more product out to its customers.

Exhibit E below attests to that observation, where margins across the board got a strong boost due to falling inventory levels.

Exhibit E: Fortinet’s Margins On Steroids With Robust Expansion (Company sources)

On the earnings call, most analysts were pleasantly surprised by the margin acceleration. Here is management’s response to the first question of the earnings call that started with understanding the margin boost:

I think the gross margin is the largest driver of what you saw in the operating margin, particularly when you look at it on a quarter-over-quarter basis and in that, we talked about or made reference to a more normalized environment for us in terms of inventory levels, turns and what we’re seeing with channel inventory but also commitments to our contract manufacturers. So I think that we’ve been working through that for probably the last 3 quarters, maybe 4 quarters. And with that, I would say, I think we’ve returned to a more normal state and so I would expect that to continue on.

As noted in Exhibit E, Fortinet usually manages its business closer to the ~27% operating margin level. This is also what I had modeled in my previous valuations, but with management sounding more optimistic about managing its business moving forward at the new normalized range of margins as demonstrated in Q2, I have raised my earnings outlook for Fortinet, which also boosts the valuation premium for the cybersecurity company.

Add to this outlook the growing scope for margins due to the elevated margin profile of Fortinet’s service revenue segment, and I can easily see how margins have room to expand by at least 22-25 bp over the next 10 calendar quarters.

Here is some more forward-looking commentary from management that is pertinent to the basis of my valuation model:

Also, we’ll benefit from the service revenue which has a much higher margin compared to the product revenue. So once the product starts growing, because the product has a lower gross margin, that probably will impact the margin but the product is also the leading indicator of future service. So that’s where we kind of also were happy to see the product also starting growing now which I think going forward with the product has a higher percentage, that probably also will impact the margin.

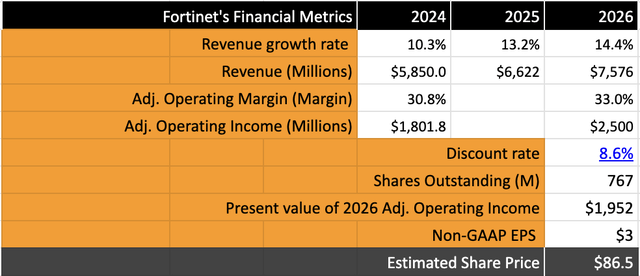

Fortinet’s Valuation Upgraded On Strong Operating Leverage

With no change in billings yet, I am still leaving my revenue targets unchanged for CY25 and CY26, while I am upgrading Fortinet’s CY24 targets to mirror management’s guidance. This implies 12-13% CAGR in top-line growth through CY26.

Fortinet’s model now gets a boost due to the operating margin expansion, where I expect margins to expand by 220 bp through CY26 based on my observation in the previous section. This points to an 18% growth in adjusted earnings, which implies a forward valuation multiple of ~34x.

Exhibit F: Fortinet’s valuation model shows upside (Author)

My model assumes a discount rate of 8.6% and a share dilution rate of half a percent to 1%. Management indicated that there was no share repurchase activity in Q2.

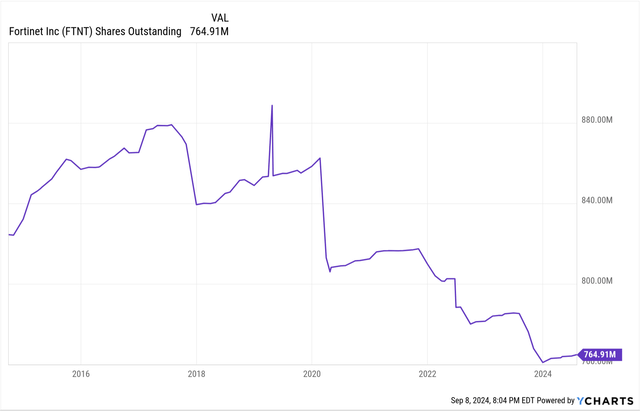

However, their forward guidance did indicate that they would exit 2024 with shares outstanding in the range of 767-777 million, which implies their share base would contract by 1.4-2.6% y/y in 2024.

I suspect management might utilize the remaining $1 billion of its buyback authorization to repurchase shares this year itself. If management does confirm that, expect another boost to the stock price.

Exhibit G: Fortinet’s shares outstanding trends lower. (YCharts)

I also expect management to announce a new share buyback program in the next two quarters after management exhausts the remaining $1 billion of its previous buyback program.

Risks & Other Factors To Consider

The key now will be to watch for Fortinet’s inventory levels, and any further drop will confirm an inflection in their firewall product business. Assuming their service business continues to grow in the double digits, the inflection of its product business will be a huge boost to the company’s outlook.

Fortinet is expected to host an Analyst Day in a few months on November 18th, where I expect management to positively update its midterm model with revised estimates on growth rates and margins. Some of those hints were strongly alluded to in the Q2 earnings call itself.

Fortinet’s management will also be participating in Goldman Sachs’ Communcopia Tech conference event tomorrow, which may also move the stock.

Takeaway

To reiterate my key takeaway from Fortinet’s recently concluded Q2 quarter, there is no better way to characterize the earnings report apart from saying that the cybersecurity’s margins look to be on steroids. The improvement in Fortinet’s product business points to an inflection and, coupled with the strong growth in its service business, is adding immense firepower to the company’s earnings outlook more than its sales outlook.

I expect Fortinet to be a winner in the next few months, and I am upgrading this stock to a Buy.

Read the full article here

")

")

")

")