")

")

")

(NASDAQ:CARG)")

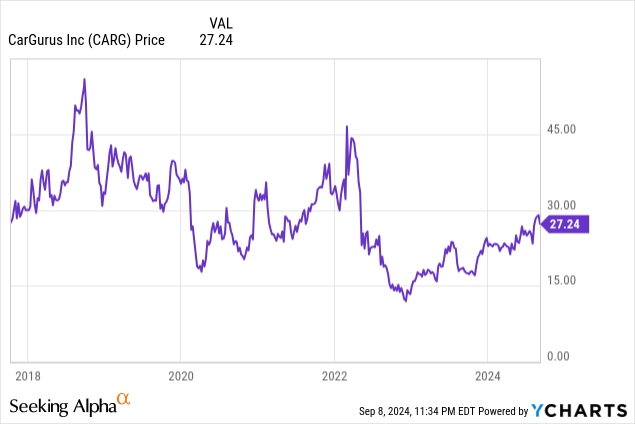

The Q2 earnings season has been surprisingly kind to a lot of out-of-spotlight rebound plays that delivered earnings beat in the wake of some high-profile misses in larger companies. CarGurus (NASDAQ:CARG) has been one of the beneficiaries of the market’s renewed willingness to bet on rebounds. The largest used car marketplace site posted acceleration in its core marketplace business in Q2, which sparked a rally in the stock that took YTD gains to above 15%:

I last wrote a bullish note on CarGurus in June, when the stock was still trading at $25 per share. Since then, CarGurus’ favorable Q2 earnings release has sparked a fresh rally in this stock: but instead of holding on for further gains, I recommend taking profits on this trade here and am downgrading CarGurus to a neutral rating.

At current higher share prices, I see a more balanced bull and bear case for this stock. In particular, two new risks have emerged:

- CarGurus is facing declining U.S. traffic, which may get worse in the wake of a recession. CarGurus’ traffic overall is flat, but it’s international that’s growing while the U.S. is receding. If we head into a recession in the back half of this year, interest in car purchases (which are discretionary buys, after all) may wane even further.

- CarGurus’ marketplace revenue growth is driven by higher average spend from its dealerships. The company has been gravitating toward larger dealerships with bigger budgets and a greater willingness to sign up for premium subscription tiers. And yet if underlying consumer demand also softens, particularly in the U.S., dealerships will also pull back on their spending as they did in the early days of COVID.

Of course, these risks are still counterbalanced by some longer-term positives for CarGurus:

- CarGurus remains the #1 site for used-car research in the U.S., and by a wide margin. By default, car dealerships (or any business, really) will go where the eyeballs are, and CarGurus has cemented its place as the leading site to do research before buying a used car.

- CarGurus has made itself essential for car dealerships. Even before adding CarOffer and Instant Max Cash Offer, CarGurus was long considered by dealerships to be a necessary partner due to the amount of web traffic flowing through its site nationwide. By adding the ability for dealerships to buy cars through the CarGurus network as well, CarGurus has effectively just doubled its wallet share within the used-car industry.

- Reliable recurring revenue streams that have a proven history of working through down cycles. CarGurus enjoys a steady stream of fee income from its paying car dealerships. Quarterly average revenue per car dealership also continues to rise. CarGurus has also proven itself capable of managing through downturns, swiftly acting to support struggling dealership customers in the immediate aftermath of COVID but now recovering even after those actions.

Still: given the near-term decline in traffic which is the ultimate dictator of car dealerships’ spending budgets, I’d take this opportunity to exert caution and reinvest my profits into other stocks.

Q2 download

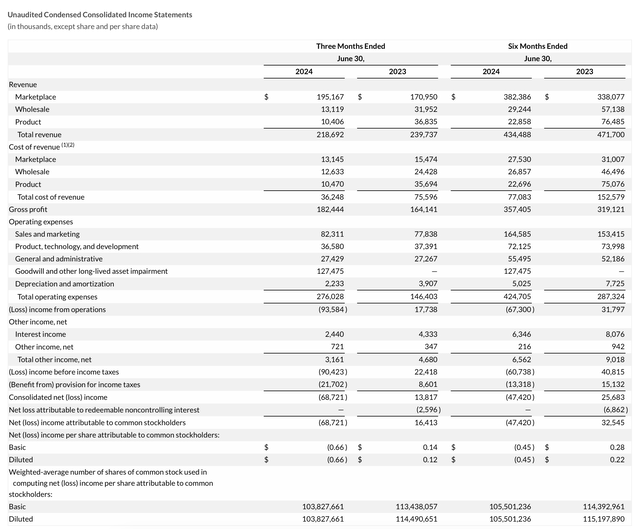

Let’s now go through CarGurus’ latest quarterly results in greater detail. The Q2 earnings summary is shown below:

CarGurus Q2 results (CarGurus Q2 earnings deck)

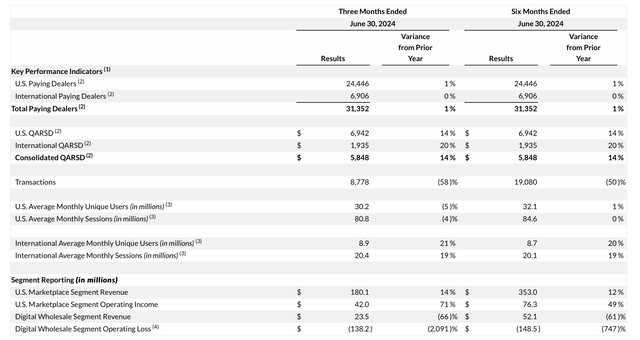

Investors cheered the company’s 14% y/y growth in marketplace revenue to $195.2 million, which accelerated over Q1’s 12% y/y growth pace. As a reminder, CarGurus has re-shifted its focus away from proprietary car sales and back on growing the marketplace business, which generates revenue from subscription and advertising fees from paying dealerships.

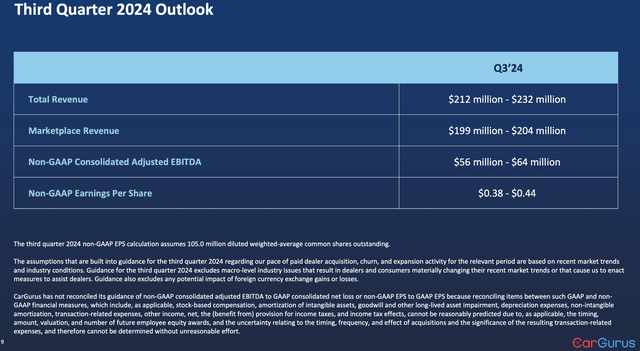

The company is pointing to continued health in the marketplace business as well, with its guidance for Q3 calling for $199-$204 million in revenue, which is an 11-13% growth range for the segment which generates nearly 90% of the company’s revenue.

CarGurus outlook (CarGurus Q2 earnings deck)

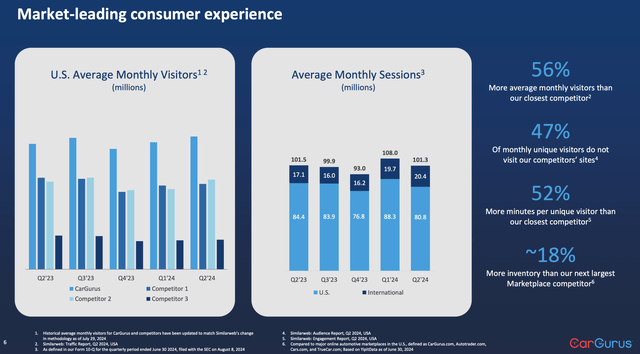

And yet, risks are emerging. Dealerships pay CarGurus to gain access to traffic eyeballs: and this is declining, at least in the U.S. As shown in the chart below, average monthly sessions in Q1 fell slightly y/y to 101.3 million, but the international segment (which is still a small portion of traffic as well as revenue) grew 19% y/y, while U.S. traffic declined -4% y/y to 80.8 million.

CarGurus traffic data (CarGurus Q2 earnings deck)

In fact, the primary reason that CarGurus’ revenue is growing is because QARSD (quarterly average revenue per dealer) is increasing 14% y/y.

CarGurus core metrics (CarGurus Q2 earnings deck)

Management noted that higher subscription tiers and greater attach rates of add-on products, from the dealership side, are the contributors to this growth. Per CEO Jason Trevisan’s remarks on the Q2 earnings call:

Our marketplace business accelerated for the fifth consecutive quarter, delivering 14% year-over-year growth and marketplace EBITDA grew 49% year-over-year with margins expanding 735 basis points versus the prior year period. In the second quarter, we achieved the highest quarterly revenue increase since 2021 driven by growth in our global dealer base, increased adoption of add-on products and migration toward higher subscription tiers.

Notably, in the U.S., our customer base has increasingly shifted toward larger dealers with higher advertising budgets who have a greater demand for data insights and analytics. We are also seeing a sustained increase in wallet share across our dealer base as more dealers adopt additional value added products, whether purchased à la carte or included in premium packages. This is evidenced by our double-digit year-over-year revenue growth while long-term advertising budgets for publicly traded dealers have increased at a mid to high single-digit rate.

We continue to experience strong momentum in our international business, which grew revenue 21% year-over-year with gross profitability in line with our domestic business. The outperformance was driven by sustained growth both in the UK and Canada, where we further expanded our traffic share and dealer base.”

And yet, if traffic declines, so will dealerships’ advertising budgets and willingness to buy add-on products. In my view, the decline in U.S. traffic is a symptom of consumers pinching their budgets and delaying major purchases, coincident with the possibility of a coming recession.

In other words, I don’t consider CarGurus’ latest acceleration in growth rates as particularly durable if underlying traffic doesn’t improve.

Key takeaways

With sharp gains in CarGurus’ stock since the company posted Q2 results, I recommend that investors take profits here and move to the sidelines. While the company’s re-acceleration in marketplace growth rates and improving profitability are admirable, I’m worried as lower traffic metrics may be a forward-looking indicator for a growth slowdown in the quarters ahead.

Read the full article here

")

")

")

")