")

")

")

")

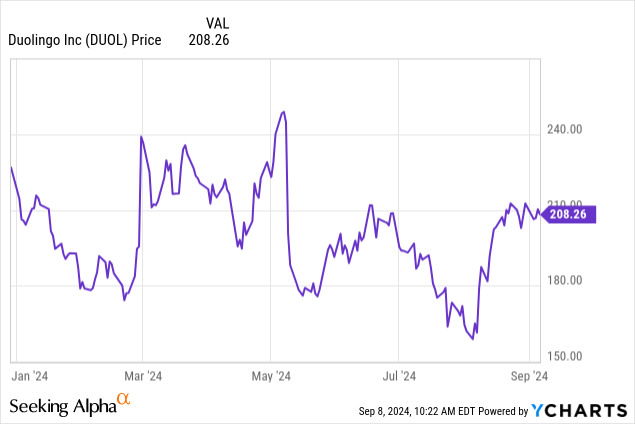

Over the past few weeks, it has seemed as if the market can’t decide whether it wants to be bullish or bearish. And amid heightened volatility, investors should also take care to deploy careful stock-picking in order to beat the sideways market.

One stock that has been particularly volatile this year is Duolingo (NASDAQ:DUOL), the popular language-learning app. Year to date, the stock is only about flat, but with wild gyrations in between, especially after earnings releases. The company has rallied after raising its FY24 outlook yet again in early August alongside its Q2 earnings print, but it has only managed to barely recoup losses after posting Q1 results. The question for investors now is: is Duolingo a buy as a rebound play?

I last wrote a neutral opinion on Duolingo in May, when the stock was trading just above $200. At the time, I had argued that the company was fairly valued, and that its still-strong but slowing growth rates were counterbalanced by rapidly rising adjusted EBITDA margins. At the time, I had advocated a $168 price target based on a 7x FY25 revenue multiple.

Duolingo’s Q2 earnings print makes me moderately more optimistic on the company’s prospects. And yet, we still can’t deny its slowing growth rates and more pessimistic measures, like its MAU growth and bookings growth rates both lagging behind its revenue growth. At the same time, with the company having reset expectations higher, I also believe a slightly higher entry point/price target is warranted. But with all the puts and takes here, I still remain neutral on this stock as Duolingo very much remains a “high price for a high quality” tech investment amid an expensive stock market where I prefer value plays.

Valuation checkup amid guidance boost

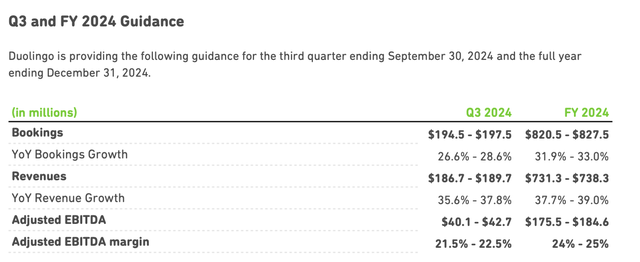

First, let’s parse through the company’s latest guidance boost and what that means for forward-looking multiples.

Duolingo raised its revenue expectations for the current year to $731.3-$738.3 million, or 37.7-39.0% growth – up from a 37.0-38.0% range previously. It’s also bumping up its adjusted EBITDA margins to 24-25%, from 23-24% previously.

Duolingo outlook update (Duolingo Q2 shareholder letter)

Street expectations for FY25 have also floated higher. For FY25, consensus is calling for revenue of $945.8 million, or 28% y/y growth. And if we conservatively assume two points of adjusted EBITDA margin expansion next year (at 27%, in line with Q2 actual margins), adjusted EBITDA would be $255 million.

Meanwhile, at current share prices near $208, Duolingo trades at a market cap of $9.07 billion. After netting off the $747.6 million of cash on Duolingo’s most recent balance sheet, the company’s resulting enterprise value is $8.32 billion. This puts Duolingo’s valuation multiples at:

- 8.8x EV/FY25 revenue

- 32.6x EV/FY25 adjusted EBITDA

I continue to believe that a more comfortable, buffered entry point for Duolingo lies at 7x EV/FY25 revenue, or a $170 price target. It’s worth noting that Duolingo stock briefly broke below this level in late July until Q2 results and the ensuing guidance boost lifted optimism for this name, suggesting that there may be a resistance point here.

All in all: this is a great watch list stock, but don’t jump the gun until Duolingo slides back down to the low $170s. With ongoing market volatility, there will be many opportunities to buy this stock for cheaper.

Q2 download

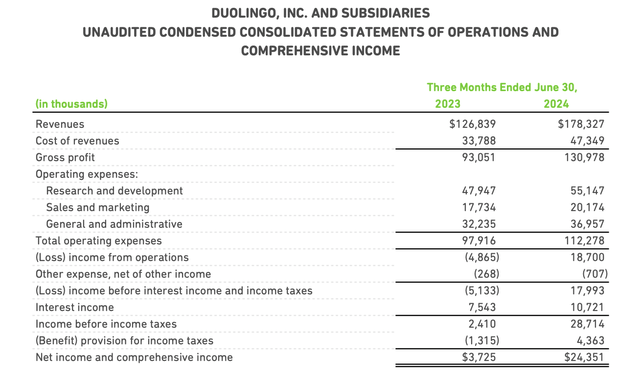

Let’s now go through Duolingo’s latest quarterly results in greater detail. The Q2 earnings summary is shown below:

Duolingo Q2 results (Duolingo Q2 shareholder letter)

Duolingo’s revenue grew 41% y/y to $178.3 million, ahead of Wall Street’s expectations for $177.1 million (+40% y/y). Growth decelerated from 45% y/y in each of the past two quarters.

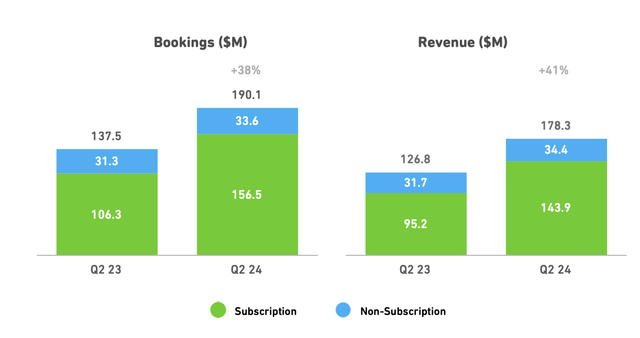

Here, I think it’s prudent to note two reasons why growth could slow down further. First is the company’s bookings growth rate. In Q2, bookings grew only 38% y/y to $190.1 million: higher than revenue on a nominal basis, but three points slower on a growth y/y basis.

Duolingo bookings (Duolingo Q2 shareholder letter)

Like various other gaming companies, Duolingo recognizes bookings as customers purchase in-game items or longer-term subscriptions, then recognizes revenue as the subscription term passes or customers consume the in-game items (in this case: non-premium Duolingo users can purchase “diamonds” which can be consumed to give them extra “lives” to correct mistakes made during lessons).

Another point worth calling out: Duolingo’s MAUs (monthly active users) grew 40% y/y to 101.6 million. This is an impressive figure on its own, but it’s slower than 52% y/y growth in paid subscribers (to 8.0 million). The subscription penetration rate against MAUs is certainly increasing, but I’d view these 100+ million users as the company’s longer-term paid subscription funnel. Fortunately, DAUs (daily actives) are growing at a faster 59% y/y clip.

The company also continues its healthy streak of innovation. It added new AI conversational capabilities to its Duolingo Max product, and also acquired a company called Hobbes that specializes in motion design and animation to improve the company’s character-based lesson design.

Here’s more context on the company’s user traction from CEO Luis Von Ahn’s remarks on the Q2 earnings call:

And not only did our business perform well, but we’re also making substantial progress on our long-term growth initiatives. This year, our monetization priorities are optimizing both our family plan and our tiered subscription plans so that we can offer learners more choices at various price points and increase LTV.

We continue to see excellent growth in our family plan. We’ve rolled out improvements to increase engagement between family members and we’re also helping existing individual subscribers discover and convert to family plan more often. As a result of these efforts, the family plan now makes up about 20% of our subscribers.

At the end of Q2, we began to see the impact of Duolingo Max, our highest-priced tier with AI-enabled features. The rollout of Max has progressed so that, as of now, it’s available in five countries in, sorry, in five courses in 27 countries, covering about 15% of our DAUs.”

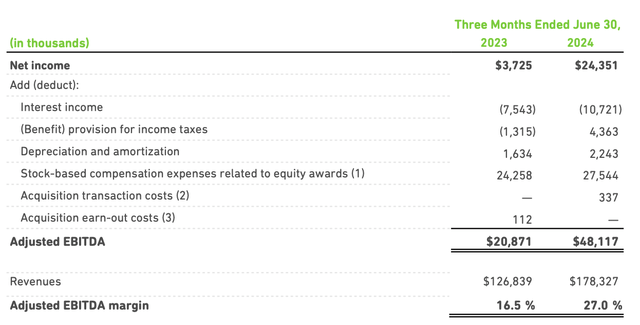

From a profitability standpoint, we note that Duolingo’s adjusted EBITDA soared more than 2x y/y to $48.1 million, or a 27.0% margin – nearly 11 points better y/y. The company is, however, expecting some margin deleverage to a ~22.0% midpoint margin in Q3 due to the timing of new hires, particularly in the R&D segment.

Duolingo adjusted EBITDA (Duolingo Q2 shareholder letter)

Key takeaways

Duolingo continues to be an impressive growth company that is aggressively pursuing new features and expanding its content, which is being rewarded by a rapid boost in subscribers and revenue. This high-quality company, however, is trading at a steep price which in my view leaves little room for upside. I’d prefer to wait for the low ~$170s before diving in.

Read the full article here

")

")

")

")